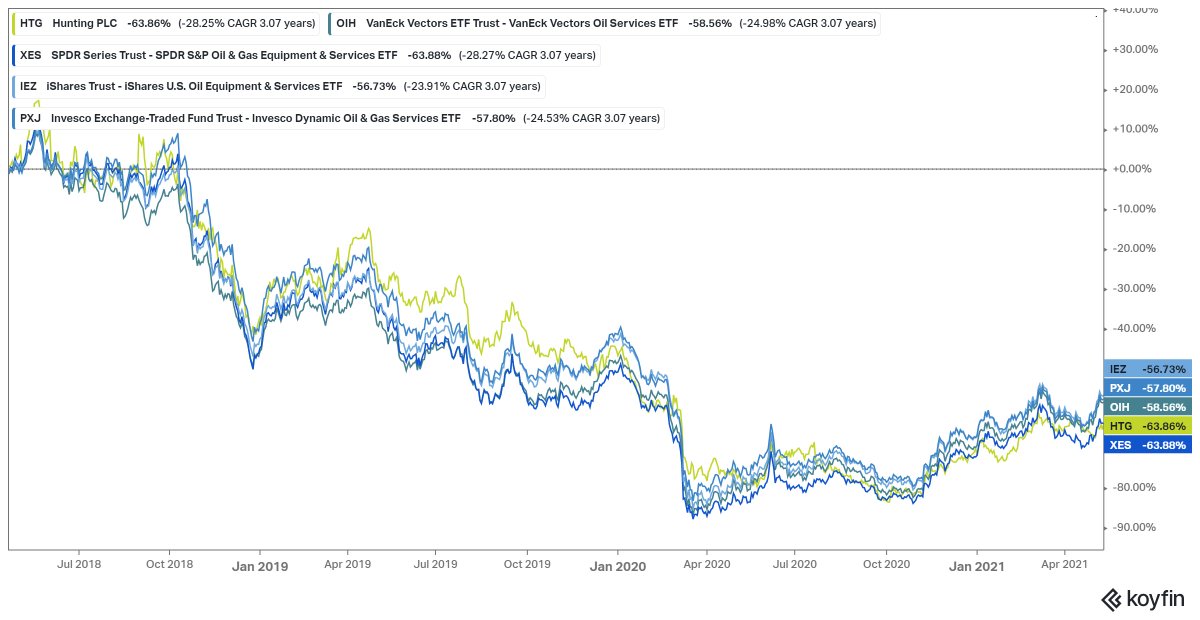

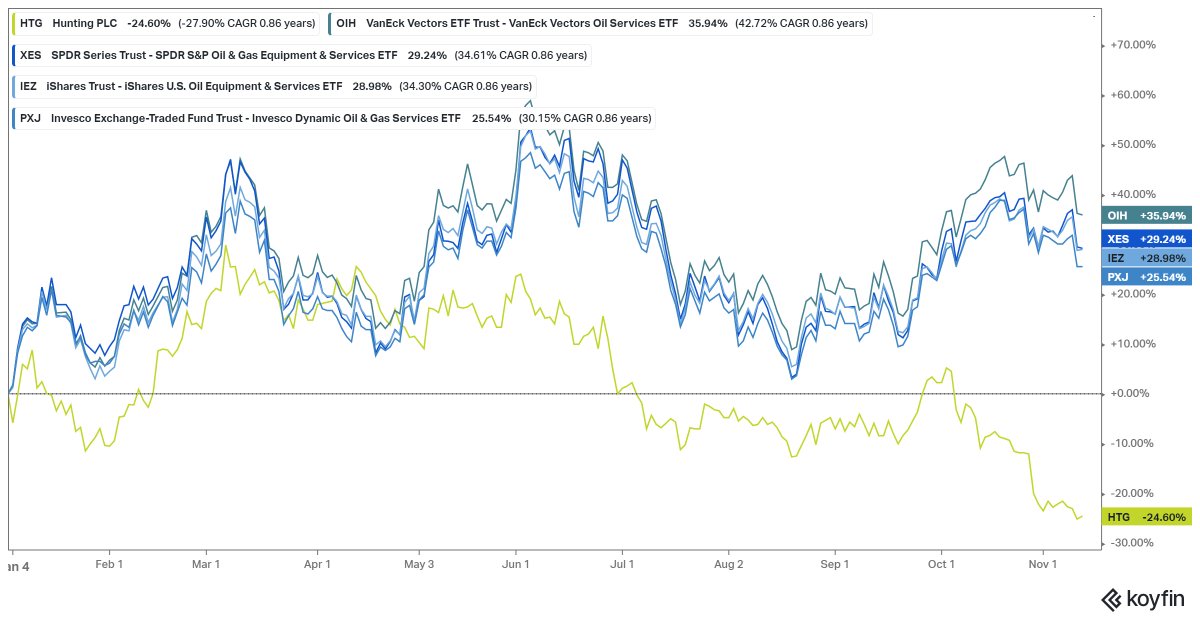

Here's a very simple idea and thread for a play on #Coronvirus and an oil price war: the nitrogen complex - because as well as Corona, China and Iran are also major exporters of Urea.

China was the marginal producer. Here's what #CF CF Industries said on their last call on China

China was the marginal producer. Here's what #CF CF Industries said on their last call on China

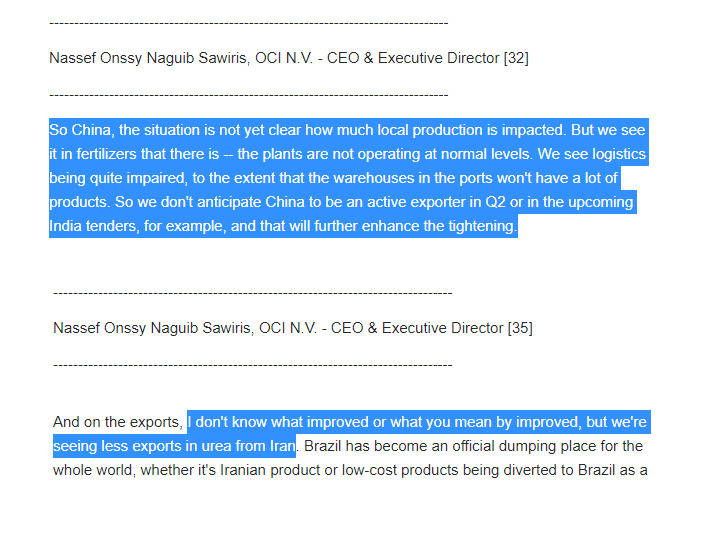

Here's what OCI said regarding China and Iran

Here is what the price of Urea has done during corona. Profercy note China is absent from the export market.

Gas is the Western feedstock whereas China uses anthracite coal. Gas is cheap and getting cheaper. Here's #CF industries sensitivity to cheaper gas and more expensive urea. Further catalyst is the annual Indian tendering in a couple of weeks or so. #CF and peers should overearn.

• • •

Missing some Tweet in this thread? You can try to

force a refresh