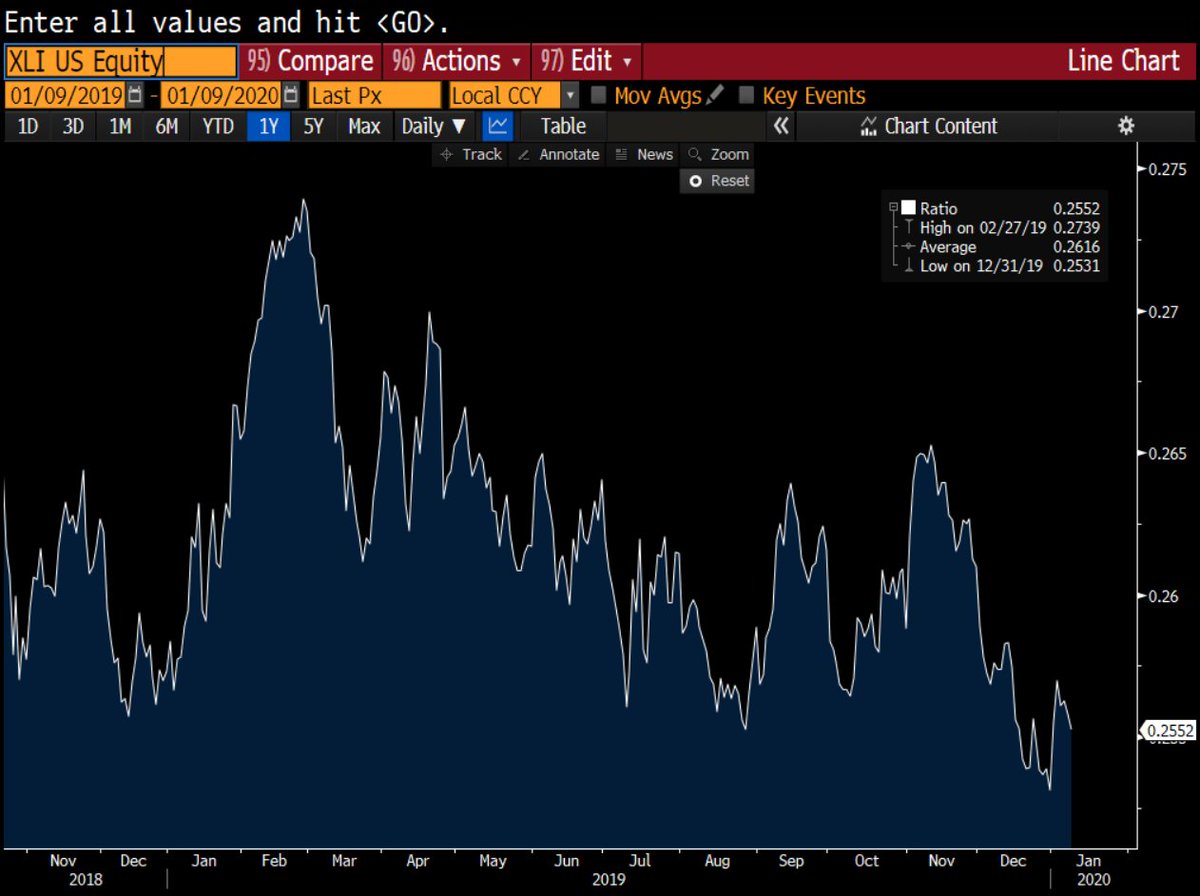

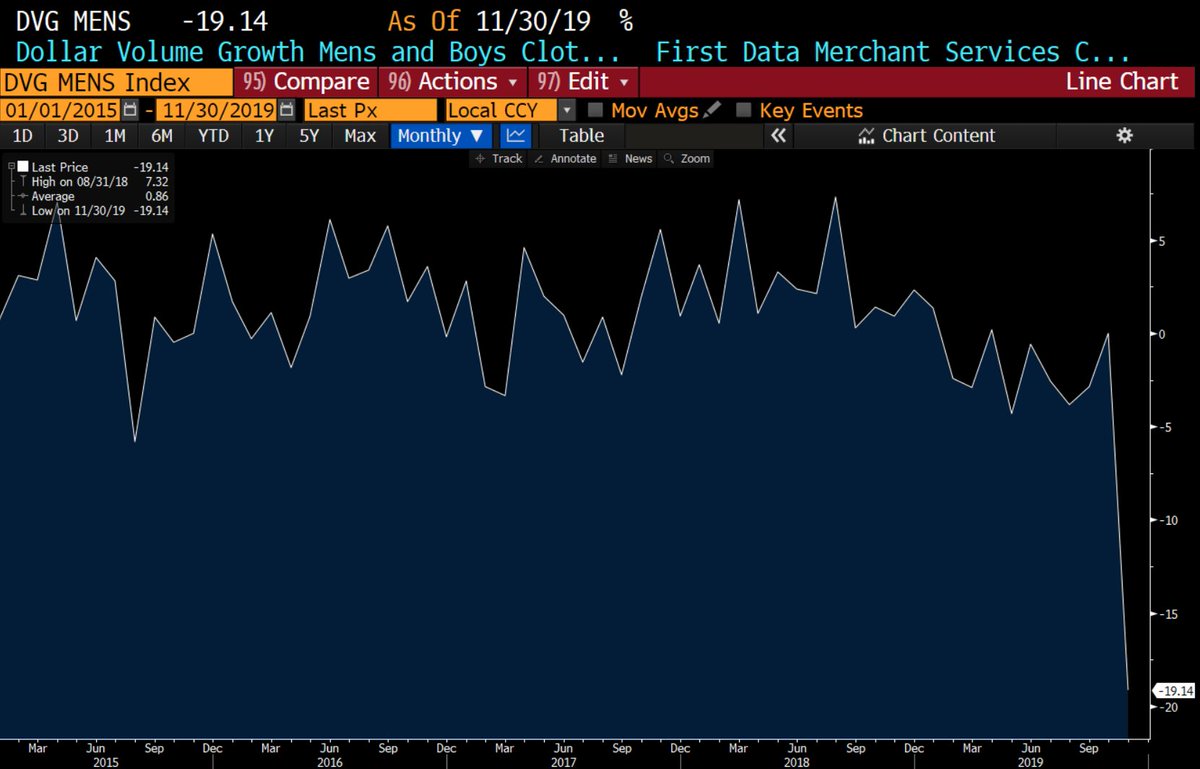

