That's my baby.

Part-ownership in companies only.

Close to no cash.

Roughly one third in Chinese companies.

Rest mostly USA.

One thing that's unusual here is number of stocks. Sligthly ashamed to admit, but I'm gradually going into direction of Walter Schloss amounts of stocks.

Part-ownership in companies only.

Close to no cash.

Roughly one third in Chinese companies.

Rest mostly USA.

One thing that's unusual here is number of stocks. Sligthly ashamed to admit, but I'm gradually going into direction of Walter Schloss amounts of stocks.

While I get the concept of "Slugging", I've seen too many investors buy large positions that go down >50%.

I'm maximizing "hit ratio" currently. I need lots of opportunities to answer "did I analyze this opportunity correctly and make money?" thus I own lots of companies.

I'm maximizing "hit ratio" currently. I need lots of opportunities to answer "did I analyze this opportunity correctly and make money?" thus I own lots of companies.

By doing so I'm essentially growth-hacking investment experience of decades into years by simply owning & experiencing more individual situations.

Constantly learning about huge numbers of companies and owning a lot of them aligns well with only being into investment since 2.5y.

Constantly learning about huge numbers of companies and owning a lot of them aligns well with only being into investment since 2.5y.

There are >65,000 public companies out there. I try to find the top 1% & I'm strictly following Buffett's "reading from A-Z" approach.

If you apply some filters, like insider ownership & or maybe "involvement of Founder", you really can study almost everything that's out there.

If you apply some filters, like insider ownership & or maybe "involvement of Founder", you really can study almost everything that's out there.

Another thing about owning lots of companies: Holding them is psychologically easier.

It's more modest, too: It's more about their performance, less about the portfolio manager's ingenuity of trading around.

My performance = companies' long-term performance, not me day-trading.

It's more modest, too: It's more about their performance, less about the portfolio manager's ingenuity of trading around.

My performance = companies' long-term performance, not me day-trading.

Owning those wonderful companies stocks' for me is my way to show respect to the people who run these companies. People with whom I'm in awe with.

Me not expecting my performance to come from trading is the same side of the coin for me: It's about the companies & their people...

Me not expecting my performance to come from trading is the same side of the coin for me: It's about the companies & their people...

Me owning lots of companies also is influenced by "right-sidedness" out outcomes, typical in venture capital.

Most painful for me would be missing out on future tenbaggers. Even if initial position is small, I believe enough right-side exposure will drive meaningful returns.

Most painful for me would be missing out on future tenbaggers. Even if initial position is small, I believe enough right-side exposure will drive meaningful returns.

If you own lots of companies, your idea of valuation is "concrete" because you know every data point of all your companies & you constantly have to think about what's relatively cheap.

-> Less risk because you're not operating in a vacuum, but always know relative valuations.

-> Less risk because you're not operating in a vacuum, but always know relative valuations.

Lastly, my approach in owning lots of companies fits my personality & background. I love to learn, analyze a lot, love to "know" and I love to be right about things (for better & worse).

My background is "book person" and "philosophy".

I'm expecting to outperform analytically.

My background is "book person" and "philosophy".

I'm expecting to outperform analytically.

Outperforming analytically doesn't mean 1% of knowledge about companies.

Investment community is becoming aware of negative dialectics of the concept of "circle of competence".

World is way, way more complex than 50y ago. Good luck staying in your comfort zone.

Investment community is becoming aware of negative dialectics of the concept of "circle of competence".

World is way, way more complex than 50y ago. Good luck staying in your comfort zone.

My approach: "Inverted circle of lesser incompetence".

I'm constantly way beyond my "circle of competence" and it's a feature. Being top 1% with one company might protect you, but reality is moving too fast. Too much time and energy required to be top 1% with a single company.

I'm constantly way beyond my "circle of competence" and it's a feature. Being top 1% with one company might protect you, but reality is moving too fast. Too much time and energy required to be top 1% with a single company.

