🔥 #PetroleumSectorInZimbabwe #PetroleumBusinessInZimbabwe #FuelBusinessInZimbabwe

1/ There has been acute fuel shortages in ZW for period up to 2008 & from 2016 to date.

What are the public policies in operation that have either caused the shortages or have not ended them?

1/ There has been acute fuel shortages in ZW for period up to 2008 & from 2016 to date.

What are the public policies in operation that have either caused the shortages or have not ended them?

2/ What you will find in this thread is either meant to be informative or provoke discussions.

Its a citizen contribution to the conversations on a matter of public interest: FUEL SHORTAGE.

Its a citizen contribution to the conversations on a matter of public interest: FUEL SHORTAGE.

3/ #Petroleum - rock oil, oily inflammable substance occurring naturally in certain rock beds." This is from Medieval Latin petroleum, from Latin petra ("rock") + oleum ("oil").

"Petroleum" word was first used in 1556 by the German mineralogist Georg Bauer (Georgius Agricola).

"Petroleum" word was first used in 1556 by the German mineralogist Georg Bauer (Georgius Agricola).

4/ "Petroleum & petroleum related substances were already known by the ancient civilizations of the Fertile Crescent & Egypt.

eolss.net/Sample-Chapter…

eolss.net/Sample-Chapter…

5/ Petroleum was known later to the Persians, Greeks& Romans under the name of naphtha; the less-liquid varieties were called [asphaltos] by the Greeks, and bitumen was with the Romans a generic name for all the naturally occurring hydrocarbons.

6/ Petroleum, complex mixture of hydrocarbons that occur in Earth in liquid, gaseous or solid form. The term is often restricted to the liquid form, commonly called crude oil, but, as a technical term, petroleum also includes natural gas & the solid form known as bitumen.

7/ The liquid and gaseous phases of petroleum constitute the most important of the primary fossil fuels.

8/ Liquid & gaseous hydrocarbons are customarily shortened as “petroleum&natural gas” to “petroleum” when referring to both.

9/ Petroleum products consist of:

1. Diesel,

2. Petrol (Gasoline),

3. Liquefied Petroleum Gas (LPG),

4. Paraffin,

5. Jet Fuel,

6. Aviation Fuel,

7. Bio-fuel

1. Diesel,

2. Petrol (Gasoline),

3. Liquefied Petroleum Gas (LPG),

4. Paraffin,

5. Jet Fuel,

6. Aviation Fuel,

7. Bio-fuel

10/ The #PetroleumIndustry has the following business activities:

i. petroleum engineering: exploration by petroleum geologists, extraction by drilling & reservoir engineers, refining by petroleum production engineers,

ii. transporting,&

iii. marketing of petroleum products.

i. petroleum engineering: exploration by petroleum geologists, extraction by drilling & reservoir engineers, refining by petroleum production engineers,

ii. transporting,&

iii. marketing of petroleum products.

