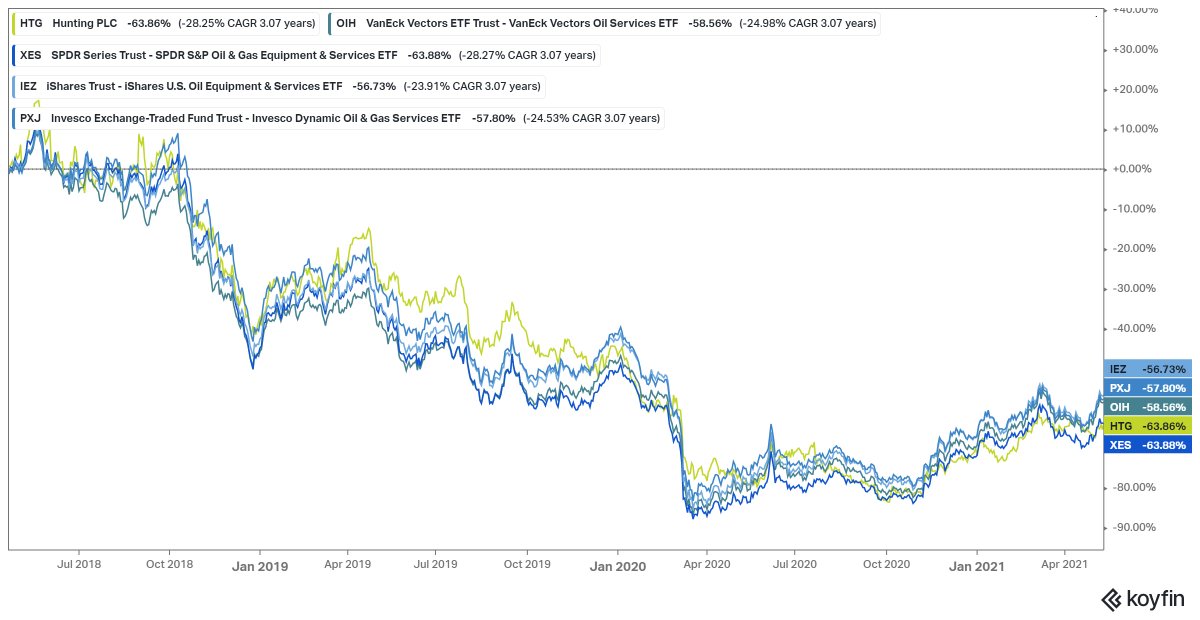

What a difference a year makes.. but an albatross is still an albatross although #BOKU are coming to discover that theirs performs more like a turkey