Think this quote from Jeff Bezos also applies to investing:

-> Reading about as many companies as possible -> training pattern recognition -> working by the negative art of stock picking, namely exclusion.

Assume all Co's are awful.

Buy the least awful one you can find.

My $JD writeup imho is a solid example of negative stock picking.

Assume all Co's are awful.

Buy the least awful one you can find.

My $JD writeup imho is a solid example of negative stock picking.

Imo one thing that separates amateur investing from pro investing is that pro investors know that indeed, most companies are awful. Most companies will give you horrible returns long-term.

Thus 180° change of perspective follows: PLEASE DON'T try to stock pick positively.

Thus 180° change of perspective follows: PLEASE DON'T try to stock pick positively.

Noobs don't realize that the stock market, from the perspective of investor returns, is a bag of turds with some raisins that are hidden in between.

They just stick their hands in that bag and they get what they deserve.

They just stick their hands in that bag and they get what they deserve.

Stock picking is a dirty endeavor. Not only are you separating turds and raisins all the time, but even if you're pro enough to view the stock market as a bag of turds and try hard to NOT GRAB TURDS by "via negativa", you _still_ grab them quite often.

...Just not as often as retail turd-baggies that believe the stock market is a bag of raisins that contains some turds here and there.

BTW: Microcap level is not a great place for your first year(s) in investing.

Certainly >10x turd:raision ratio vs e.g. in the S&P500.

Anyway.

BTW: Microcap level is not a great place for your first year(s) in investing.

Certainly >10x turd:raision ratio vs e.g. in the S&P500.

Anyway.

Outperforming analytically? Companies that "need to be understood", stuff that is highly impactful in real world, but doesn't always show in numbers, thus also hopefully gives me an edge in an investment age that will be even more dominated by AIs.

Examples of portfolio companies that "need to be understood":

$AMZN, $LVGO, $JD, $TCEHY, $3690.HK, $WORK, $ESTC, $HMI, $NTDOY, $SPOT, $PDD, $TWTR, $XPEL - most of them need "taste" & some form of philosophy about where our world is going and its driving historical forces.

$AMZN, $LVGO, $JD, $TCEHY, $3690.HK, $WORK, $ESTC, $HMI, $NTDOY, $SPOT, $PDD, $TWTR, $XPEL - most of them need "taste" & some form of philosophy about where our world is going and its driving historical forces.

(just some examples, not giving away several favorites)

Also, generally, how I view my job as a PM. I already said that it's about companies' performance.

Personally, I interpret the role of a PM quite analytical. Because that's an interpretation I feel relatively adequate for.

Also, generally, how I view my job as a PM. I already said that it's about companies' performance.

Personally, I interpret the role of a PM quite analytical. Because that's an interpretation I feel relatively adequate for.

This means that my job as a risk manager is not necessarily to hedge things or trade around but by out-thinking before events like e.g. Corona happen.

My job would have been to own companies that fare well in disruption of physical & capital infrastructure.

How am I doing there?

My job would have been to own companies that fare well in disruption of physical & capital infrastructure.

How am I doing there?

* most portfolio companies profitable / breakeven, most fortress net cash balance sheets. Almost no company that has lots of debt. Why would a top 1% company (where most long-term returns come from) have lots of debt anyway? Simple as that.

* I own $LVGO and $HMI long before Coronavirus. Both companies are thematic plays on digital healthcare platforms.

When I look at those companies from my "at scale" perspective, they would be very meaningful in solving Coronavirus early. -> Aligned with society.

When I look at those companies from my "at scale" perspective, they would be very meaningful in solving Coronavirus early. -> Aligned with society.

* I own $JD that was born in its current form during SARS crisis 2003... JD really thrives during current virus. Built for this.

Is this luck, or is this solid portfolio management? We'll see over longer periods of time, during many more periods of distress. But so far, so good.

Is this luck, or is this solid portfolio management? We'll see over longer periods of time, during many more periods of distress. But so far, so good.

