Excerpts on Global Macro, Inflation, QE etc from Murray Stahl of @HorizonKinetics who has penned one of the finest investor letters this season (Q1'20) - their portfolios are "rich in certain types of asset-light, low-debt, inflation beneficiary businesses" 1/n

We believe that what’s coming down the road is going to be a reversal of the conditions that existed for the prior three decades; all the accepted wisdom and the statistics and correlations will be out the window. 2/n

Understanding that is probably the single most important preparation any investor can undertake right now.. Not only hasn’t the impact of the pandemic altered the course of those trends and risks, it is accelerating and magnifying them. 3/n

On inflation & CPI. Those figures are highly suspect and we believe that they understated the rate of inflation. ...The transparent measure of inflation is the money supply, and that had been rising not at the 2% CPI rate, but at 6%. 4/n

On federal debt leverage : Just a 1%-point increase across all that debt would amount to $760 billion of additional interest expense, effectively a nationwide tax. That’s equivalent to a 3.6% reduction in GDP, a deeper recession than the Credit Crisis recession (3.25%). 5/n

The point of these stats is: the Fed really could not afford to let rates rise, no matter what it might say. So, part of the money creation stats reflected the Fed buying bonds to suppress their prices, and to do so, it needed to create more money– it was monetizing the debt. 6/n

Thus, investors were unwittingly facing a twinned long-term disaster: 1) an insufficient yield on fixed

income securities, more or less 1 or 2 percent, and 2) a real money debasement rate of 6%, and which

was likely to accelerate over time. 7/n

income securities, more or less 1 or 2 percent, and 2) a real money debasement rate of 6%, and which

was likely to accelerate over time. 7/n

Consequently, we emphasized inflation beneficiaries, with a focus on the highest quality or highest contingent return assets we could find. And not just for the year or two ahead, but for the decade or two ahead. 8/n

So that was then. All of those debt and money growth figures I just gave you are now anachronisms. The govt is now spending unimagined quantities of money, and enlarging its B/S on an unimagined scale, in order to support the econ during this mandated shut-down of businesses. 9/n

On Mar 23rd, the Federal Reserve.. made a pretty extraordinary statement. It said that it would spend any amount of money necessary to support the flow of credit to employers, businesses and consumers. On Mar 27th, the $2 trillion stimulus bill was approved – the CARES Act. 10/n

What does $2 trillion mean, in some relatable framework? Far and away the greatest debt/GDP ratio we ever had was in 1946, following the massive 5-year World War II spending. 11/n

If $2 trillion were to be the limit of the current excess spending, and if the economy this year were to shrink by just 2% -- which would be a mild recession – then the U.S. debt/GDP ratio would be the same record 119%. 12/n

But that’s not the half of it; literally. There is $454B allocated for Treasury to make loans and other inv in various kinds of fin assets - via an SPV that the Tsy seeds with some equity capital, and which the Fed tops up with up to 10 times that amt. 13/n

With up to 10:1 leverage, that $454B could easily be another $3T or more... You couldn’t know what the real

value of a Japanese bond would be, since the government made the price. Now the U.S. is doing it. 14/n

value of a Japanese bond would be, since the government made the price. Now the U.S. is doing it. 14/n

It also means that, through the SPV prog, the Treasury is, in a fashion, directing the Fed to create more money. That’s a very big deal.

Now there’s a link that’s never existed before, not one that you could circle on a document, between the White House and the Fed. 15/n

Now there’s a link that’s never existed before, not one that you could circle on a document, between the White House and the Fed. 15/n

So the U.S. budget deficit will be in the many $Trillions. The debt/GDP ratio will balloon to Italy and Greece levels, which means beyond the ability of the economy to grow rapidly enough to allow govt to pay down its debt. 16/n

The only way out is to debase the currency, allowing debt to be repaid over a long period of time with ever cheaper money. It will be a wealth transfer from savers who own bonds to the debtors who borrowed the money. 17/n

Beyond the near term, as an asset class, bonds will be more dangerous than equities, because the

return prospects for bonds are now defined by a binary set of possibilities, neither of which works. There’s no scenario in which investors escape losing money in bonds. 18/n

return prospects for bonds are now defined by a binary set of possibilities, neither of which works. There’s no scenario in which investors escape losing money in bonds. 18/n

The asset allocation models haven’t been revised yet, because they are all backward looking, statistical series-based models.

:

Since the ultimate danger is in the bond market, equities are where the defensive shift needs to be. 19/n

:

Since the ultimate danger is in the bond market, equities are where the defensive shift needs to be. 19/n

There have been only a couple of times in the last century when national life and the world

order have been in such disequilibrium.

Today, a challenge is that governments have so distorted the capital markets that it’s extraordinarily

difficult to construct a portfolio. 20/n

order have been in such disequilibrium.

Today, a challenge is that governments have so distorted the capital markets that it’s extraordinarily

difficult to construct a portfolio. 20/n

First, we don’t doubt that the stock market, at least for the time being, might stabilize, might even go up,

maybe a lot.

So, the stock market might remain elevated, people will be heartened and might feel that the danger is over. 21/n

maybe a lot.