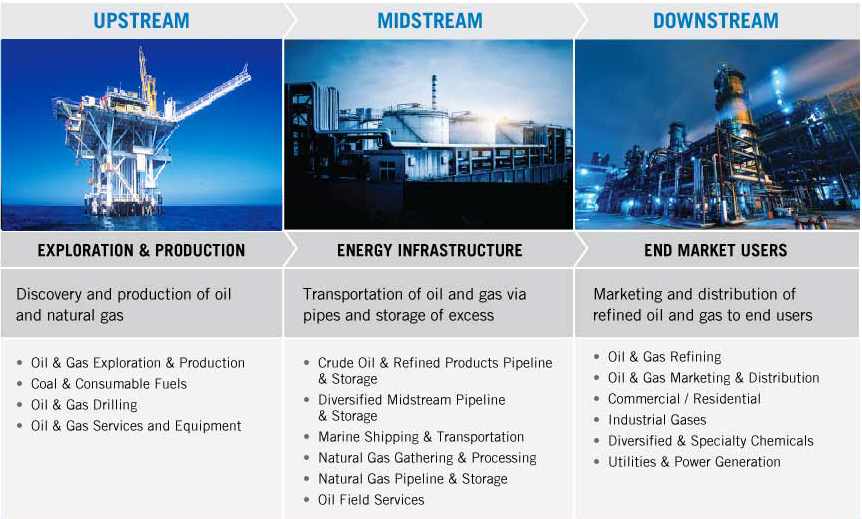

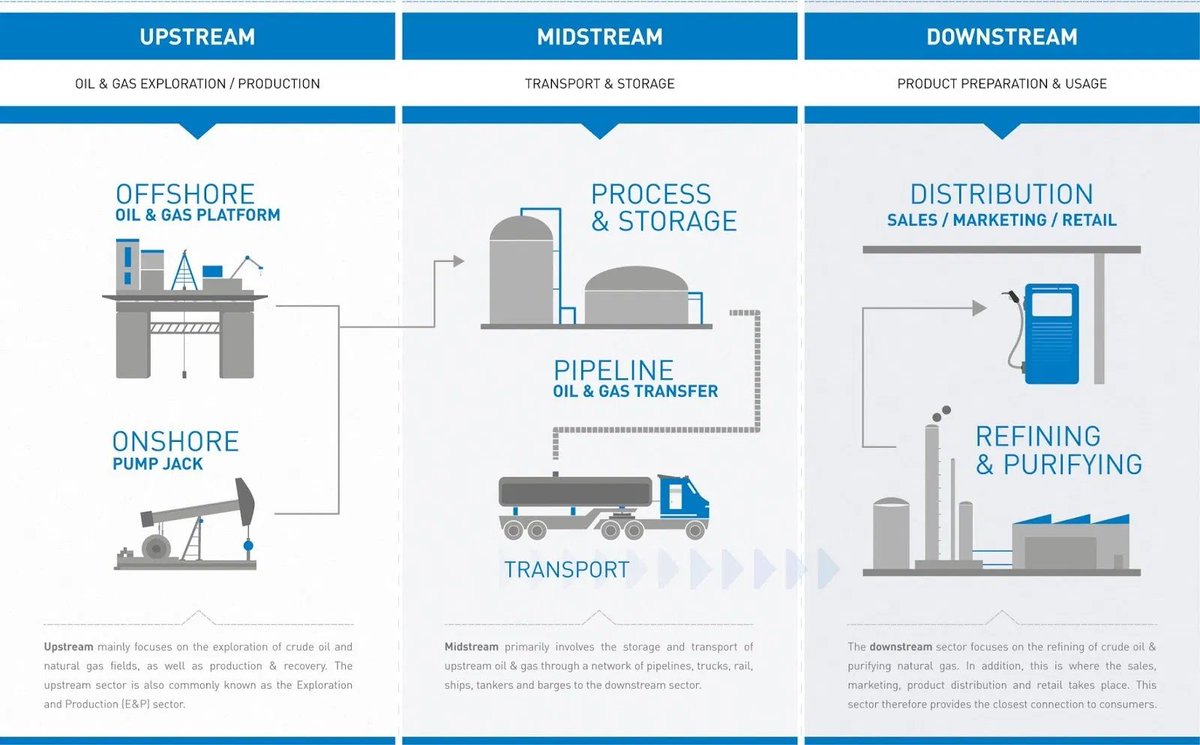

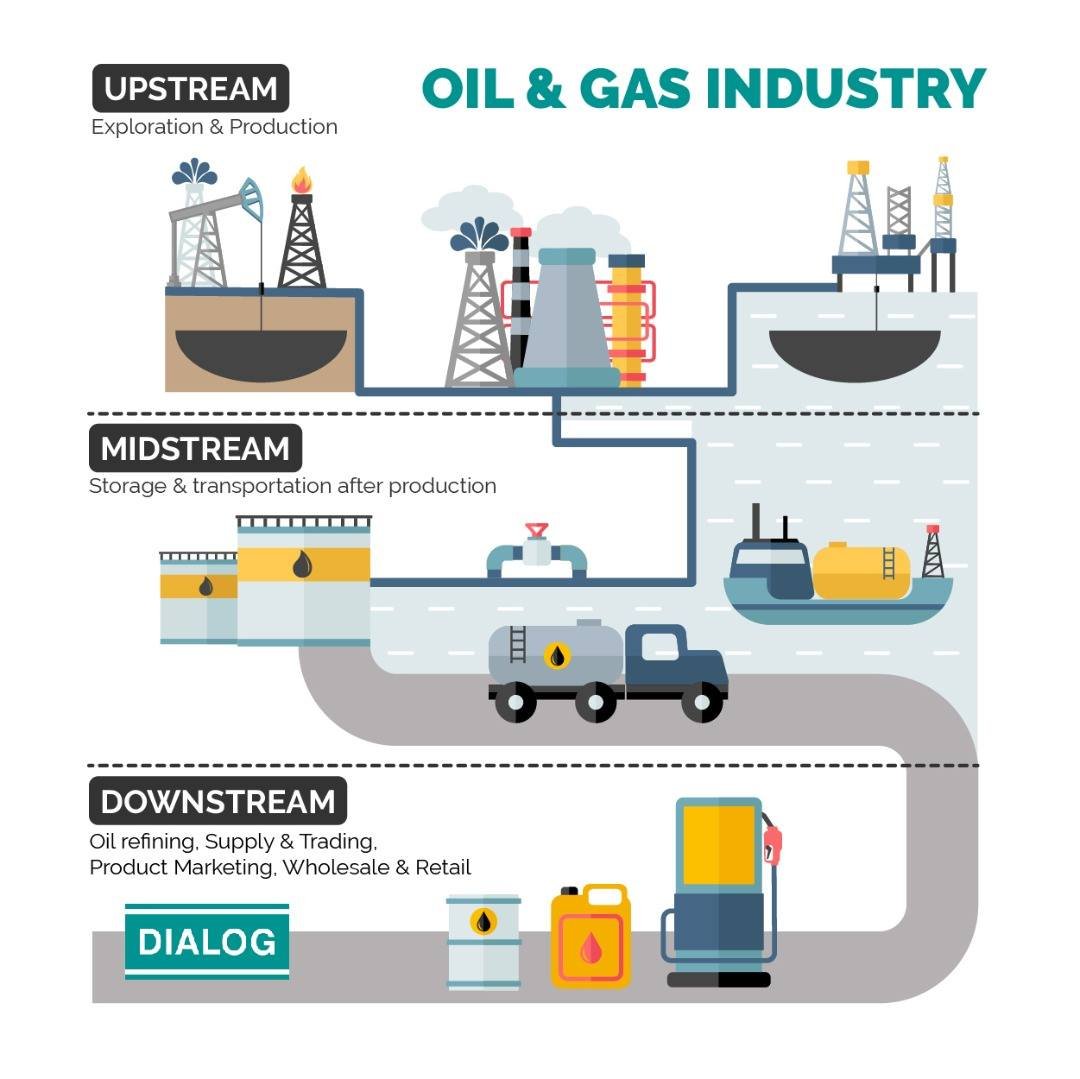

11/ There are three process segments of the #PetroleumIndustry:

i. #Upstream,

ii. #Midstream &

iii. #Downstream

i. #Upstream,

ii. #Midstream &

iii. #Downstream

11/ ii) #Midstream: this pertains to the transportation of crude oil&natural gas after production, i.e the infrastructure including pipelines &tank trucks to transport&store crude oil&natural gas

