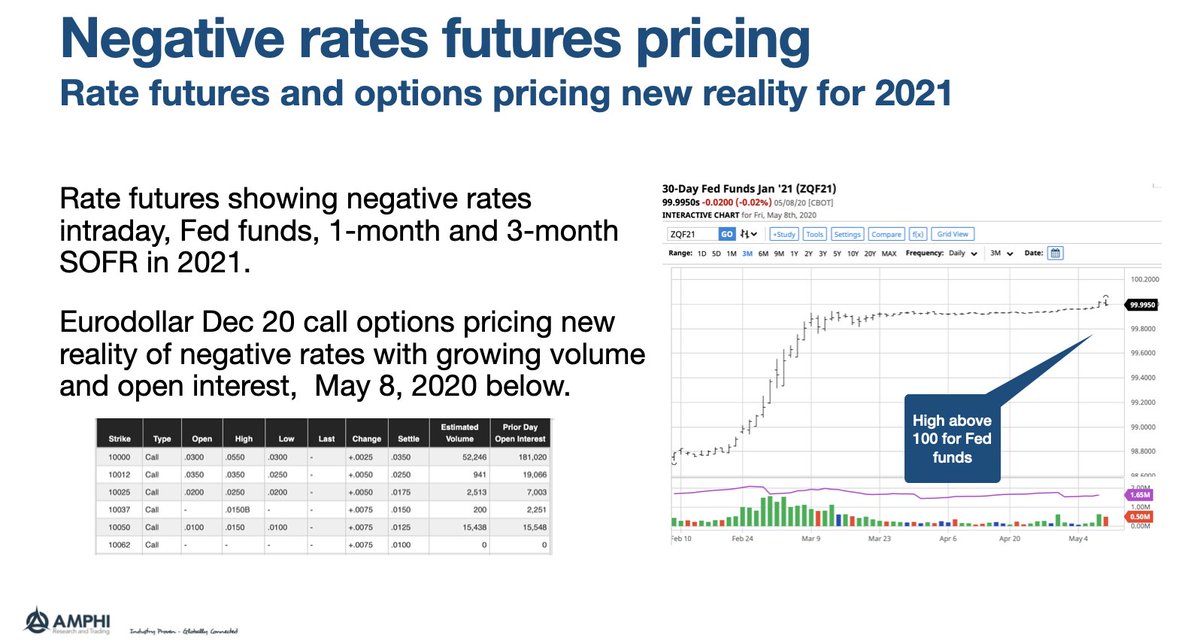

1/ The Rate of Return on Everything (Jordà, Knoll, Kuvshinov, Schularick, Taylor)

"Our new, comprehensive data set includes total returns for equity, housing, bonds, and bills in 16 advanced economies from 1870-2015, revealing new insights and puzzles."

papers.ssrn.com/sol3/papers.cf…

"Our new, comprehensive data set includes total returns for equity, housing, bonds, and bills in 16 advanced economies from 1870-2015, revealing new insights and puzzles."

papers.ssrn.com/sol3/papers.cf…

2/ Returns of single-family homes = capital appreciation + estimated rental yield.

Caveats!

* A national housing index is not investable.

* Appreciation rates and (especially!) rental yields vary from region to region.

* Property taxes are not included (but management fees are).

Caveats!

* A national housing index is not investable.

* Appreciation rates and (especially!) rental yields vary from region to region.

* Property taxes are not included (but management fees are).

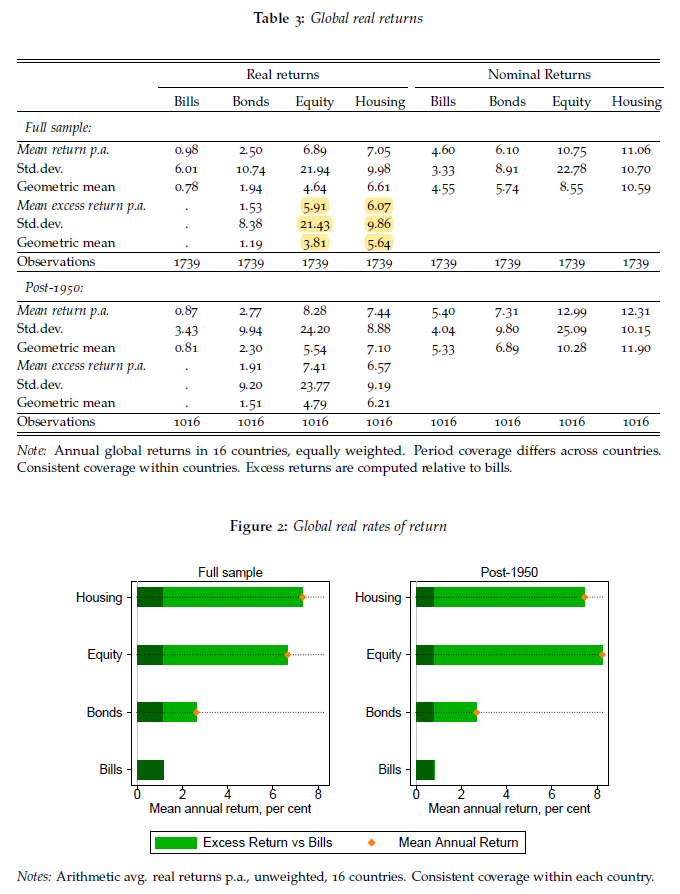

3/ Housing has comparable returns to equities but w/ lower volatility (higher geometric return).

