Head of Strategy & Macro Research, Pictet Wealth Management @PictetGroup.

ECB Watcher. All opinions mine.

M3 annual growth continues to be dragged lower by the narrow money aggregate M1 which contracted by a record amount in nominal and real terms.

M3 annual growth continues to be dragged lower by the narrow money aggregate M1 which contracted by a record amount in nominal and real terms.

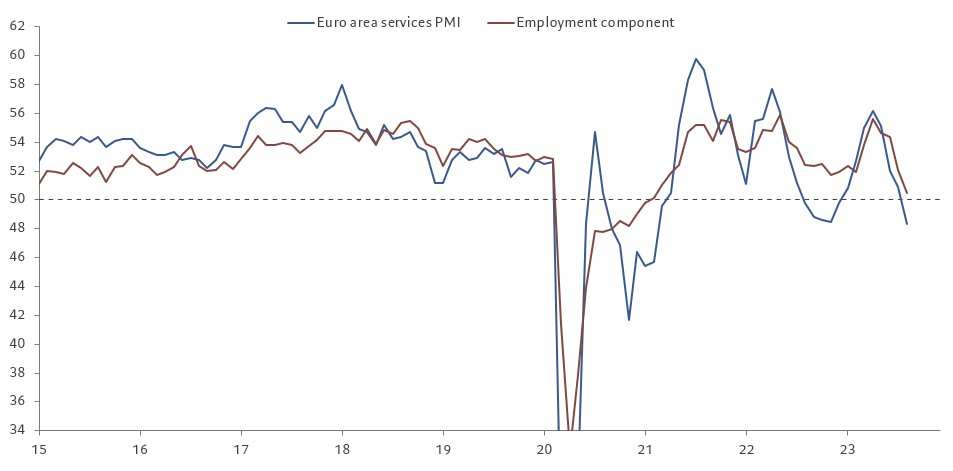

2. Early signs of stabilisation in the manufacturing sector, but external demand remains subdued.

2. Early signs of stabilisation in the manufacturing sector, but external demand remains subdued.

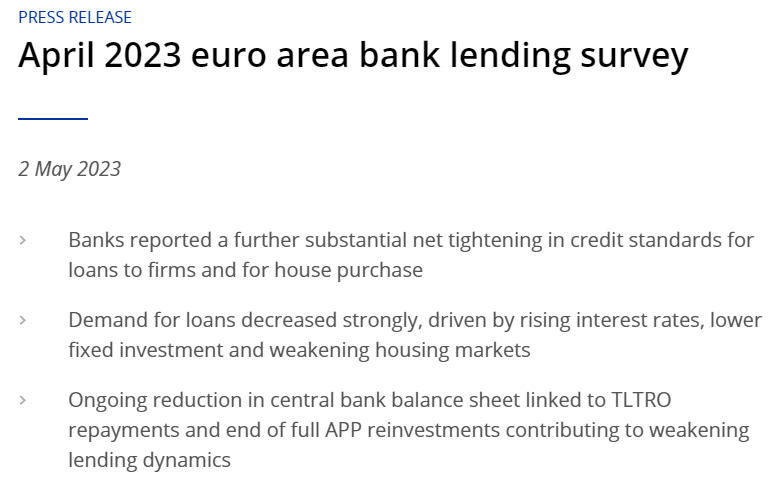

The ECB's Bank Lending Survey was conducted between 22 March and 6 April, taking into account recent events.

The ECB's Bank Lending Survey was conducted between 22 March and 6 April, taking into account recent events.

In real terms, M1 growth is now down 10% YoY, consistent with a collapse in economic growth. 😱

In real terms, M1 growth is now down 10% YoY, consistent with a collapse in economic growth. 😱

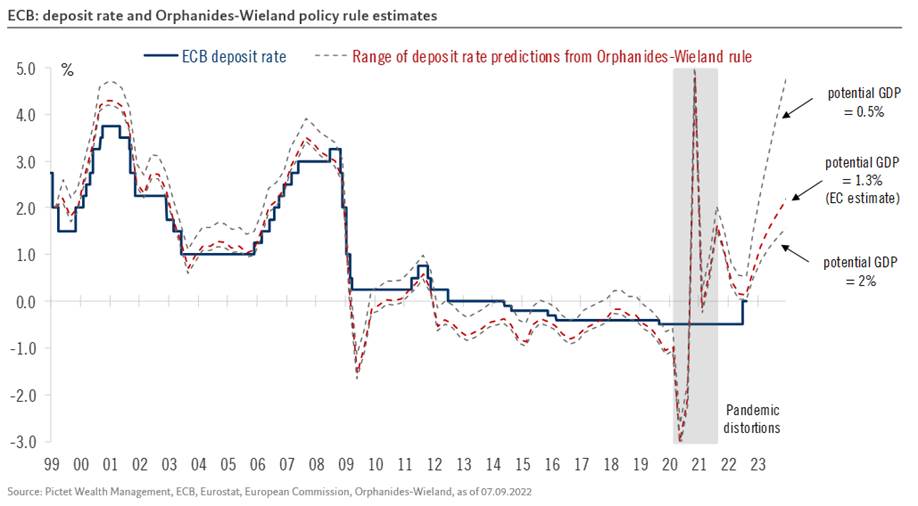

The hawkish reality check came in December, when the ECB committed to raising rates "significantly at a steady pace to reach levels that are sufficiently restrictive". The sentence should be adjusted as the ECB gets closer to peak rates.

The hawkish reality check came in December, when the ECB committed to raising rates "significantly at a steady pace to reach levels that are sufficiently restrictive". The sentence should be adjusted as the ECB gets closer to peak rates.

Here's the @NBB_BNB_FR press release confirming the profit warning issued in September.

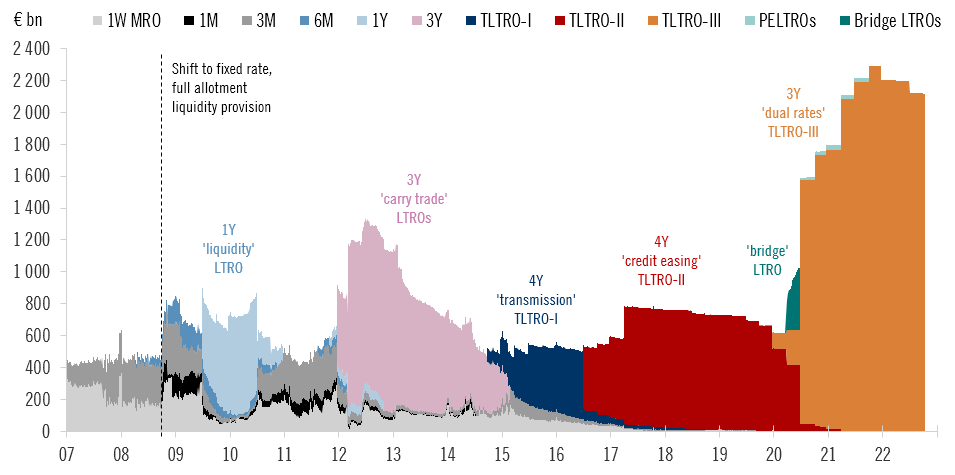

Here's the @NBB_BNB_FR press release confirming the profit warning issued in September. We once dubbed TLTROs The Last Tools Really Operational. TLTROs have played a crucial role in the transmission of monetary policy to the real economy, including during the pandemic, providing stable medium-term funding to banks under the conditions to maintain lending to SMEs.

We once dubbed TLTROs The Last Tools Really Operational. TLTROs have played a crucial role in the transmission of monetary policy to the real economy, including during the pandemic, providing stable medium-term funding to banks under the conditions to maintain lending to SMEs.

The SNB's record losses make it highly unlikely that the central bank will redistribute anything to the federal government and cantons.

The SNB's record losses make it highly unlikely that the central bank will redistribute anything to the federal government and cantons.

Euro area core HICP inflation rose to 4.79% in September as underlying price pressures kept broadening. Core goods inflation was up 50bp to 5.6%, but is likely to ease soon. Services inflation up by 50bp to 4.3%, which is more of a concern.

Euro area core HICP inflation rose to 4.79% in September as underlying price pressures kept broadening. Core goods inflation was up 50bp to 5.6%, but is likely to ease soon. Services inflation up by 50bp to 4.3%, which is more of a concern.

ECB: "This major step frontloads the transition from the prevailing highly accommodative level of policy rates towards levels that will ensure the timely return of inflation to the ECB’s 2% medium-term target."

ECB: "This major step frontloads the transition from the prevailing highly accommodative level of policy rates towards levels that will ensure the timely return of inflation to the ECB’s 2% medium-term target."

We expect the ECB to hike rates by 75bp. It’s all about preserving credibility at all cost, because a failure to act would lead to more pain in the future, as per @Isabel_Schnabel's Jackson Hole speech.

We expect the ECB to hike rates by 75bp. It’s all about preserving credibility at all cost, because a failure to act would lead to more pain in the future, as per @Isabel_Schnabel's Jackson Hole speech.