So, the stock market might remain elevated, people will be heartened and might feel that the danger is over. 21/n

But, as my colleague Peter Doyle reminded us recently, through the words of Winston Churchill, that you don’t want to fall victim to this thinking: The danger has not arrived, so the danger has passed. 22/n

The recent market decline did not diminish the index concentration or valuation problem, it actually made

it more extreme.

Indexation has gotten so large that it has become the market, become the marginal trade. 22/n

it more extreme.

Indexation has gotten so large that it has become the market, become the marginal trade. 22/n

And being price-indifferent, it has been establishing its own ever-higher clearing prices in an ever-narrower list of

the largest cos. In the past decade, indexation has not been providing safety via diversification – just ever-increasing concentration and valuation risk. 23/n

the largest cos. In the past decade, indexation has not been providing safety via diversification – just ever-increasing concentration and valuation risk. 23/n

In the past, you can see how a portfolio manager who wanted to beat the S&P during the last 10 years

would have had to not only own that small, 1% group of concentrated stocks, but would have had to

overweight all of them. No way around it. 24/n

would have had to not only own that small, 1% group of concentrated stocks, but would have had to

overweight all of them. No way around it. 24/n

On the likes of Google and Facebook : "Investors will eventually learn that the leading IT companies are becoming slow-growth cyclical." - this was followed by a great commentary on the FANGs & the risks in their biz models. 25/n

We believe there are a couple of shoes that haven’t dropped yet... It will dawn on investors that they’re transitioning from being growth companies to growth-constrained cyclical businesses. 26/n

The second shoe is that something bad is likely to happen in the bond market. It hasn’t yet, because the

government support is just getting under way. 26/n @TaviCosta

government support is just getting under way. 26/n @TaviCosta

We don’t know how all of this will shake out. In about

three months, though, governments will start reporting their budgets. Japan, the U.K. and Canada, for

instance, have March 31st fiscal years. 27/n

three months, though, governments will start reporting their budgets. Japan, the U.K. and Canada, for

instance, have March 31st fiscal years. 27/n

The credit rating agencies, which follow strict parameters, such as debt/GDP ratios, will have to start downgrading sovereign debt. That’s the kind of development that can

alarm investors. 28/n

alarm investors. 28/n

So profound changes are coming. The most profound would be persistent inflation. There has never been a society in history of the world that has been able to avoid serious inflation and debasement of their currency after a surge in money creation. 29/n

..Global supply chains will be pared back - It is almost certain that the U.S. manufacturing base is returning to the mainland, perhaps with government incentives. The cost structure will be a lot higher. In a great reversal, we will, in effect, begin to import inflation. 30/n

This informs the kinds of companies we don’t wish to own as well as what we are looking for. It is typically said that low interest rates support high stock and other financial asset valuations. But it is high inflation that is associated with serious valuation contraction. 31/n

Between April 1971 and March 1980, the inflation rate rose from 4.2% to 14.6%. The trailing P/E ratio on the S&P 500 contracted by two-thirds, from 19.5x to 6.7x.

.. the earnings multiples really were associated with the inflation rate. 32/n

.. the earnings multiples really were associated with the inflation rate. 32/n

So we want companies that have certain qualitative characteristics that will enable them to come out of

this period well, irrespective of the alterations in the economy. It helps if the business has minimal fixed costs that inflation could magnify. 33/n

this period well, irrespective of the alterations in the economy. It helps if the business has minimal fixed costs that inflation could magnify. 33/n

Similarly, it would be good if its OpEx are not much subj to cost inflation either. Obv, a royalty business model is the most emblematic example. But beyond the royalty model, there are other biz that can increase their revenues with very low incremental operating cost. 34/n

Securities exchanges have that characteristic, since their primary cost is the computer trade matching and processing platforms; that’s a fixed, not a variable cost. 35/n

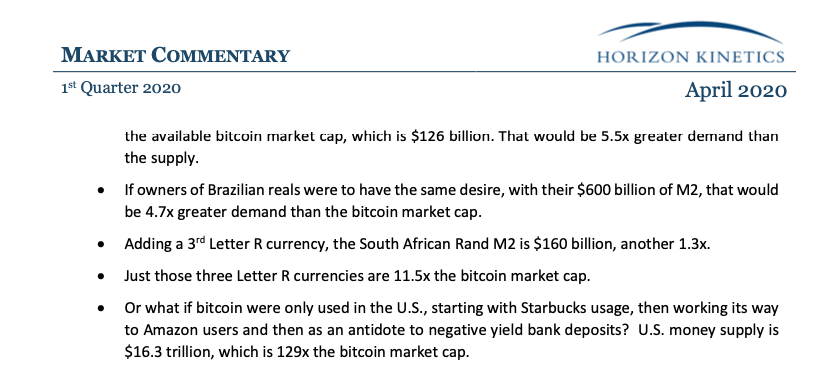

Finally, "The Last Pitch – Changes are Happening – Banks, Brokers and Central Banks" - a superb section on "bitcoin, the most misunderstood of all asset classes". 36/n

Institutional developments in the crypto space worth noting. 37/n

On government cryptocurrency, the Grayscale bitcoin trust and GMO Internet.. 38/n

Last leg of the crypto discussion.

The full letter if you are interested is ~23 pages & is at horizonkinetics.com/wp-content/upl…

39/n

The full letter if you are interested is ~23 pages & is at horizonkinetics.com/wp-content/upl…

39/n