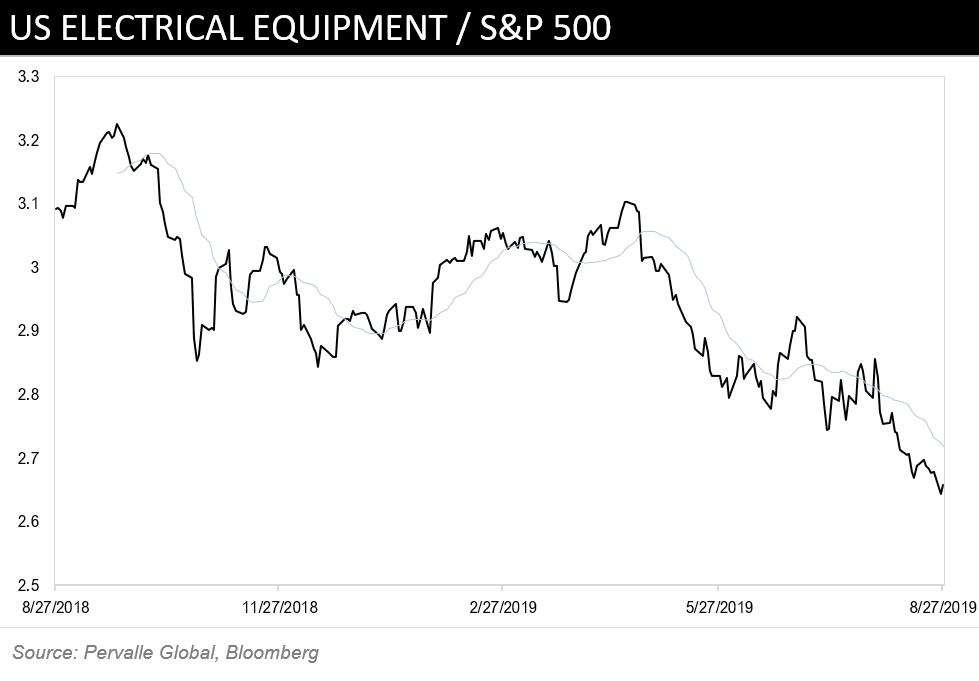

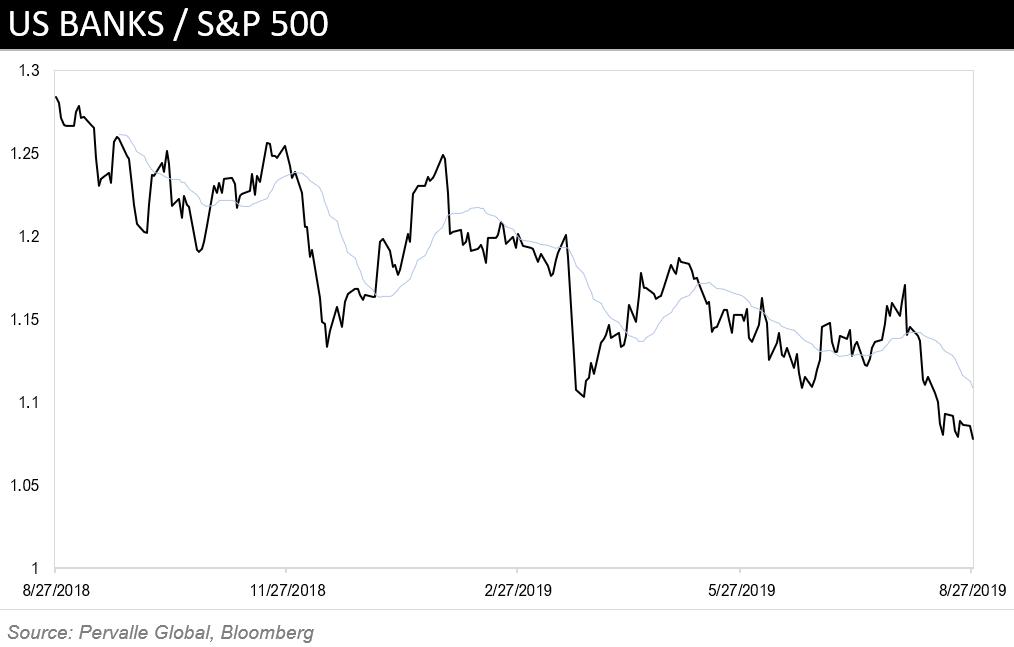

Some charts on relative performance confirming out leads.