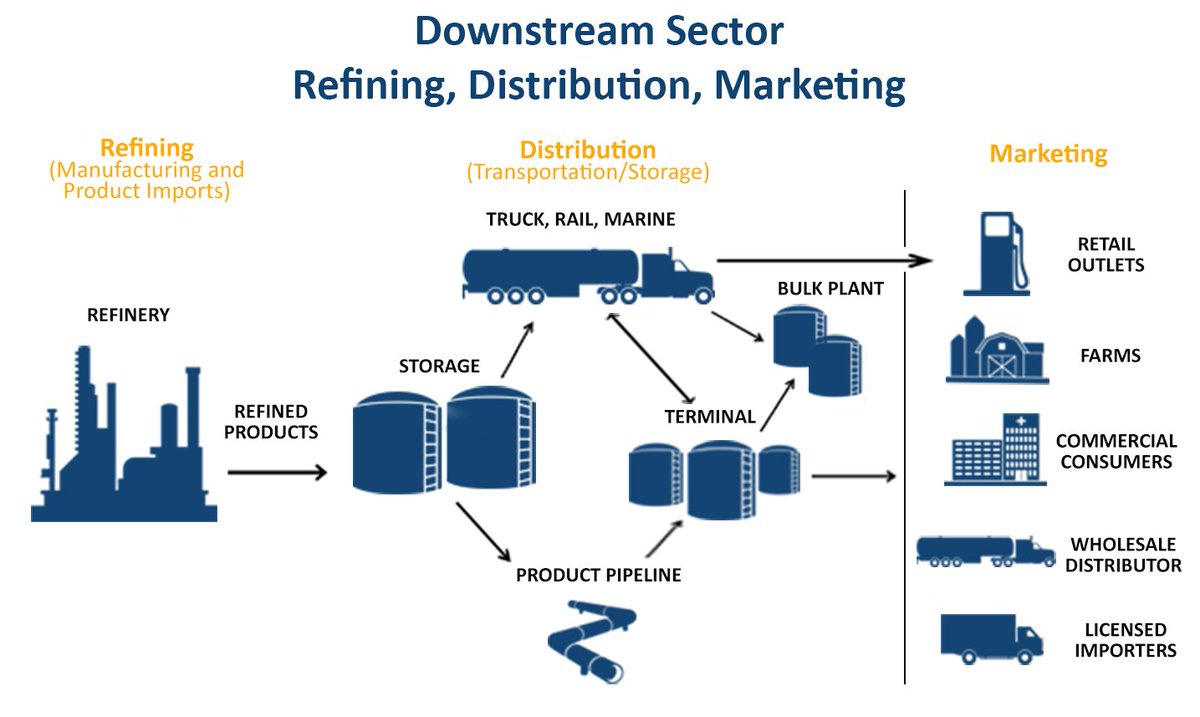

11/ iii) #Downstream: this involves turning crude oil&natural gas into various useful final products. Even detergent, plastic&candles are also made with petroleum products.

12/ Ordinarily, the downstream businesses (marketing channel) consists of a:

i) /Importer,

ii) Petroleum Marketing Company (Procurer&Wholesaler) &

iii) Retailer.

For one to do business in any of these, one needs to be licensed by the regulatory authority, ZERA.

i) /Importer,

ii) Petroleum Marketing Company (Procurer&Wholesaler) &

iii) Retailer.

For one to do business in any of these, one needs to be licensed by the regulatory authority, ZERA.

12/ i) Petroleum Manufacturer/Producer - this one refines or manufactures petroleum products & sells them to an exporter who in the case of Zimbabwe is the importer.

12/ ii) In ZW, the petroleum importers deal with a #PetroleumMarketingCompany (#PMC), which holds two licenses:

a) for procurement to buy from importers, &

b) for wholesaling to sell to retailers (own or franchisee service stations).

a) for procurement to buy from importers, &

b) for wholesaling to sell to retailers (own or franchisee service stations).

12/ iii) Petroleum Retailer - this one purchases products from a licensed wholesaler only to sell products to members of the public thru own or franchisee service stations.

