Morning!!! EUR moved downward on stimulus expectations! Dollar 💵 king 🤴! The APAC region is watching:

China stealth move to lower rates (people watching OMO too not just lending), Korea super data tom (1st 20-day trade) Fed, Indonesia monetary (fiscal budget was out last wk)

China stealth move to lower rates (people watching OMO too not just lending), Korea super data tom (1st 20-day trade) Fed, Indonesia monetary (fiscal budget was out last wk)

https://twitter.com/trinhnomics/status/1163005120201625600

So today China CNY fix key but more key is LPR & also whether other rates will get pushed downward too. All have implications for China itself, the rest of the Asia region, & of course the world.

Q: What happens to FX when rates move lower? 🧐🧐🧐

Q: What happens to FX when rates move lower? 🧐🧐🧐

https://twitter.com/trinhnomics/status/1163260318476169218?s=21

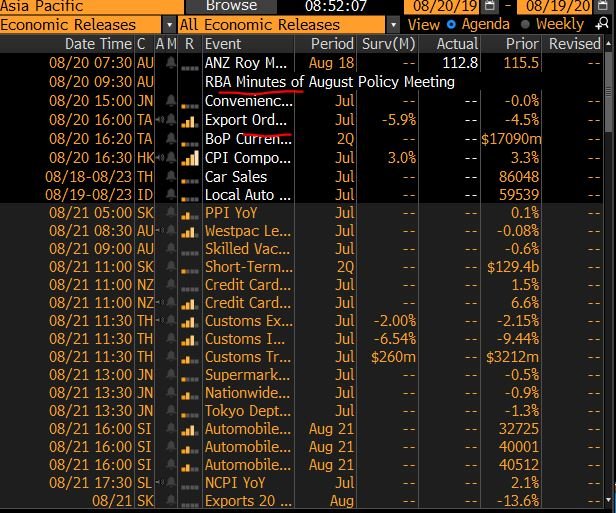

Busy morning! RBA minutes at 930 after China data. AUD has been trending back to the level of the day where RBNZ slashed rates by 50bps. Not a coincidence. Taiwan export orders out today & expectations are WORSE of -5.9% for July. But we all know that Korea is really the key data

