Economist at @BristolUni. Interested in macroeconomics. Retweet is not endorsement. From #Bhera/#Islamabad!

In simple terms, these were profits that were not paid out in dividends but were held back. But held back as what? Note, Lucky Cement has only close to 1bn in cash and deposits. This only means these profits were invested in different types of assets - both short and long-term.

In simple terms, these were profits that were not paid out in dividends but were held back. But held back as what? Note, Lucky Cement has only close to 1bn in cash and deposits. This only means these profits were invested in different types of assets - both short and long-term.

$610million worth of Eurobonds were also restructured in Dec 1999 to comply with the requirements of Paris Club that Pak should secure similar treatment from other private creditors. Another $415million which was owed to commercial banks was also restructured in the same month.

$610million worth of Eurobonds were also restructured in Dec 1999 to comply with the requirements of Paris Club that Pak should secure similar treatment from other private creditors. Another $415million which was owed to commercial banks was also restructured in the same month.

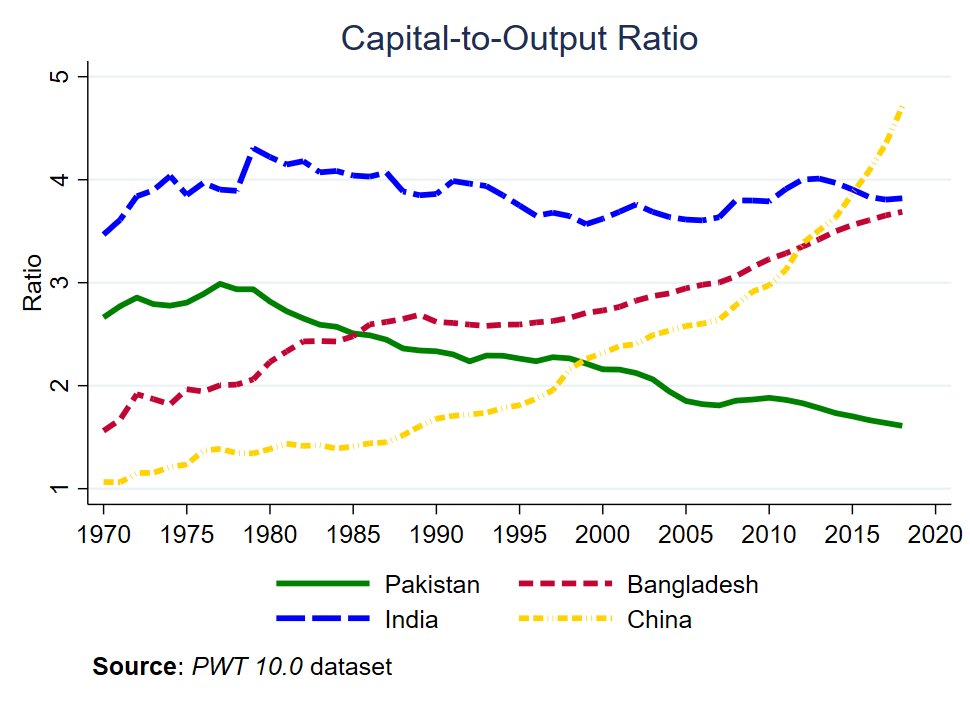

Let's first put this in perspective. The decline in capital-to-output ratio we see for Pak is the exact opposite of what we see in the region. The ratio has remained stable for India. However, both Bangladesh and China have accumulated much more capital over the same time period.

Let's first put this in perspective. The decline in capital-to-output ratio we see for Pak is the exact opposite of what we see in the region. The ratio has remained stable for India. However, both Bangladesh and China have accumulated much more capital over the same time period.

2/5: As far as CDS is concerned, the paper assessing Bloomberg's model clearly suggests that CDS is a better indicator than whatever the Bloomberg model is telling us. Hard to disagree when the model only throws out a default probability of 17% one month before it happens.