I'm long bits and not very long atoms, except e-commerce and online-to-offline companies.

(e.g. $TCEHY, $SFTBY, $AMZN, $FB, $NTES, $NTDOY, $DOYU, $YY, $HUYA, $BEST, $SPOT ) Feel good about them (and my choices) on a relative basis vs current situation.

Thanks for reading! <3

(e.g. $TCEHY, $SFTBY, $AMZN, $FB, $NTES, $NTDOY, $DOYU, $YY, $HUYA, $BEST, $SPOT ) Feel good about them (and my choices) on a relative basis vs current situation.

Thanks for reading! <3

2nd pic is a snippet from my text from 17.03.2020 ( & drive.google.com/open?id=1BLVq6… )

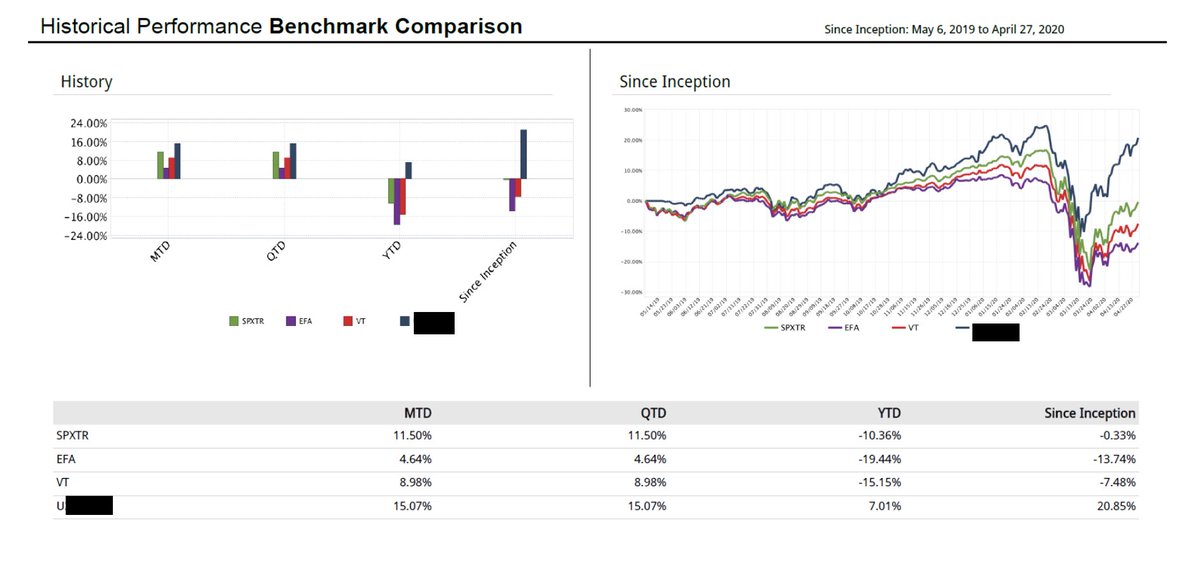

Performance is not coming from concentration, I'm long >100 companies.

Performance is not coming from concentration, I'm long >100 companies.

I believe it was helpful that - even though I also make exceptions here and there - for the vast majority I own growing ~profitable companies with net cash balance sheets in growing markets with above avg company & employee cultures that are led by founders with skin in the game.

I mean you can just read all my tweets and analyze the stuff I've mentioned. $WORK works, $LVGO is 2x for me as of ~today (not selling a single share!), $ETSY is >2x, still long 15 $ZM from $67.872 (yep), $JD (so many sold & talked about it in their letters, I'm still holding)...

$AMZN, $FB, $GOOG, $TWTR, $NTDOY, $SFTBY, $TCEHY, $3690.HK, $SPOT - you get the point. I think my alpha spread vs indices is probably going to shrink from its current number but let's be clear: I didn't even know about investing <3y ago. I'm okay if I perform like SPY next years.

