Trend, value, quality, carry, volatility. Tentmaker (eating vol-targeted Sortino to fund Christian work). See the pinned tweet for compound return generators.

2/ "Ecclesiastes tells the story of someone who saw it all, got it all, experienced it all, and in the end found fault with it all - yet the author of Ecclesiastes still didn’t find what he was looking for. Having it all won’t make you happy." (p. xi)

2/ "Ecclesiastes tells the story of someone who saw it all, got it all, experienced it all, and in the end found fault with it all - yet the author of Ecclesiastes still didn’t find what he was looking for. Having it all won’t make you happy." (p. xi) 2/ "A small group of undervalued professional players & executives, many of whom had been rejected as unfit for the big leagues, turned themselves into one of the most successful franchises.

2/ "A small group of undervalued professional players & executives, many of whom had been rejected as unfit for the big leagues, turned themselves into one of the most successful franchises. 2/ Asset classes have fat tails, and most have negative skewness.

2/ Asset classes have fat tails, and most have negative skewness.

2/ #1. Fiction: Factors are Data-Mined with No Good Economic Story

2/ #1. Fiction: Factors are Data-Mined with No Good Economic Story

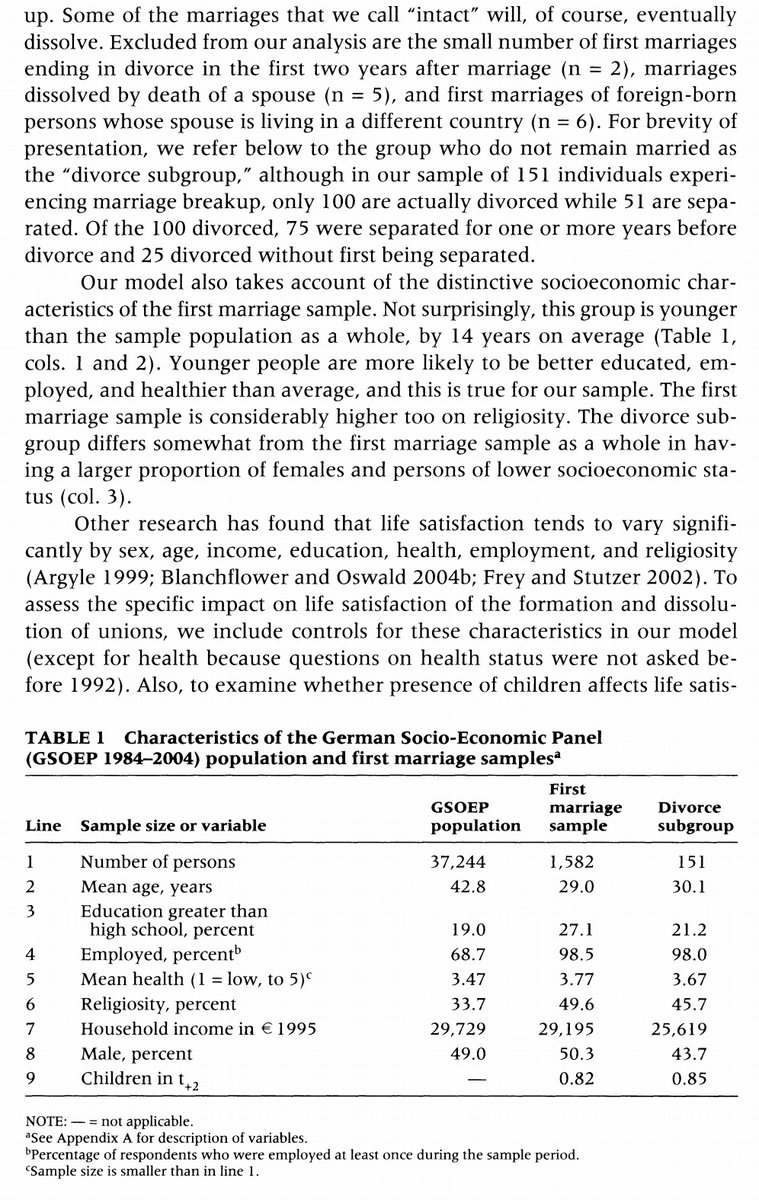

2/ "The model's four terms describe different life stages for an individual who marries during the sample period. The intercept reflects the average life satisfaction of individuals in the baseline period [all noncohabiting years that are at least one year before marriage]."

