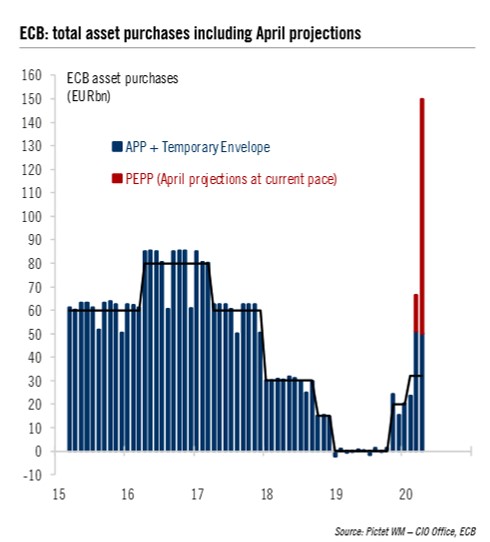

Some early indicators suggest that the ECB should at least double the size of its Pandemic Emergency Purchase Programme (PEPP), and that is before we get any clarity in terms of the longer term effects of the crisis on economic growth and inflation. (2/n)

We are well aware that the German Court ruling was against PSPP, not PEPP, but the point is still relevant in forward-looking terms including if new complaints against PEPP are brought to the court. (3/n)

We are also aware of the difficulty of estimating the required size of asset purchases, even in ‘normal’ times. Here's a piece we wrote last year in the topic: How much ECB QE is needed? Go big, or go home! (4/n) perspectives.group.pictet/sites/perspect…

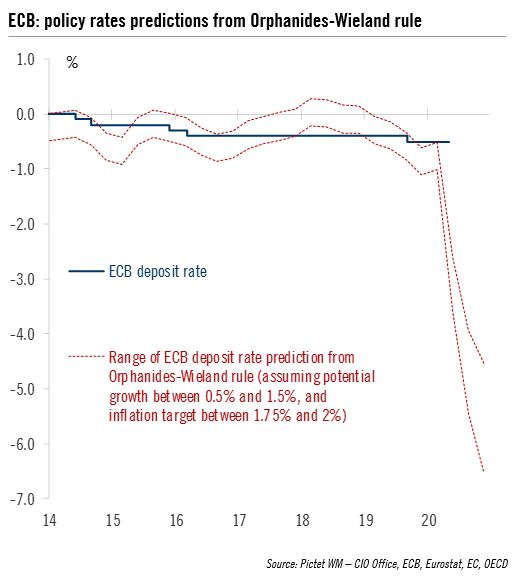

One approach is based on the Orphanides-Wieland (OW) Taylor rule, which is interesting since @WielandVolker was one of the economists heard by the @BVerfG in July 2019 ahead of its ruling. (5/n)

Using the latest SPF, and assuming euro area potential growth between 0.5% and 1.5%, the OW rule suggests that the ECB deposit rate should be lowered by 150bp to 250bp over the next quarter, and by 350bp to 550bp by year-end (not a typo). (6/n)

Using past elasticities, the OW rule would suggest that ECB asset purchases need to be increased by a factor 3 to 5! In practice, the lagged effects of QE must be taken into account as well as other credit easing measures, including TLTROs. (7/n)

Either way, the OW rule would require a significant amount of addition ECB stimulus by June, for the monetary stance to remain “proportionate” to the economic conditions. @WielandVolker (8/n)

Note that APP, not PEPP, should be the most appropriate tool to address the inflation outlook. But this makes the decision more complicated after the German Constitutional Court’s ruling on PSPP. (9/n)

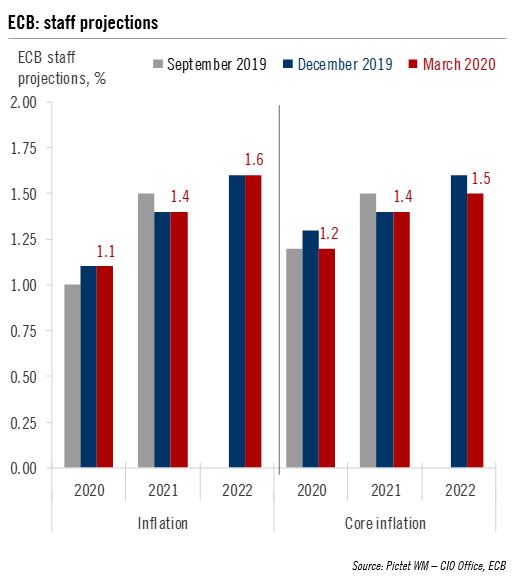

Another simple rule of thumb relates the amount of asset purchases required to close the “inflation gap” (the distance from staff projections to the inflation target). The so-called Draghi rule says that a 0.5% inflation gap requires up to €700bn in asset purchases. (10/n)

Assuming that 2022 headline inflation is lowered to 1.5% in the June staff projections *despite* recent ECB measures, the Draghi rule would be consistent with an increase in the PEPP to close to €1.5tn, along a possible extension to September 2021. (11/n)

At best, a compromise solution could be found with the ECB increasing PEPP by, say, €500bn, to €1.25tn.

At worst, it could force the ECB to delay a decision with the risk that higher financial volatility and fragmentation forces them to do more eventually. (/End)

At worst, it could force the ECB to delay a decision with the risk that higher financial volatility and fragmentation forces them to do more eventually. (/End)