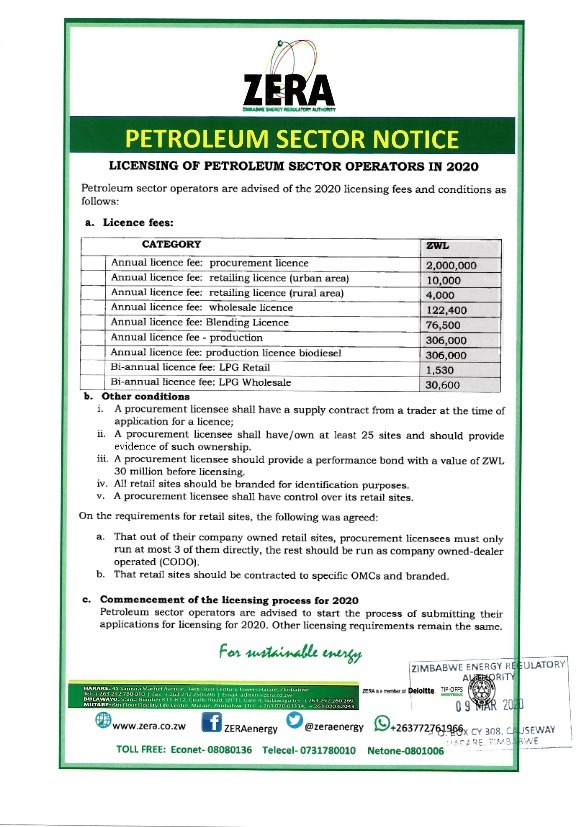

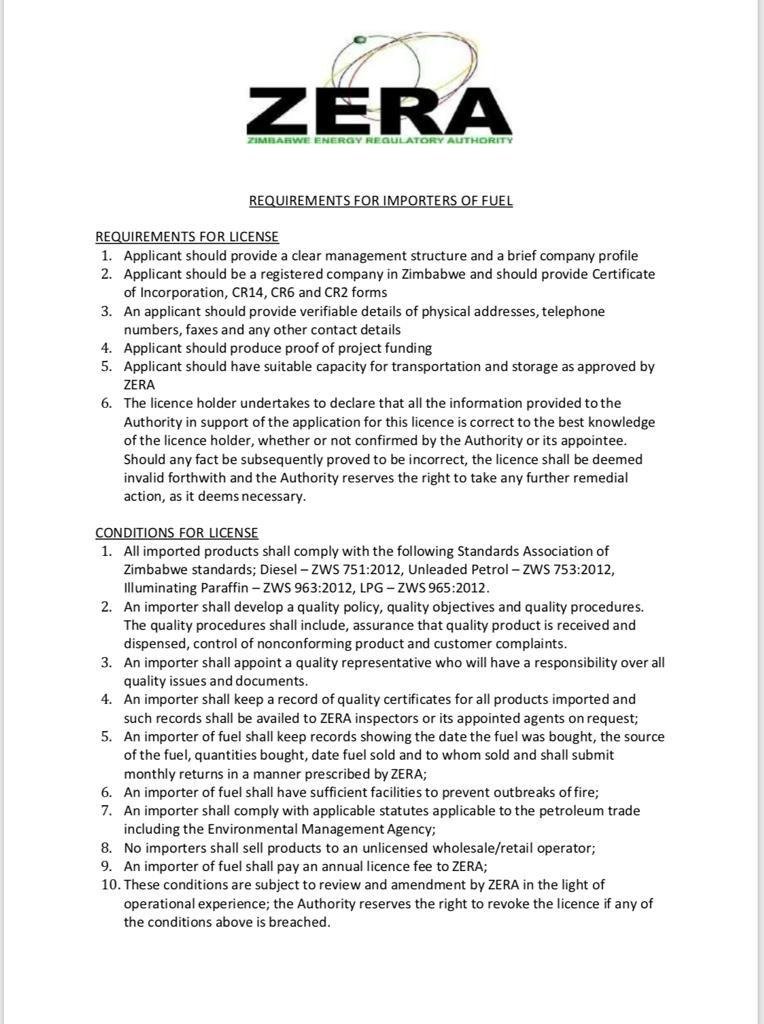

13/ Under s32 of the Energy Regulatory Act, “license” is for procurement, wholesaling, retailing or production.