I would love to highlight that my performance also isn't based on microcaps. If one ignores psychological factors (surely a kind assumption), ceteris paribus >90% of my performance from 06.05.2019 (incept. of relevant port.) until here could have happened with >$50mn in AUM, too.

Why?

1. Internet & tech benefiting scale

2. Cost of capital (also influenced by money printing governments) disadvantages smallcap more than my competition thinks

(If u REALLY think inflation is only 2%/y when governments bail out airlines, mb you should work for a central bank)

1. Internet & tech benefiting scale

2. Cost of capital (also influenced by money printing governments) disadvantages smallcap more than my competition thinks

(If u REALLY think inflation is only 2%/y when governments bail out airlines, mb you should work for a central bank)

3. I'd honestly attribute up to half of my alpha to the macro (!) belief that current investing isn't about finding things that make sense based on current earnings multiples.

Absolute amounts of net profits are an optical illusion when governments just make up their own money.

Absolute amounts of net profits are an optical illusion when governments just make up their own money.

I have no idea how much money governments are actually printing but one doesn't see a black hole either.

Owning companies that care a lot more about future earnings power (disruptive scale-sharers & innovative breakeven growers) vs current one (cash cows) makes sense to me.

Owning companies that care a lot more about future earnings power (disruptive scale-sharers & innovative breakeven growers) vs current one (cash cows) makes sense to me.

I hope you realize that I'm experimenting with essentially everything! Whenever I bought something for less than 4x FCF without too much hair, it was stressful and it never seemed to work the way it "should". There's almost always this factor X that makes those cases super hard.

I'd attribute another part of my performance to simply learning about as many companies as possible.

Can't say it often enough but actual valuation work imo isn't looking at one company abstractly and doing a DCF or something, instead:

Can't say it often enough but actual valuation work imo isn't looking at one company abstractly and doing a DCF or something, instead:

You concretely learn about thousands of companies at the same time and simply compare everything.

This develops taste about what you can trust because you are comparing. I mean, is it surprising to find actual cheapness when one actually compares thousands of companies?

This develops taste about what you can trust because you are comparing. I mean, is it surprising to find actual cheapness when one actually compares thousands of companies?

Also a differentiator not only vs retail but also pros.

Too manual, too time-intensive.

Chances are that you're too old and you have too many other things going on in your life to actually look at companies.

Lot's of time-intensive grind + Sitzfleisch (German for "iron butt")

Too manual, too time-intensive.

Chances are that you're too old and you have too many other things going on in your life to actually look at companies.

Lot's of time-intensive grind + Sitzfleisch (German for "iron butt")

Last week I looked into:

(folder now has 1,710 sub folders, each with files in it. 13.7GB & 21,031 manually sorted files)

I generally say I have no: process, assumptions, planing, timetables or anything "fixed", but I'm building a data base here that will serve me over time.

(folder now has 1,710 sub folders, each with files in it. 13.7GB & 21,031 manually sorted files)

I generally say I have no: process, assumptions, planing, timetables or anything "fixed", but I'm building a data base here that will serve me over time.

essentially Buffett's A-Z process + tech.

Poor Buffett didn't have the tech to collect info, but luckily he has this wonderful memory.

1) read a lot (only ~65,000 pub co's!) 2) sort a lot 3) develop concrete filters based on current reality which is only possible as practicioner

Poor Buffett didn't have the tech to collect info, but luckily he has this wonderful memory.

1) read a lot (only ~65,000 pub co's!) 2) sort a lot 3) develop concrete filters based on current reality which is only possible as practicioner

4) get a sense for the exceptional, unique, wonderful, shocking and best by comparing.

Happens that I buy positions after half a day because everything just feels WAY above avg & if u simply trust companies' guidance CAGR should be nice: $FTNT or $ADSK (tiny positions but long)

Happens that I buy positions after half a day because everything just feels WAY above avg & if u simply trust companies' guidance CAGR should be nice: $FTNT or $ADSK (tiny positions but long)

I'm fully aware that I own many popular names.