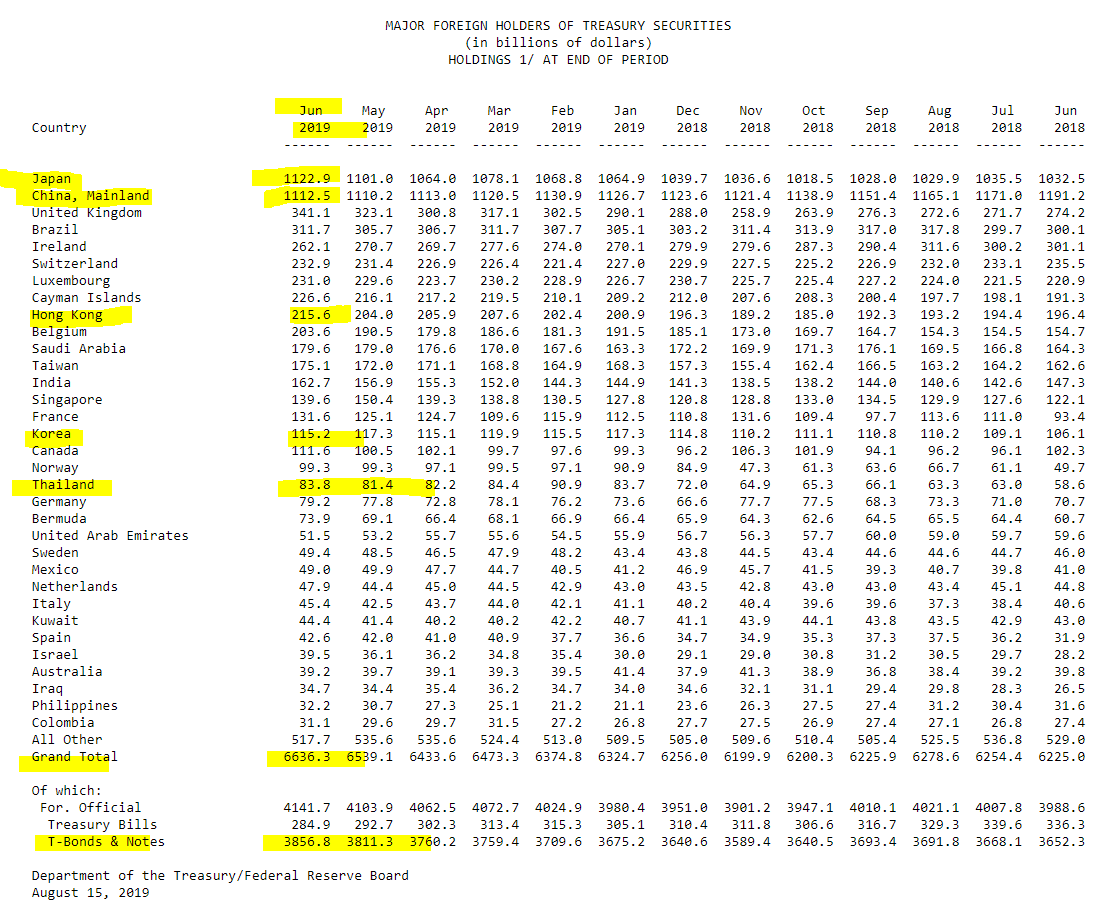

Let's look at foreign ownership of UST in June: it is totally up (+97.2bn). Note that some of this is due to valuation impact but still!

Japan 🇯🇵overtook China 🇨🇳 as the largest holder of UST! Everyone is buying thanks to NIRP. Btw, if u add it up, Europe 28 ownership BIGGEST!!

Japan 🇯🇵overtook China 🇨🇳 as the largest holder of UST! Everyone is buying thanks to NIRP. Btw, if u add it up, Europe 28 ownership BIGGEST!!

Repeat after me: NIRP loves PIRP! The US is totally PIRP (even if the Fed cuts rates by another 50bps by end 2019, still pretty PIRP compared to these NIRPers). Hence, King USD 🙇🏻♀️🙇🏻♀️🙇🏻♀️.

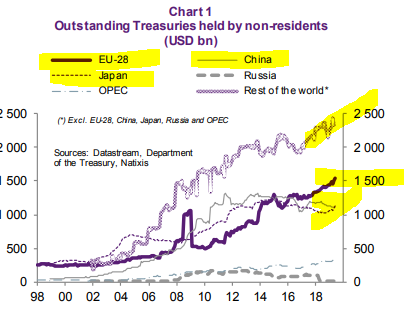

As China reduces purchases, the EU is buying more! So is Japan! So is the rest of the world!

As China reduces purchases, the EU is buying more! So is Japan! So is the rest of the world!

NIRP 😘💜 PIRP . Yep, true story - the data shows!!! Opposites attract! Totally complementary. Totally natural & u know what that means?

The PIRPers of EM Asia should be doing okay. We're talking about current account deficit guys like India, Indonesia, the Philippines, etc👏🏻👏🏻

The PIRPers of EM Asia should be doing okay. We're talking about current account deficit guys like India, Indonesia, the Philippines, etc👏🏻👏🏻

China 1yr LPR is 4.25%, which is 6bps lower 📉 (was 4.31% before) & so moving lower slowly here. Treading very gently here. Note that this is a rate set by 18banks w/ a spread over 3.3%1yr MLF.

RBA is saying that, "reasonable to expect extended period of low interest rates."

RBA is saying that, "reasonable to expect extended period of low interest rates."

• • •

Missing some Tweet in this thread? You can try to

force a refresh