2/ "The model's four terms describe different life stages for an individual who marries during the sample period. The intercept reflects the average life satisfaction of individuals in the baseline period [all noncohabiting years that are at least one year before marriage]."

2/ "The valuation gap between cheap and expensive stocks remains extremely wide. This signals the potential for attractive returns going forward."

2/ "The valuation gap between cheap and expensive stocks remains extremely wide. This signals the potential for attractive returns going forward."

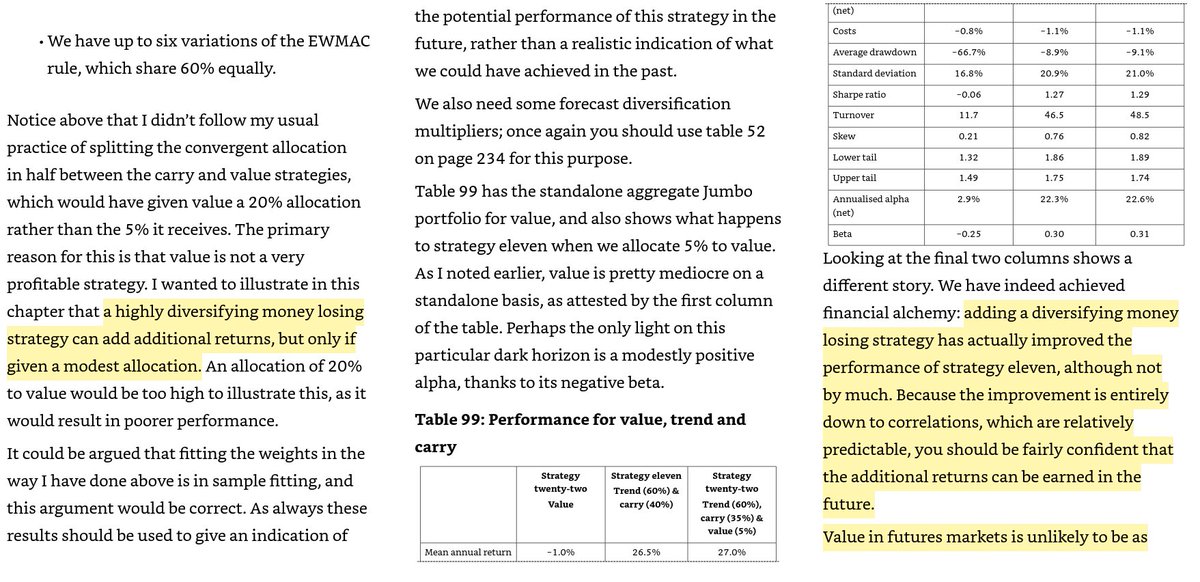

2/ Part 1: Basic directional strategies

2/ Part 1: Basic directional strategies

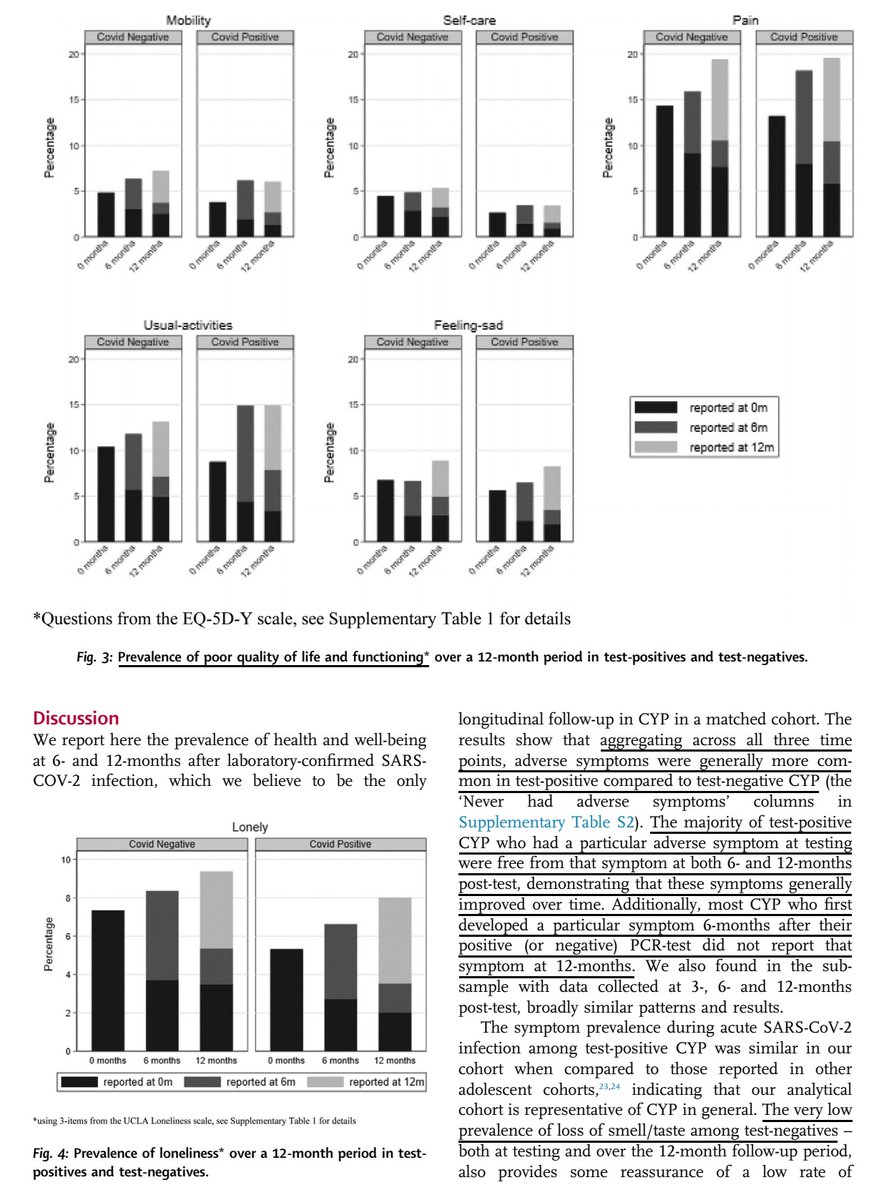

2/ "The broadly similar pattern of adverse health and well-being reported as new-onset at 6- and 12 months among test-positives and test-negatives highlights the non-specific nature of these symptoms and suggests that multiple aetiologies may be responsible."

2/ "The broadly similar pattern of adverse health and well-being reported as new-onset at 6- and 12 months among test-positives and test-negatives highlights the non-specific nature of these symptoms and suggests that multiple aetiologies may be responsible."

2/ Do you hedge out market beta in order to make the portfolio more risk balanced?

2/ Do you hedge out market beta in order to make the portfolio more risk balanced?

2/ "Study 1 shows that less hedonic adaptation is reported in response to activity changes than to circumstantial changes."

2/ "Study 1 shows that less hedonic adaptation is reported in response to activity changes than to circumstantial changes."

2/ "After controlling for age, gender, and population size, greater neighborhood socioeconomic status (SES) predicted greater desires for material consumption, more impulsive buying, and fewer savings behaviors, while individual SES showed the reverse pattern."

2/ "After controlling for age, gender, and population size, greater neighborhood socioeconomic status (SES) predicted greater desires for material consumption, more impulsive buying, and fewer savings behaviors, while individual SES showed the reverse pattern."

2/ " This phenomenon is robust to including out-of-the-money options or delta-hedging the returns.

2/ " This phenomenon is robust to including out-of-the-money options or delta-hedging the returns.