US chemicals / $SPX -- new lows

US autos / $SPX -- new lows

US Machinery / $SPX -- new lows

US Electrical equipment / $SPX -- new lows

US Banks / $SPX -- new lows

Global financials / $ACWI -- lows

Global materials / $ACWI -- lows

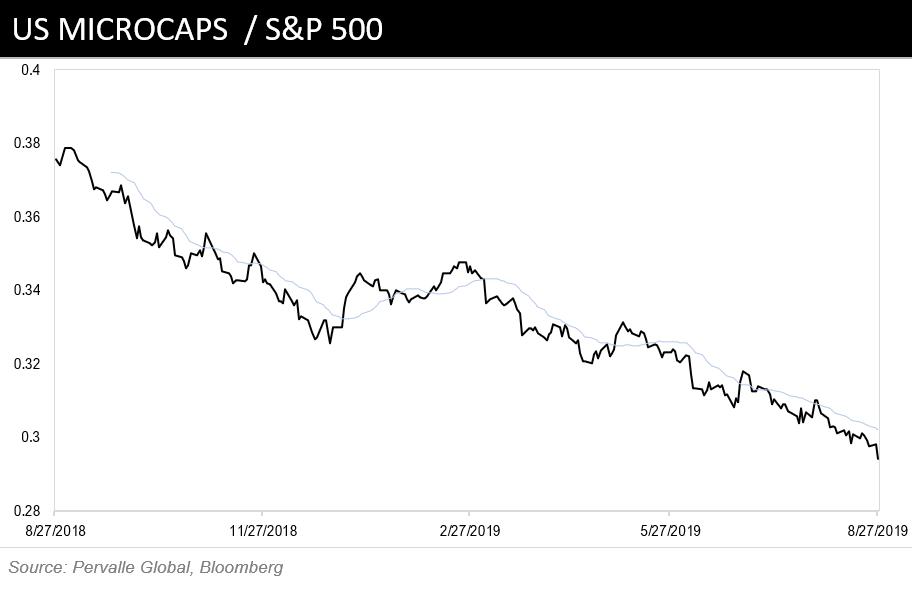

US Micro caps / $SPX -- no comment

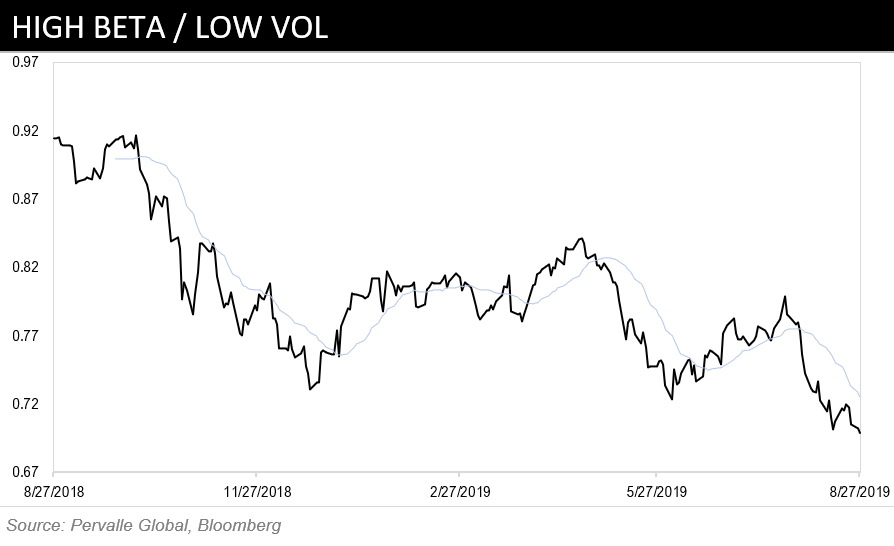

High beta / Low vol -- new lows

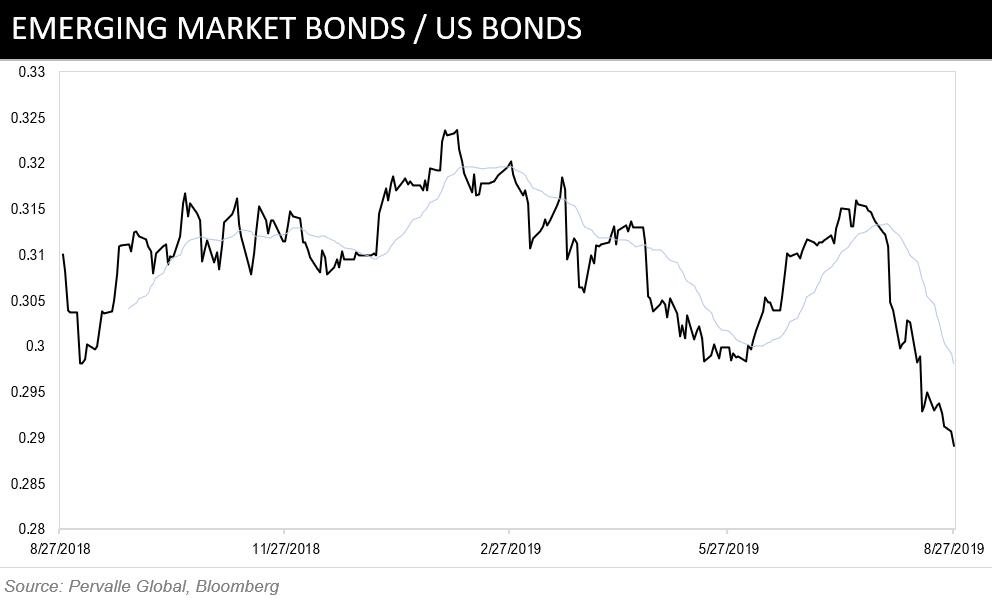

$EEM bonds / US bonds -- new lows

• • •

Missing some Tweet in this thread? You can try to

force a refresh