1/ Have been meaning to do a thread on Soitec for a while.

Relative to the impact it will have on the world I'd wager that it's one of the least known stocks in Europe.

It's my second largest position and even though it's had a good run I think there's still some way to go.

Relative to the impact it will have on the world I'd wager that it's one of the least known stocks in Europe.

It's my second largest position and even though it's had a good run I think there's still some way to go.

2/ Soitec has had a chequered history to say the least; it nearly went bankrupt a few years ago thanks to an ill-advised venture into solar panels.

In 2015, however, a new CEO was appointed and he ultimately refocused the business on its crown jewel, SOI.

In 2015, however, a new CEO was appointed and he ultimately refocused the business on its crown jewel, SOI.

3/ SOI is an acronym for silicon on insulator.

Effectively, it is a wafer (of the silicon variety) that has an extremely thin layer cut from a 'donor' wafer affixed to its surface.

This video explains it pretty well.

Effectively, it is a wafer (of the silicon variety) that has an extremely thin layer cut from a 'donor' wafer affixed to its surface.

This video explains it pretty well.

4/ Why bother?

There are a bunch of reasons, but the most pertinent is that with standard 'bulk' wafers electrons can leak through the wafer - not efficient.

With SOI the affixed layer acts as an insulator, preventing leakage and enabling ultra low power consumption.

There are a bunch of reasons, but the most pertinent is that with standard 'bulk' wafers electrons can leak through the wafer - not efficient.

With SOI the affixed layer acts as an insulator, preventing leakage and enabling ultra low power consumption.

5/ Soitec makes a few different types of SOI wafers, which are explained in this excellent article, but the main growth driver is FD-SOI (FD = fully depleted).

This is the 'flavor' of SOI that is specifically designed for the lowest power usage.

eejournal.com/article/the-ma…

This is the 'flavor' of SOI that is specifically designed for the lowest power usage.

eejournal.com/article/the-ma…

6/ As you can imagine, a wafer that allows chips to be built that have ultra low power consumption is pretty vital as we move towards a world of smart devices and the much heralded IoT.

IoT may not even be possible in the same way without FD-SOI.

IoT may not even be possible in the same way without FD-SOI.

7/ A couple of cool examples:

The GPS chips in pretty much all smartwatches are built on FD-SOI wafers.

Renesas has developed a microcontroller that uses a tenth of the energy of its predecessors using FD-SOI.

eenewseurope.com/design-center/…

The GPS chips in pretty much all smartwatches are built on FD-SOI wafers.

Renesas has developed a microcontroller that uses a tenth of the energy of its predecessors using FD-SOI.

eenewseurope.com/design-center/…

8/ The other, still important, growth driver is RF-SOI (RF = radio frequency).

These wafers are the standard in the antenna in smartphones. As we move from 3G to 4G to 5G the surface area of RF-SOI required increases materially.

These wafers are the standard in the antenna in smartphones. As we move from 3G to 4G to 5G the surface area of RF-SOI required increases materially.

9/ Soitec then has two main growth drivers: FD-SOI has wearables, IoT, etc, and RF-SOI has 5G.

Fortunately these two products account for the majority of sales.

In the most recent fiscal year Soitec grew by 42% and management think over the next five years they can do ~25% pa.

Fortunately these two products account for the majority of sales.

In the most recent fiscal year Soitec grew by 42% and management think over the next five years they can do ~25% pa.

10/ Competition?

Soitec has 70% of the SOI market and this has been stable for a long time.

The key is the manufacturing process, known as Smart Cut. It is difficult.

Cutting ever-thinner layers from the donor wafer requires experience and Soitec has been doing it for decades.

Soitec has 70% of the SOI market and this has been stable for a long time.

The key is the manufacturing process, known as Smart Cut. It is difficult.

Cutting ever-thinner layers from the donor wafer requires experience and Soitec has been doing it for decades.

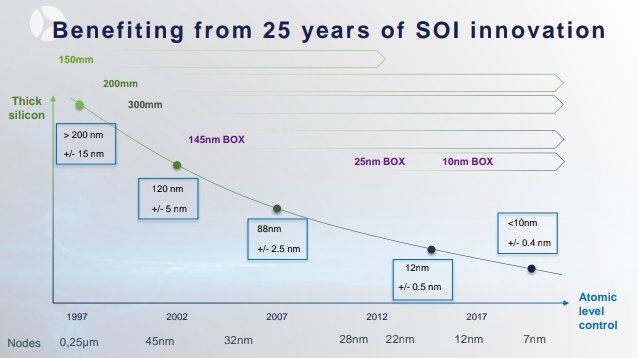

11/ To illustrate the difficulty...

FD-SOI wafers need an insulating layer that is uniformly 10nm thick (around 20 Si atoms) across a 300mm diameter wafer. Nothing is perfectly uniform but the imperfections can't be greater than 0.4nm. That is 0.0001% of the wafer's diameter.

FD-SOI wafers need an insulating layer that is uniformly 10nm thick (around 20 Si atoms) across a 300mm diameter wafer. Nothing is perfectly uniform but the imperfections can't be greater than 0.4nm. That is 0.0001% of the wafer's diameter.

12/ In addition there are a bunch of patents around the Smart Cut process.

There are two other companies that make SOI wafers: Shin Etsu and GlobalWafers. They both license the manufacturing technology from Soitec and pay royalties.

There are two other companies that make SOI wafers: Shin Etsu and GlobalWafers. They both license the manufacturing technology from Soitec and pay royalties.

13/ Shin Etsu is the biggest 'bulk' wafer supplier in the world and has been producing SOI wafers and licensing the technology from Soitec since the late 90s.

GlobalWafers is newer to it and has only been making them since their acquisition of SunEdison in 2016.

GlobalWafers is newer to it and has only been making them since their acquisition of SunEdison in 2016.

14/ Both Shin Etsu and GlobalWafers are technologically behind Soitec. Neither of them are yet qualified to manufacture 300mm wafers (which are over half of Soitec's sales). Only Shin Etsu is even trying to qualify at the moment, as I understand it.

15/ The usual pattern in the industry is this: Soitec comes out with an innovative new use case for SOI, they initially have a virtual monopoly, competition comes and their share eventually settles down to ~70%. Rinse and repeat.

16/ The result of the benign competitive environment is Soitec makes 30%+ EBITDA margins.

This is despite having huge customers such as GlobalFoundries and Samsung, both of which have recently signed long term supply agreements with Soitec.

This is despite having huge customers such as GlobalFoundries and Samsung, both of which have recently signed long term supply agreements with Soitec.

17/ That's more or less it.

Soitec is researching other possible use cases for the Smart Cut manufacturing process, some of which are quite cool and have the potential to be material in the next five years.

Soitec is researching other possible use cases for the Smart Cut manufacturing process, some of which are quite cool and have the potential to be material in the next five years.

18/ Also, Eric Meurice is the Chairman. He was CEO of ASML from 2004 to 2013. Under him ASML became the world leader in lithography machines and the share price more than quadrupled.

19/ So, what are you paying for all this? Around 25x NTM earnings.

I believe Soitec will comfortably justify this valuation.

If you want more info they had a CMD recently. Check it out. I'm also happy to chat about Soitec until the cows come home.

End thread.

I believe Soitec will comfortably justify this valuation.

If you want more info they had a CMD recently. Check it out. I'm also happy to chat about Soitec until the cows come home.

End thread.