Often it seems that retail folks only know a handful of companies. It's risky that way. (even though there's lots of intuitive traders' smartness present!)

But I really can say that I mostly decided against alternative options.

Often it seems that retail folks only know a handful of companies. It's risky that way. (even though there's lots of intuitive traders' smartness present!)

But I really can say that I mostly decided against alternative options.

My JD writeup continues to be my fav example if you want to learn more about my primary approach in regard to stock picking: negative stockpicking. (I chose JD over dozens of concrete other opportunities)

Also, if you really know "how big things are" you can get much more ...

Also, if you really know "how big things are" you can get much more ...

comfortable with mcaps of seemingly "expensive" things.

E.g. the biggest publically traded Chinese banks are >$1tn in mcap. I can squeeze in a LOT of SaaS companies that seem abstractly expensive. I just view it differently.

Concrete thinking example:

E.g. the biggest publically traded Chinese banks are >$1tn in mcap. I can squeeze in a LOT of SaaS companies that seem abstractly expensive. I just view it differently.

Concrete thinking example:

Not an expert on $CRM but I think $CRM at ~$145bn mcap has a good chance to outperform Industrial and Commercial Bank of China at $385bn mcap - even though if you assume market efficiency you actually assume that both should return exactly the same going forward.

Somebody asked me about valuation (+concerns) in regard to my $ESTC investment (long @ sligthly below $5bn mcap). I look kinda stupid, but my honest answer is that their mcap isn't very big based on the fact that I've looked at many hundreds of cringy companies with higher mcaps.

Again, there's zero excel modeling in there. It absolutely is a quality judgement call. I'm trusting my quantitative gut feeling comparing to numbers & sizes of other companies.

Also, I protect myself with position sizing. $ESTC is 1%. For me this is a very big position.

Also, I protect myself with position sizing. $ESTC is 1%. For me this is a very big position.

Feel free to make fun of me for saying that 1% is a very big position. But think of the effects of having so many positions:

1. You don't get in trouble with individual mistakes.

2. You could buy more if something goes down a lot.

3. You're overwhelmed in a positive way.

1. You don't get in trouble with individual mistakes.

2. You could buy more if something goes down a lot.

3. You're overwhelmed in a positive way.

4. You totally accelerate into research & learning.

5. You get super fast in analyzing one company after the other.

6. You actually know what's out there & get macro sense.

7. You can own companies with certain risks, e.g. country risk (e.g. $STNE or $PAGS or Chinese companies)

5. You get super fast in analyzing one company after the other.

6. You actually know what's out there & get macro sense.

7. You can own companies with certain risks, e.g. country risk (e.g. $STNE or $PAGS or Chinese companies)

8. You are forced to think long-term and look for ultra-long term mega compounders, something I strongly believe in. If I get even one 100x on a 1% position (of my >100 companies) performance of whole portfolio is alright.

9. I'm not easy to clone

9. I'm not easy to clone

10. Holding is easier because it's not actually easy to recycle THAT quickly into other cheap high quality companies. For example I bought $ETSY at ~$31 (btw entirely enabled by following "everything" ) & I haven't sold here because the initial position was way below 0.5%.

11. If you're new to investing, you need experience, thus you need skin in the game, even if it's smaller percentages than usual (again, also protects me!). I think I'm simply learning more.

I would do the same even if I would perform ~worse than the market in the short-term.

I would do the same even if I would perform ~worse than the market in the short-term.

12. Simpler and less stressful way to get to a point where one feels absolutely confident to prefer the companies where one has worked on ~absolutely alone.

Investing isn't supposed to be easy. You have to first survive until you get to a point where you can rely on yourself.

Investing isn't supposed to be easy. You have to first survive until you get to a point where you can rely on yourself.