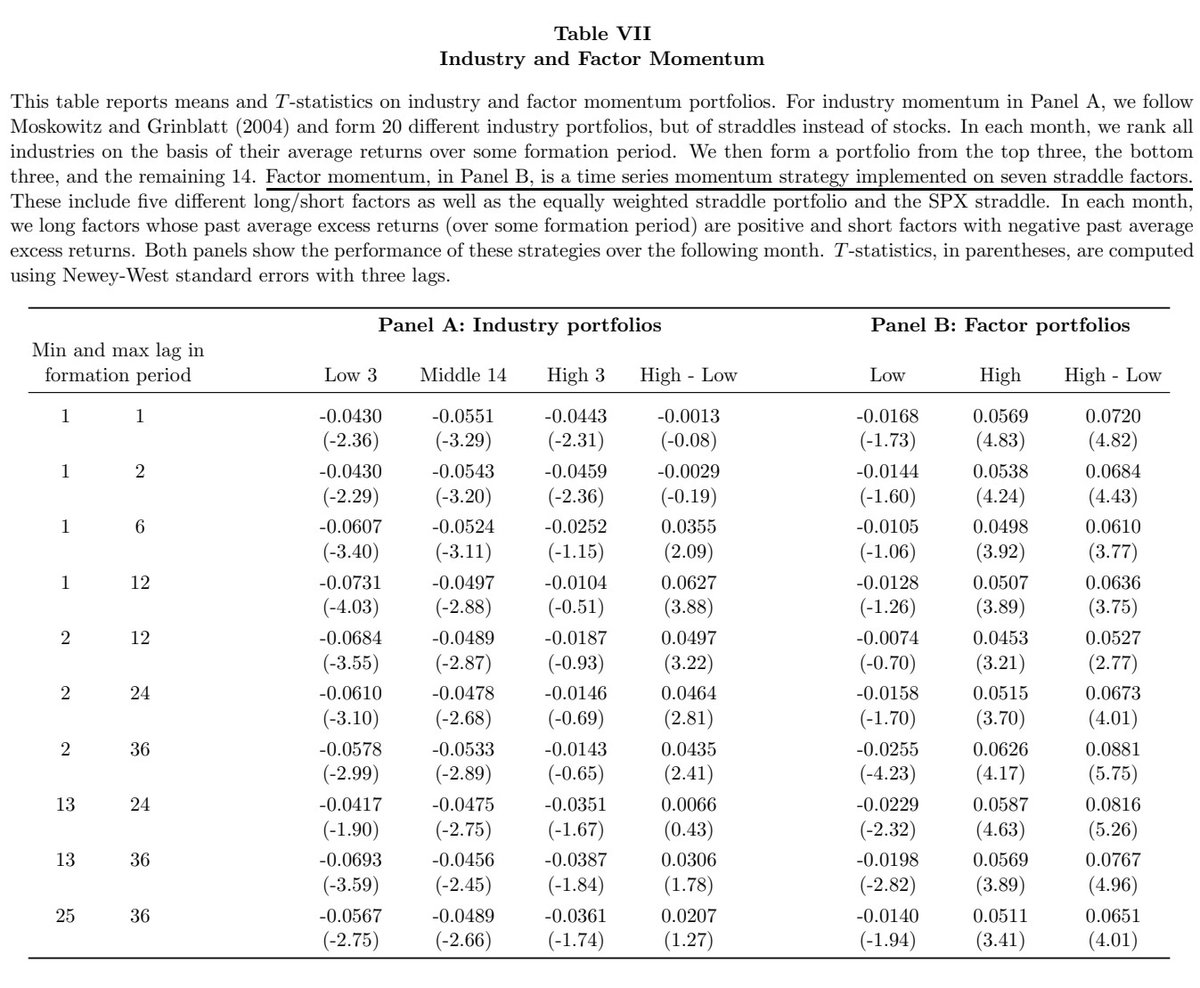

2/ "This result is robust to the length of the formation period and is apparent in a wide variety of subsamples.

2/ "This result is robust to the length of the formation period and is apparent in a wide variety of subsamples.