2/5: As far as CDS is concerned, the paper assessing Bloomberg's model clearly suggests that CDS is a better indicator than whatever the Bloomberg model is telling us. Hard to disagree when the model only throws out a default probability of 17% one month before it happens.

The story is quite simple. Govt borrowing (net) from external sources remained almost negligible. Public external debt only increased by about $8bn between Jul-08 and Jun-13. And since there were less dollars in the system, there was less to spend on imports during this period.

The story is quite simple. Govt borrowing (net) from external sources remained almost negligible. Public external debt only increased by about $8bn between Jul-08 and Jun-13. And since there were less dollars in the system, there was less to spend on imports during this period.

(2/n) ... this is not bec rest of the world thinks of Pak as an attractive place to invest. If this was the case (e.g. India), we wouldn't have to worry too much. The world would invest in us (e.g. FDI) and the country would produce enough in future (i.e. exports) to pay it back.

(2/n) ... this is not bec rest of the world thinks of Pak as an attractive place to invest. If this was the case (e.g. India), we wouldn't have to worry too much. The world would invest in us (e.g. FDI) and the country would produce enough in future (i.e. exports) to pay it back.

(2/n) Raza Baqir took on the task of reversing this to contain inflationary pressures over medium to long-term. Over the three years of his tenure, he decreased SBP's holdings of government bonds by more than a trillion.

(2/n) Raza Baqir took on the task of reversing this to contain inflationary pressures over medium to long-term. Over the three years of his tenure, he decreased SBP's holdings of government bonds by more than a trillion.

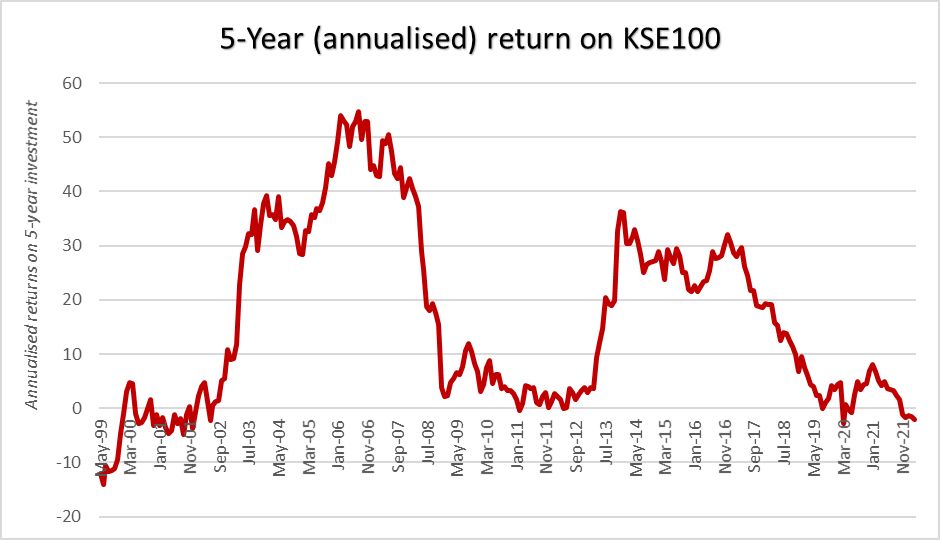

On average, u can expect to get an annual return of 16%. However, the standard deviation is also quite large at 17%. Meaning, investing in KSE100 index over a 5-year period comes with considerable risk. If u r risk averse, you may be better-off investing in bonds than in KSE100.

On average, u can expect to get an annual return of 16%. However, the standard deviation is also quite large at 17%. Meaning, investing in KSE100 index over a 5-year period comes with considerable risk. If u r risk averse, you may be better-off investing in bonds than in KSE100.

(2/n) While global economic conditions did have a significant negative effect on Pak export performance during 2020 (blue bars), the sharp recovery since then meant that the effect has been positive during most of FY21. See -ve blue bars during 2020, followed by +ve bars in FY21.