I think I'm getting there. For me, companies where I worked "completely alone" (= definitely not buying things because someone else is long) actually seems to work better for me now (for example $3690.HK, $LVGO, $WORK, $HMI) and I got there because I didn't screw up early.

At least for my first whole year of investing - even though I did it absolutely 24/7 of my own investible, personally available time & gave my best - I was quite value destructive.

Even after 1.5y (last AL) my filters weren't good enough: e.g. Freshii (no position since ~ >1y)

Even after 1.5y (last AL) my filters weren't good enough: e.g. Freshii (no position since ~ >1y)

Even today my position sizing is respecting my assumption that I lack experience.

(For a very brief moment in time I had 20% in FCAU, obviously not a good idea in retrospect, as of today. m) )

Hope to be around for some time. If lack of concentration is a problem, I can change.

(For a very brief moment in time I had 20% in FCAU, obviously not a good idea in retrospect, as of today. m) )

Hope to be around for some time. If lack of concentration is a problem, I can change.

Digital transformation accelerated & internet companies are the eye of the needle that the world has to go through.

Those businesses benefit non-linearly, in a compounded manner whilst other, weaker pre-internet & often close to mere subsistence businesses are hurt non-linearly.

Those businesses benefit non-linearly, in a compounded manner whilst other, weaker pre-internet & often close to mere subsistence businesses are hurt non-linearly.

Last months every day was both a tightrope sprint & marathon!

Mentally, definitely the hardest period of managing solid sums of money for me so far because headline sentiment reads:

"unemployment worst since great depression"

"A dangerous gap - the markets v the real economy".

Mentally, definitely the hardest period of managing solid sums of money for me so far because headline sentiment reads:

"unemployment worst since great depression"

"A dangerous gap - the markets v the real economy".

Was not intuitive to stay 100% long but it was imo highly rational & justified by "reality".

Investors remain skeptical, but it seems market as a supra-individual quasi-sentient emergent being is understanding value of antifragile digital transformation companies better now.

Investors remain skeptical, but it seems market as a supra-individual quasi-sentient emergent being is understanding value of antifragile digital transformation companies better now.

(Yes, this diminishes prospective returns bc change of perspective, market's understanding of anti-fragility of internet vs fragility of physical is not recurring, - even though one can and should still argue if it's enough already, for example: $FB & $GOOG vs $KO & $PG)

As long as there are still people that write about "the real economy", you can derive from that that we're essentially in a comparable period to the invention of the printing press, a truly remarkable time of "before" and "after".

Staying long & focused:

E-comm ~ <20% of retail.

Staying long & focused:

E-comm ~ <20% of retail.

Will I be able to keep up my alpha spread?

Yes, if some companies get more respect as well, mostly smaller, US-listed "Chinese" companies: $MOMO, $DOYU, $YY, $BEST, $TME. Oh, & Softbank. $BABA, unlike $AMZN isn't around ATHs, arguably it should.

If Softbank performs, so do I.

Yes, if some companies get more respect as well, mostly smaller, US-listed "Chinese" companies: $MOMO, $DOYU, $YY, $BEST, $TME. Oh, & Softbank. $BABA, unlike $AMZN isn't around ATHs, arguably it should.

If Softbank performs, so do I.

Still bullish on $BABA & $TCEHY.

Compare $TCEHY to $V. (Has worked whole last y since I mentioned this!)

Compare $BABA to $IDCBY ($370bn mcap)

Tencent+Baba+JD+Meituan = less mcap vs five biggest Chinese banks iirc.

You want to beat the market? Imho this is all you need to know.

Compare $TCEHY to $V. (Has worked whole last y since I mentioned this!)

Compare $BABA to $IDCBY ($370bn mcap)

Tencent+Baba+JD+Meituan = less mcap vs five biggest Chinese banks iirc.

You want to beat the market? Imho this is all you need to know.

Imagine living around 1820 and being literate. (estimates of ~12% world literacy rate for that time)

What do you feel for non-literate people? Shame? Guilt?

You probably don't tell them they are worse off in most (but not all!) aspects of their live because they can't read.

What do you feel for non-literate people? Shame? Guilt?

You probably don't tell them they are worse off in most (but not all!) aspects of their live because they can't read.

Same bifurcation: Because we KNOW offline is worse off, we ideologically at least call it "the real economy". (false flattery)

This "REAL economy" thing as a THING (a something that few people question) shows that we might repeat the internet surge of the 90s since the 2010s.

This "REAL economy" thing as a THING (a something that few people question) shows that we might repeat the internet surge of the 90s since the 2010s.

Why are we back to the 90s?

"Dotcom period" was abstract idea but "in itself" correct!

Cloud is concrete reality more than ever.

2020 market simply said NO to the viewpoint "But the real economy is bad".

Ofc this view is just as ideological, but it's directionally right.

"Dotcom period" was abstract idea but "in itself" correct!

Cloud is concrete reality more than ever.

2020 market simply said NO to the viewpoint "But the real economy is bad".

Ofc this view is just as ideological, but it's directionally right.

"Directionally right" means that many specific companies indeed were unsustainably cheap vs their high quality & the fact that they're the inevitable future which just got pulled forward.

This is a matter of concrete discussion of valuations though.

This is a matter of concrete discussion of valuations though.

There should be no gap between philosophical thoughts and specific valuation work (theory=praxis), thus:

Take $ADSK.

Traded for ~$28bn mcap in March. Company's 2023 target: $2.3bn FCF.

Compare that to utility & consumer staples... Can you buy Cola for <13x 3y forward FCF? $KO

Take $ADSK.

Traded for ~$28bn mcap in March. Company's 2023 target: $2.3bn FCF.

Compare that to utility & consumer staples... Can you buy Cola for <13x 3y forward FCF? $KO

People who understood market's change of perspective, got rewarded and people who bought non-internet businesses (potentially driven by guilt and shame) didn't.

Internet = New World / America

Offline = Old World / Europa

Reality moves in a direction & it's digital reality.

Internet = New World / America

Offline = Old World / Europa

Reality moves in a direction & it's digital reality.

Yes, everything of this is highly reflexive. Inevitable direction is digital, but enitrely possible to take a lot of steps backwards (in "non-market" reality & markets).

But so many businesses just OBVIOUSLY became way more valuable, typically the large ones that gain share.

But so many businesses just OBVIOUSLY became way more valuable, typically the large ones that gain share.

Some feel guilty buying AMZN vs local book store.

Amazon simply is worth more after Corona vs before.

Market is rational, it's just probably not fashionable to say this bc of actual harm caused to non-competitive small businesses & their people.

Amazon simply is worth more after Corona vs before.

Market is rational, it's just probably not fashionable to say this bc of actual harm caused to non-competitive small businesses & their people.

Only moral thing in the 1820s would have been to help a person become literate. (no blame or shame)

Same for today, don't feel guilty for being a digital business, your moral job is to help everyone successfully transition.

Most people now are somewhat literate. Better planet!

Same for today, don't feel guilty for being a digital business, your moral job is to help everyone successfully transition.

Most people now are somewhat literate. Better planet!

Digital businesses are the eye of the needle precisely because apparently we're still early into this internet transformation.

Imagine a catastrophe in the 1820s where everyone suddenly had to learn how to read. Bullish or not?

Can you blame the market for bouncing solidly?

Imagine a catastrophe in the 1820s where everyone suddenly had to learn how to read. Bullish or not?

Can you blame the market for bouncing solidly?

Some people came to Silicon Valley & thought they missed everything.

When I learned about investing I thought:

"would have loved to invest in the 90s "internet boom", an era comparable to invention of printing press"

Then I understood: I am alive during EARLY internet epoch.

When I learned about investing I thought:

"would have loved to invest in the 90s "internet boom", an era comparable to invention of printing press"

Then I understood: I am alive during EARLY internet epoch.