The impact of stablecoins on small banks has received a lot of attention, but not for the right reasons.

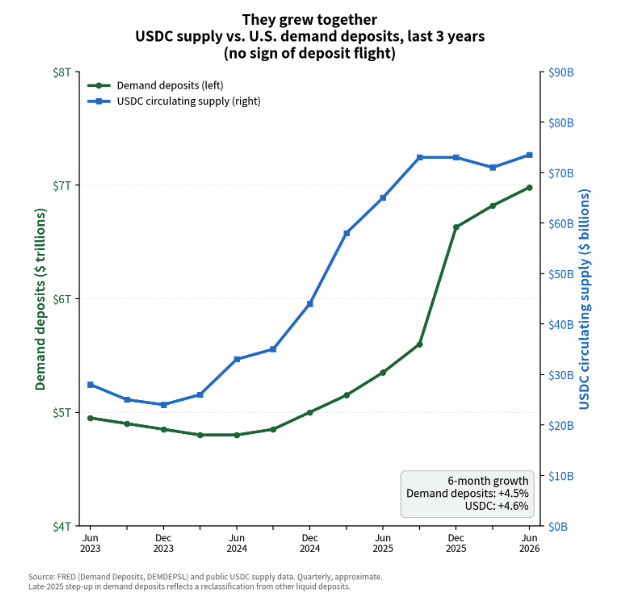

Let’s recap: Multiple empirical studies have found no meaningful link between stablecoin growth and bank deposits. As USDC grew to ~$75B, overall bank and community bank deposits grew right alongside it. In fact, over the last 6 months, USDC has grown 4.6%, and total demand deposits have grown 4.5%. No displacement there.

Now the part small banks should actually care about: stablecoins enable ~4,000 community and regional banks to punch above their weight. Same 24/7 settlement and cross-border rails as a $3T GSIB. And with partners like @Fiserv, @Visa, and @crossriverbank, it's a configuration, not a multi-year build. No billion dollar IT budget or crypto team required.

For more detail, see our new @coinbase Institute @CoinbaseCBI paper: "Small Banks and Stablecoins: Nothing to Fear, Much to Gain"

Let’s recap: Multiple empirical studies have found no meaningful link between stablecoin growth and bank deposits. As USDC grew to ~$75B, overall bank and community bank deposits grew right alongside it. In fact, over the last 6 months, USDC has grown 4.6%, and total demand deposits have grown 4.5%. No displacement there.

Now the part small banks should actually care about: stablecoins enable ~4,000 community and regional banks to punch above their weight. Same 24/7 settlement and cross-border rails as a $3T GSIB. And with partners like @Fiserv, @Visa, and @crossriverbank, it's a configuration, not a multi-year build. No billion dollar IT budget or crypto team required.

For more detail, see our new @coinbase Institute @CoinbaseCBI paper: "Small Banks and Stablecoins: Nothing to Fear, Much to Gain"

Here’s the paper: coinbase.com/public-policy/…

• • •

Missing some Tweet in this thread? You can try to

force a refresh