There are 5 categories of petroleum licensees:

i. Production

ii. Blending

iii. Wholesale

iv. Procurement

v. Retailing (Urban&Rural)

zera.co.zw/electricity3/

There are 5 categories of petroleum licensees:

i. Production

ii. Blending

iii. Wholesale

iv. Procurement

v. Retailing (Urban&Rural)

zera.co.zw/electricity3/

14/

i. The value chain is as follows:

a. Producer >>

b. Importer (international petroleum companies) >>

c. Wholesaler (#PetroleumMarketingCompanies) >>

d. Retailer (own or franchisee service stations))

All the PMCs have their own & franchised retail outlets.

i. The value chain is as follows:

a. Producer >>

b. Importer (international petroleum companies) >>

c. Wholesaler (#PetroleumMarketingCompanies) >>

d. Retailer (own or franchisee service stations))

All the PMCs have their own & franchised retail outlets.

14/ ii. PMCs buy from petroleum importers generally at a minimum deal size of 500,000 litres.

iii. #Wholesalers or importers buy the products directly from #PetroleumProducers.

iii. #Wholesalers or importers buy the products directly from #PetroleumProducers.

14/ iv. Even if local small companies that wish to be licensed for procurement, the volume required by the importers would require a bigger consortium of them to bring resources together.

15/ These are the licensees per area of business for the period 2012-2019.

16/ ZW's importers supplies #PMCs (Procurers/Wholesalers)

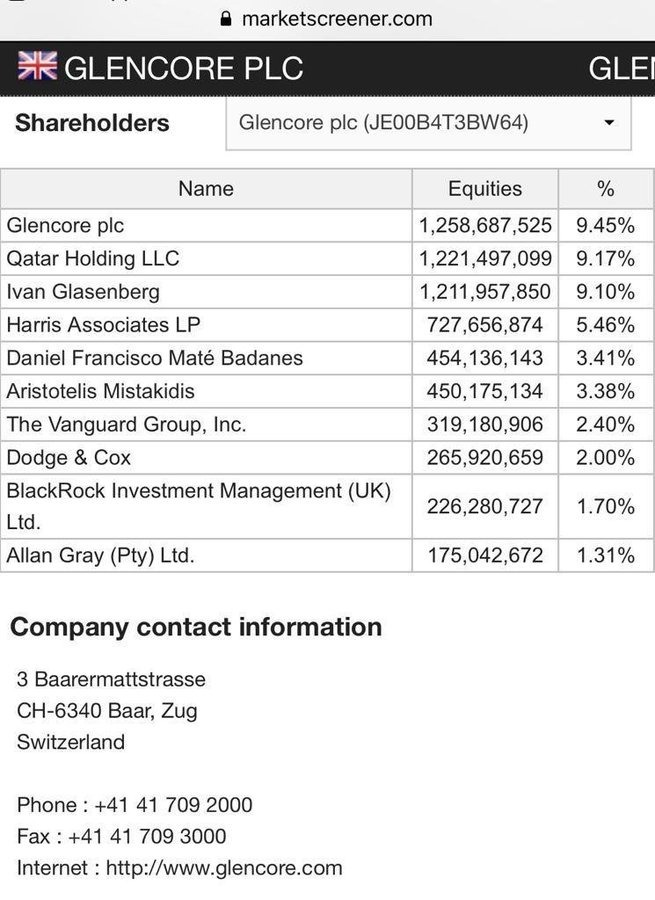

i. Glencore plc - Zuva

ii. Puma Energy - Trek/Puma/Genesis/Petrotrade/Ram

iii. Total -Total

iv. Vivon Energy - Engen

v. Unknown importer for various small players under Indigenous Petroleum Association of Zimbabwe (IPAZ)

i. Glencore plc - Zuva

ii. Puma Energy - Trek/Puma/Genesis/Petrotrade/Ram

iii. Total -Total

iv. Vivon Energy - Engen

v. Unknown importer for various small players under Indigenous Petroleum Association of Zimbabwe (IPAZ)

