Good morning 🦁- it is Monday 🤗 Can’t wait for another week of Asian economics!!! Don’t worry, we’ll continue this NIRP thread during lunch hour (kind of fun to have a virtual reading club right?) This is where nerds rejoice 🤓🤓🤓😎💪🏻💪🏻💪🏻!!!

https://twitter.com/trinhnomics/status/1163005120201625600

Let's look at the agenda for this week:

South Korea 🇰🇷 1st 20-day of trade 🥳🤗 - fav data obvs because it is the 1st for the region & so far the 1st 10-day is really bad & China lending data horrible for July

Fed minutes

Indonesia rate - cut expected by me

Flash PMIs 👈🏻

South Korea 🇰🇷 1st 20-day of trade 🥳🤗 - fav data obvs because it is the 1st for the region & so far the 1st 10-day is really bad & China lending data horrible for July

Fed minutes

Indonesia rate - cut expected by me

Flash PMIs 👈🏻

Watch reforms to the Loan Prime Rate (LPR) that replaces the benchmark 1y lending rate of 4.35% for new ref rate for pricing of new corp loans from 20 Aug:

Frequency of adjustment MONTHLY on 20th each month

Linked to 1yMLF (3.3%)

# of participating banks rise to 18 from 10

Frequency of adjustment MONTHLY on 20th each month

Linked to 1yMLF (3.3%)

# of participating banks rise to 18 from 10

(Deleted old tweet b/c I said daily but should be monthly).

Note that the central bank said that the reform of the LPR can, "Achieve the effect of lowering the real interest rate for loans."

In other words, watch this stealth move by the PBOC to lower lending rates for the eco

Note that the central bank said that the reform of the LPR can, "Achieve the effect of lowering the real interest rate for loans."

In other words, watch this stealth move by the PBOC to lower lending rates for the eco

How rates work in China:

a) Benchmark lending rate for 1yr was 4.35% & that will be REPLACED TOMORROW

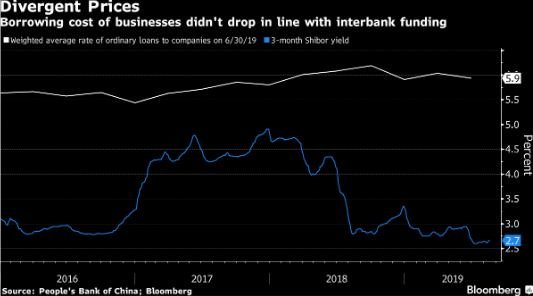

b) Average lending rates is 5.9% (above 4.35% & defo above ever-lower SHIBOR, which doesn't tell u much about funding conditions of eco but rather large banks)

c) MLF rate 3.3%

a) Benchmark lending rate for 1yr was 4.35% & that will be REPLACED TOMORROW

b) Average lending rates is 5.9% (above 4.35% & defo above ever-lower SHIBOR, which doesn't tell u much about funding conditions of eco but rather large banks)

c) MLF rate 3.3%

MLF stands for medium lending facility & this move on LPR key:

*18 reporting banks'll add a spread to the MLF (3.3%) based on own calculation of funding costs, demand, risks

*Submit before 9am on 20th/month

*LPR'll have longer tenure & ref for new loans

*Goal is to lower rates

*18 reporting banks'll add a spread to the MLF (3.3%) based on own calculation of funding costs, demand, risks

*Submit before 9am on 20th/month

*LPR'll have longer tenure & ref for new loans

*Goal is to lower rates

This is on the back of very bad lending data in July & the only thing that went up was local gov issuance so the PBOC is clearly worried about TIGHT LIQUIDITY & the stickiness of lending costs despite lower SHIBOR.

My good mornings are useful right? 🤗

My good mornings are useful right? 🤗

https://twitter.com/Trinhnomics/status/1160841814254878720?s=20

Oldies but definitely goodies on what happens next in China regarding PPI & - yes, the interview was on 15 Feb 2019 - on why rates will have to fall in China. This interview was the day after we published our 💌

"Interest rates have 1 direction to go🤗"

bloomberg.com/news/videos/20…

"Interest rates have 1 direction to go🤗"

bloomberg.com/news/videos/20…

And also this one to follow up on that one (all relevant today & I was right that the Korea deficit was a one-off):

bloomberg.com/news/videos/20…

bloomberg.com/news/videos/20…

And obvs this one a month ago - all relevant today. Btw, what happens when rates fall? Watch China tomorrow for the new LPR thing & also the OMO. People are watching this very intensely.

https://twitter.com/Trinhnomics/status/1159625534646575104?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh