Air Partner #AIR.L may be re-rating rather than bouncing.

They're an aircraft charterer in a rather profitable spot: current air travel restrictions mean they're currently over-earning at quite a rate (understatement) and should continue to benefit even as the industry returns.

They're an aircraft charterer in a rather profitable spot: current air travel restrictions mean they're currently over-earning at quite a rate (understatement) and should continue to benefit even as the industry returns.

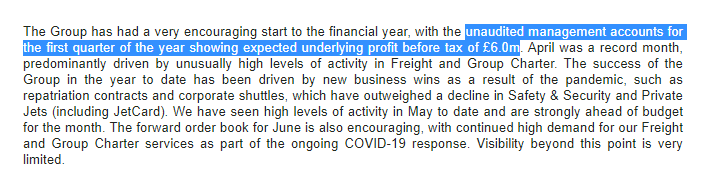

You'd probably never know otherwise unless you found a line buried on page 10 of 56 in their last report or follow @EricUKinvestor's posts flagging up the company: by their measure of underlying profitability, their first quarter was bigger than any full year previously.

It's a simple thesis - the freight division benefits from Covid emergency response needs and the pinch in airline freight capacity as airlines are grounded. As the crisis abates, airlines will only gradually reintroduce routes and frequencies meaning this should decline slowly.

Their private jet chartering arm may pick up the slack at this point; social distancing is an inherent attraction to the business and projections for a 3-year return to normality for airlines mean route choice / frequency remain limited, driving increased demand for this service.

Their May private jet flight interest is already up 210% according to this link posted by Eric. Whilst it's not a company without issues, I think there's a chance the current and coming environment should allow them to re-rate to a higher level.

privatejetcardcomparisons.com/2020/05/27/may…

privatejetcardcomparisons.com/2020/05/27/may…

Air Partner #AIR

June 4 "At the end of May, the Group has normalised cash in the bank of £16.5m" = £11.9M in Q1

Cashflow timing issues aplenty no doubt but impressive nonetheless compared to previous FYs' net change in cash:

-£3M (20), +£1.5M (19), +£3.9M (18), -£1.6M (17)

June 4 "At the end of May, the Group has normalised cash in the bank of £16.5m" = £11.9M in Q1

Cashflow timing issues aplenty no doubt but impressive nonetheless compared to previous FYs' net change in cash:

-£3M (20), +£1.5M (19), +£3.9M (18), -£1.6M (17)

Airports like Zadar and Split in Croatia have been packed with private jets even before the UK travel corridor restrictions

uk.finance.yahoo.com/news/how-to-ch…

uk.finance.yahoo.com/news/how-to-ch…

• • •

Missing some Tweet in this thread? You can try to

force a refresh