At first, this looks like the low vol factor, but the housing index is not investable. The 10% vol is probably not achievable.

Note the poor risk-adjusted returns of bonds as well.

At first, this looks like the low vol factor, but the housing index is not investable. The 10% vol is probably not achievable.

Note the poor risk-adjusted returns of bonds as well.

4/ The results are robust to GDP weighting (which gives greater weight to the U.S., Japan, and Germany) and to the choice of sample.

5/ "Dropping the two world wars from the sample leaves the main results largely unchanged."

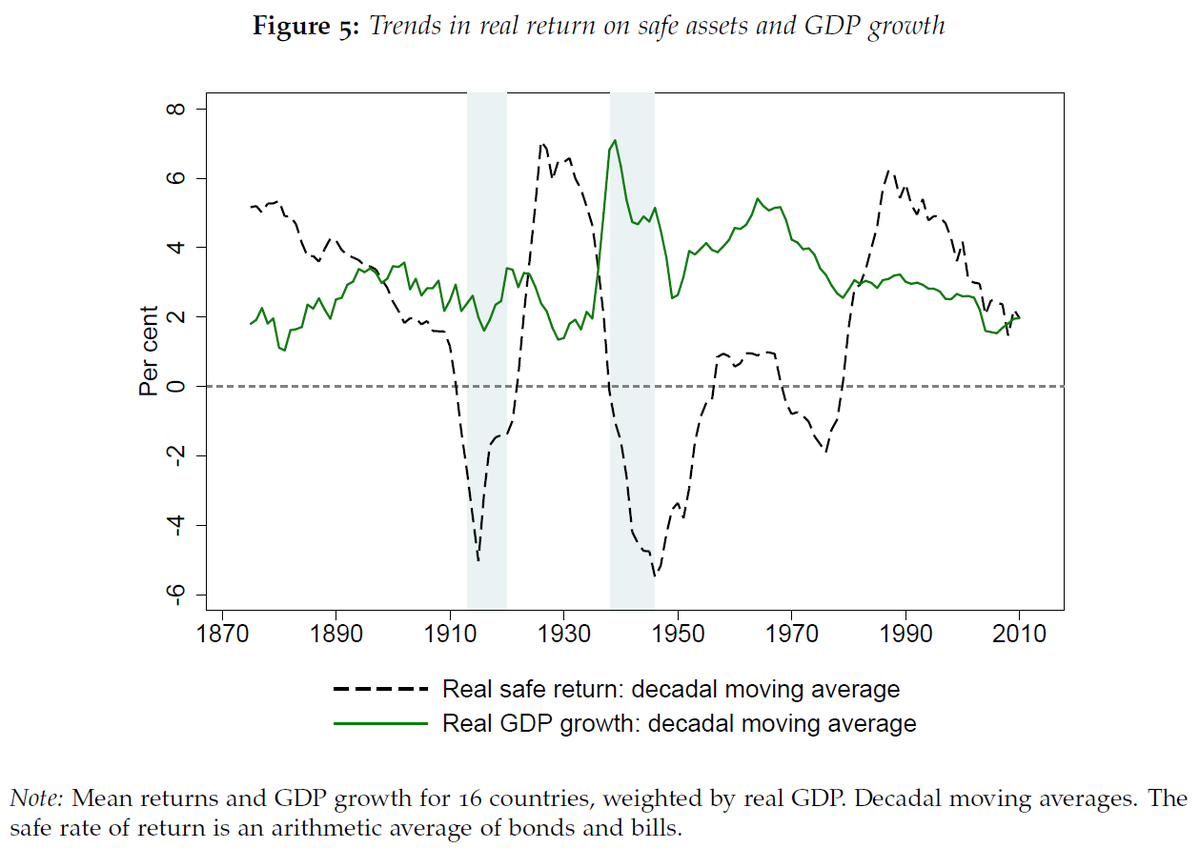

6/ "Low and even negative real rates have been relatively common during modern history.

"Safe rates are as (or more!) volatile than real risky rates. Variation in the risk premium often comes from sharp changes in safe real rates, not from the real returns on risky assets."

"Safe rates are as (or more!) volatile than real risky rates. Variation in the risk premium often comes from sharp changes in safe real rates, not from the real returns on risky assets."

7/ "From a broad historical perspective, high rates of return on safe assets and high term premiums are more the exception than the rule.

"Safe assets offered little protection during high-inflation eras and during two world wars, both periods of low consumption growth."