https://twitter.com/hareng_rouge/status/1070618827510214657

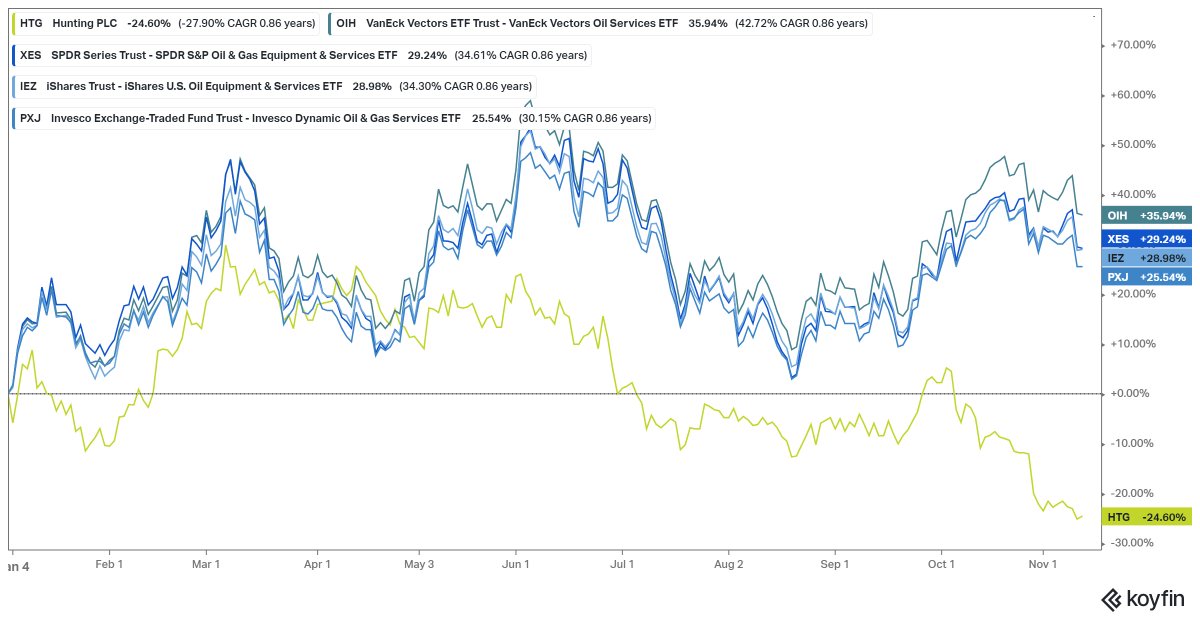

What a difference a week makes.. #BOKU

I've noticed this with the UK market and it isn't just Boku: you get told one thing in one form of words, then later on the same thing in a different form of words and the market reacts as if it's new.

I've noticed this with the UK market and it isn't just Boku: you get told one thing in one form of words, then later on the same thing in a different form of words and the market reacts as if it's new.

Here are this year's results from #BOKU:

Payments 19: $43.5M (+23%) / TPV $5.0B (+38%) = 0.87%

Payments 18: $35.3M (+44%) / TPV $3.6B (+112%) = 0.98%

Payments 17: $24.4M / TPV $1.7B = 1.44%

Payments 19: $43.5M (+23%) / TPV $5.0B (+38%) = 0.87%

Payments 18: $35.3M (+44%) / TPV $3.6B (+112%) = 0.98%

Payments 17: $24.4M / TPV $1.7B = 1.44%

"Scale is not just about bragging rights.. Despite the fact that volumes have increased so fast, operating expenses have stayed reasonably stable. The incremental cost of processing each new extra transaction is negligible. New revenue falls through to the bottom line."

Amongst the blizzard of BS ("The World is Flat, and Hedgehogs are beating Foxes") in the #BOKU results, I can't pretend I know what "adjustment for previous year cash items" actually means but suppose the headline figures look a touch better for it.

Having spent the last couple of years constructively shitposting on Boku, I think the acquisition that they just announced may be something quite interesting.

The figures are buried in pages 5 & 6 of this inviting looking announcement

The figures are buried in pages 5 & 6 of this inviting looking announcement

Here are those numbers, along with their results naively glommed onto Boku's

Fortumo is another DCB biz and as you see, it appears to be very profitable compared to others in the space as well as the parent.

Googling around, there's quite a bit of (positive) newsflow around this company; a fortnight ago - payments for Fortnite

forte.delfi.ee/news/tarkvara/…

Googling around, there's quite a bit of (positive) newsflow around this company; a fortnight ago - payments for Fortnite

forte.delfi.ee/news/tarkvara/…

#BOKU update

Payments H1/20: $22M (+14%) / TPV $3.1B (+36%) = 0.71%

Usual selection of jazz quotes, s-curve references and nonsense.

"The company has seen a boost in the adoption of digital services during the pandemic "

ID / Danal still a disaster

Payments H1/20: $22M (+14%) / TPV $3.1B (+36%) = 0.71%

Usual selection of jazz quotes, s-curve references and nonsense.

"The company has seen a boost in the adoption of digital services during the pandemic "

ID / Danal still a disaster

https://twitter.com/hareng_rouge/status/1243077984946438144?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh