Yesterday the Governing Council @ecb took important decisions, further easing the liquidity conditions for banks & fostering lending to the economy. Philip Lane provides a comprehensive explanation of the macro environment & our measures in a recent blog post. #ECBexplains 1/12

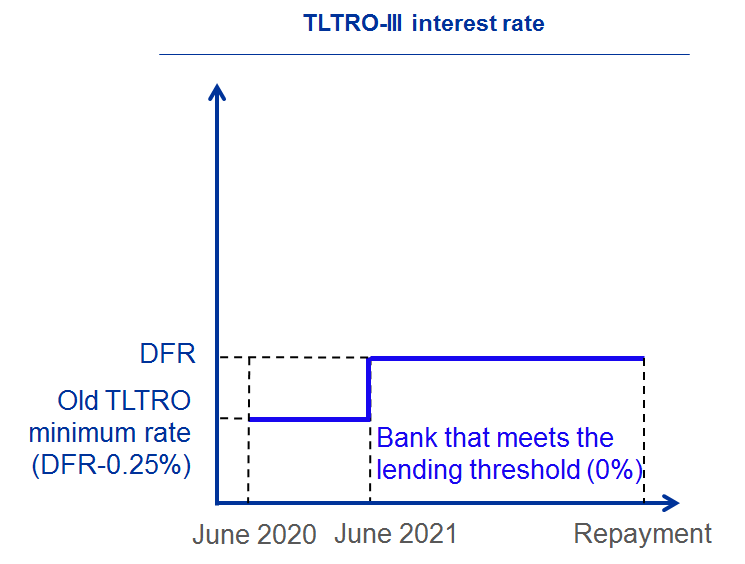

I will add some technical explanations, starting with the #TLTROs, our targeted longer-term refinancing operations. This graph shows the rates for a bank that met the lending threshold of 0% under the old TLTRO (12 March), giving rise to more favourable rates. 2/12

Under the new TLTRO (30 April), banks meeting the lending threshold of 0% pay even lower rates in the “pandemic period”: currently -1% (versus -0.75% before). The assessment period for the lending threshold now starts one month earlier to reward lending in March. 3/12

Under the old TLTRO (12 March), a bank that did not meet the lending threshold of 0%, but met the old lending criterion, calculated over two years, would have gotten the DFR over the entire period. Note that this bank is never worse off than before the changes of 12 March. 4/12

Under the new TLTRO (30 April), conditions are the same, but the required lending threshold, calculated over two years, is proportionally reduced to 1.15%, reflecting the difficulty to expand lending during the pandemic. 5/12

Under the old TLTRO (12 March), a bank that did not meet any lending criterion, would have gotten the old TLTRO entry rate (-0.25%) during the “pandemic period”. 6/12

Under the new TLTRO (30 April), a bank that did not meet any lending criterion, gets the new TLTRO entry rate (currently -0.50%) during the “pandemic period”. 7/12

This graph summarizes the TLTRO conditions under the old decision (12 March)… 8/12

… while this one shows the TLTRO conditions under the new decision (30 April). 9/12

This graph shows the calendar of the new unconditional PELTROs. Earlier operations have a longer maturity (16 months), but the maturity shortens over time (up to 8 months). Pricing is less attractive than for the TLTROs, which set incentives for lending to the real economy. 10/12

So who could make use of these less attractive operations: (1) banks who hit the TLTRO bidding limits, (2) banks with non-eligible lending (real estate, loans to public entities), (3) banks for whom the TLTROs are operationally too complex. 11/12

Finally, we decided on the granularity of publication for asset purchases under #PEPP. Granular reporting will occur on a bi-monthly basis, starting in June. It will show the decomposition across asset classes & jurisdictions, documenting the flexibility of our purchases. 12/12