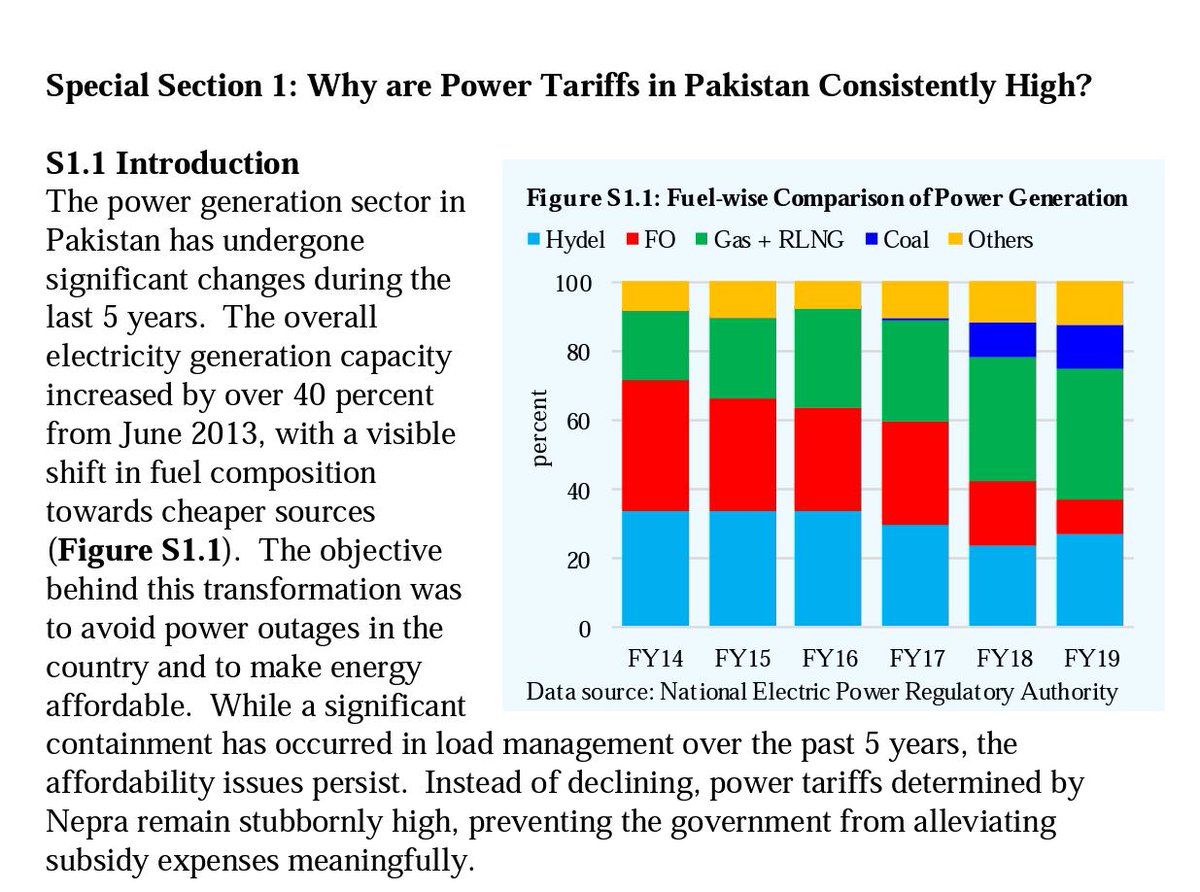

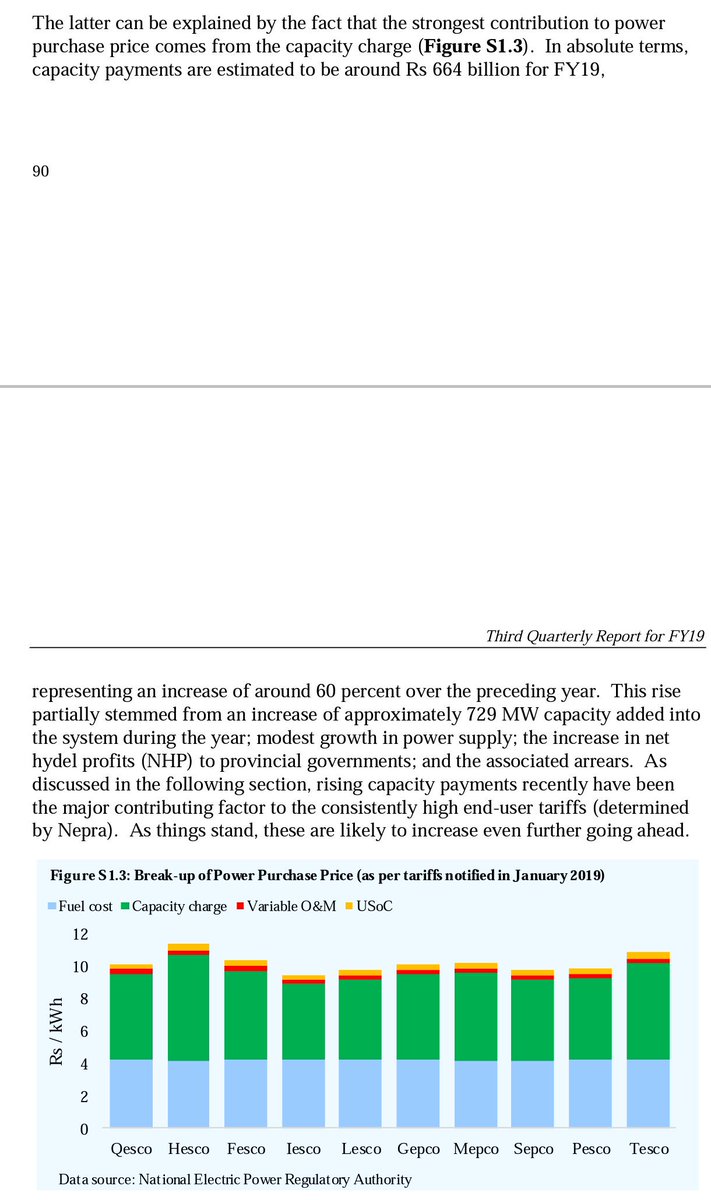

#PMLN govt was successful in shifting electricity prod away frm furnace oil towards LNG. So y hav electricity prices not come down? CULPRIT: Capacity charges!

@StateBank_Pak report explains y capacity charges hav increased over time: (Special Section 1) bit.ly/2xVScqo

@StateBank_Pak report explains y capacity charges hav increased over time: (Special Section 1) bit.ly/2xVScqo

Electricity production will continue to increase. However (and unfortunately), electricity prices will also continue to increase even wen we will start producing electricity using coal, hydro and nuclear. Whoever came up with 'capacity charge' formula screwed us big time!

UPDATE: someone working at NEPRA says that the reason for indexing to dollars is bec most IPPs are financed in . Perhaps this is reasonable. But then one is to ask why were these projects not financed by local banks? Especially those owned by domestic players.

• • •

Missing some Tweet in this thread? You can try to

force a refresh