(2/n) While global economic conditions did have a significant negative effect on Pak export performance during 2020 (blue bars), the sharp recovery since then meant that the effect has been positive during most of FY21. See -ve blue bars during 2020, followed by +ve bars in FY21.

Also, I am not sure why everyone is assuming treasury yields should move one-to-one with the policy rate i.e. no change in spreads. If market anticipates that govt's repayment capacity will weaken in the future, treasury yields may go up by more than one-to-one with policy rate.

Also, I am not sure why everyone is assuming treasury yields should move one-to-one with the policy rate i.e. no change in spreads. If market anticipates that govt's repayment capacity will weaken in the future, treasury yields may go up by more than one-to-one with policy rate.

(2/5) We started with looking at the changing nature of trade in recent decades which is increasingly dominated by different components of the supply chain rather than the end product.

(2/5) We started with looking at the changing nature of trade in recent decades which is increasingly dominated by different components of the supply chain rather than the end product.

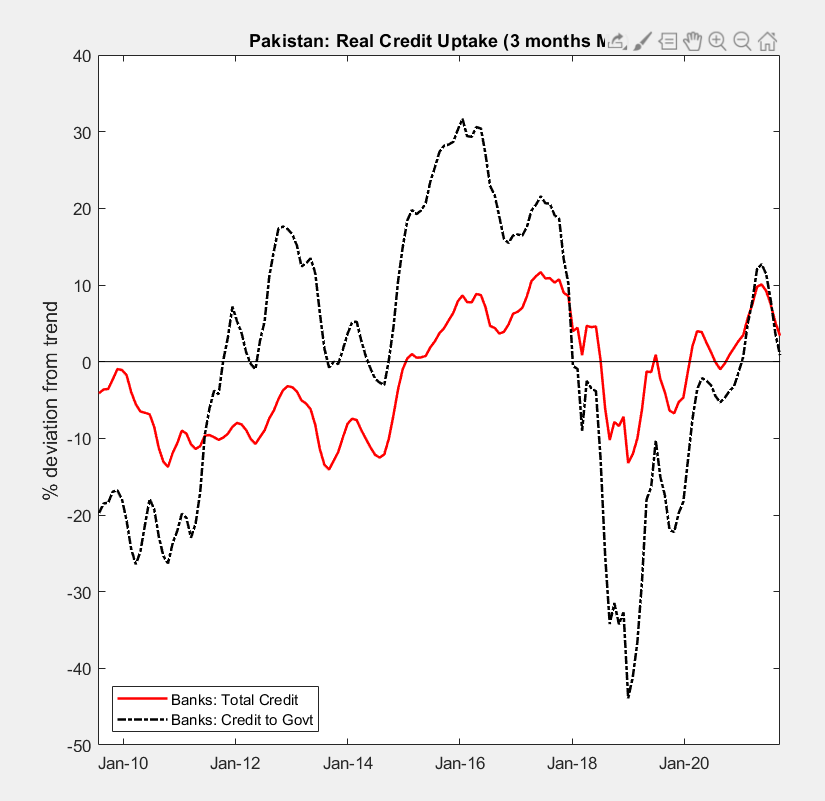

(2/4) In previous periods, every time govt decreased its borrowing from banks in response to increase in borrowing costs, it ended up increasing its borrowing from SBP. So far, this time around, we are not seeing this. However, in its place, there is something else going on ...

(2/4) In previous periods, every time govt decreased its borrowing from banks in response to increase in borrowing costs, it ended up increasing its borrowing from SBP. So far, this time around, we are not seeing this. However, in its place, there is something else going on ...

(2/n) I have used the information provided by the PBS to decompose the increase in dollar value of textile exports into 'price' and 'quantity' effects. It turns out that the contribution of 'quantity' to increase in textile exports is negative, whereas that of prices is positive.

(2/n) I have used the information provided by the PBS to decompose the increase in dollar value of textile exports into 'price' and 'quantity' effects. It turns out that the contribution of 'quantity' to increase in textile exports is negative, whereas that of prices is positive.