"Safe assets offered little protection during high-inflation eras and during two world wars, both periods of low consumption growth."

8/ "Bonds and bills have experienced prolonged periods of negative real returns. Rates usually co-move positively with inflation but do not always compensate the investor fully.

"If the return>real GDP growth, reducing the debt/GDP ratio requires continuous budget surpluses."

"If the return>real GDP growth, reducing the debt/GDP ratio requires continuous budget surpluses."

9/ "After WWI, significant budgetary efforts were required to repay war debts, especially given the reparations imposed by the Treaty of Versailles and a turbulent macroeconomic environment."

"After WW2, high growth and inflation helped reduce the value of the national debt."

"After WW2, high growth and inflation helped reduce the value of the national debt."

10/ "Housing returns have remained remarkably stable. The correlation between equity and housing returns was highly positive before WW2 but has all but disappeared.

"Housing provided a more robust inflation hedge.

"Equities have also become highly correlated across countries."

"Housing provided a more robust inflation hedge.

"Equities have also become highly correlated across countries."

11/ "For the countries in our sample, housing has Sharpe ratios that are, on average, double those of equities."

Again, serious caveats here: the national single-family home indices described here are unlikely to be investable, and they also do not include property taxes.

Again, serious caveats here: the national single-family home indices described here are unlikely to be investable, and they also do not include property taxes.

12/ "The higher volatility of equity prices is a persistent feature of all countries and periods in our sample.

"*National* *aggregate* housing portfolios have had comparable real returns to national aggregate equity portfolios but with only half the volatility." (emphases mine)

"*National* *aggregate* housing portfolios have had comparable real returns to national aggregate equity portfolios but with only half the volatility." (emphases mine)

13/ The authors estimate returns during market closures. Nominal returns are overestimates due to survivorship bias, while real capitalization changes are underestimates because they assume all delisted stocks went bankrupt.

The impact is small due to closures being infrequent.

The impact is small due to closures being infrequent.

14/ Rental yield = income net of property management costs, ground rent, other irrecoverable expenditures, and depreciation

This *excludes* the effect of property taxes, which the authors estimate to be less than 1% annually due to historical deductibility against income taxes.

This *excludes* the effect of property taxes, which the authors estimate to be less than 1% annually due to historical deductibility against income taxes.

15/ "The level of rent-to-price using two different estimation approaches is similar, both in the modern day and historically.

"Changing rental yield benchmarks has only a small impact on return, moving them up or down a little under 1 percentage point."

"Changing rental yield benchmarks has only a small impact on return, moving them up or down a little under 1 percentage point."

16/ To what extent would a bias toward city properties vs. non-city properties affect results?

Rent/price is the reciprocal of the gross rent multiplier, which itself may change by 3x rent based on location. This allows the authors to calculate upper/lower bounds for the return.

Rent/price is the reciprocal of the gross rent multiplier, which itself may change by 3x rent based on location. This allows the authors to calculate upper/lower bounds for the return.

17/ "REIT returns seem to be affected by the general ups and downs of the stock market.

"Overall, the returns on REITs confirm the general housing return results. The comparison also suggests that returns in housing markets tend to be smoother than those in stock markets."

"Overall, the returns on REITs confirm the general housing return results. The comparison also suggests that returns in housing markets tend to be smoother than those in stock markets."

18/ Round-trip transaction costs of 7.7% every 10 years = return drag of 77 bps/year

Housing prices are smoothed over 1 year, so the authors re-calculate data for the equity index by smoothing that for a year as well. Volatility drops by one-fifth with a smaller drop in returns.

Housing prices are smoothed over 1 year, so the authors re-calculate data for the equity index by smoothing that for a year as well. Volatility drops by one-fifth with a smaller drop in returns.

19/ "In the U.S., local (ZIP5) housing volatility is about twice as large as aggregate volatility, which would about equalize risk-adjusted returns to equity and housing if investors owned one undiversified house. And it is difficult to invest in a diversified housing portfolio."

20/ "Safe assets have not generally provided a hedge against risk, since safe returns were low when risky returns were low - in particular, during world wars. This positive correlation has weakened over more recent decades and turned negative from the 1990s onward."

21/ "Interestingly, the period of high risk premiums coincided with a remarkably low frequency of systemic banking crises.

"This finding speaks to the recent literature on the mispricing of risk around financial crises."

For example:

"This finding speaks to the recent literature on the mispricing of risk around financial crises."

For example:

22/ "The remarkable rise in cross-country correlations in risk premiums may pose new challenges to the risk-bearing capacity of the global financial system, a trend consistent with other macro indicators of risk-sharing."

23/ "In theory, a higher spread between the real return on wealth (r) and real GDP growth (g) tends to magnify the steady-state level of wealth inequality.

"In peactime, r has always exceeded g with a persistently large gap. R>g in every country and time period we consider."

"In peactime, r has always exceeded g with a persistently large gap. R>g in every country and time period we consider."