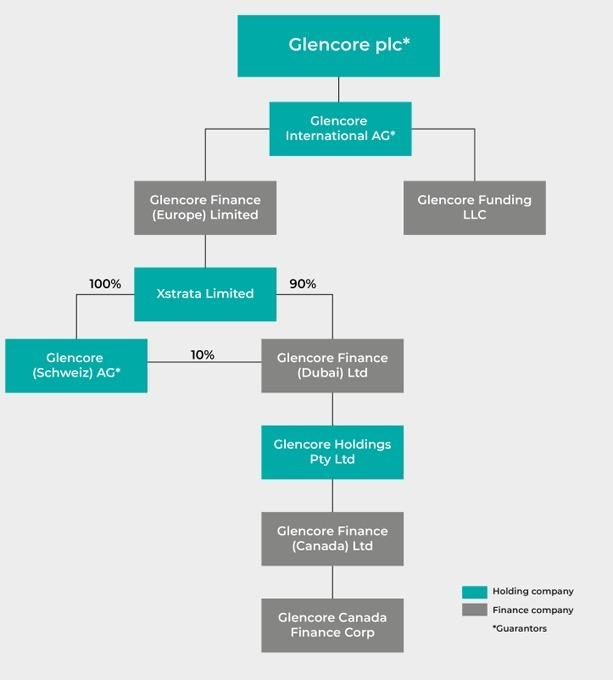

16/ i. Glencore plc, which supplies fuel to a licensed PMC, Zuva Energy, is a British multinational commodity trading & mining company with headquarters in Switzerland & its registered office in Jersey.

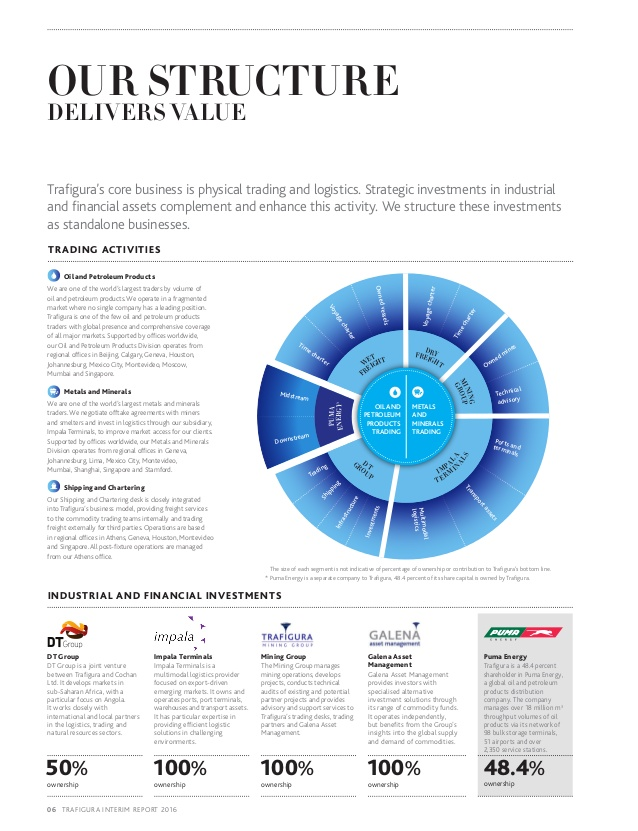

16/ ii. Puma Energy imports & supplies fuel to Trek/ Puma/ Genesis/ Ram/ Petrotrade.

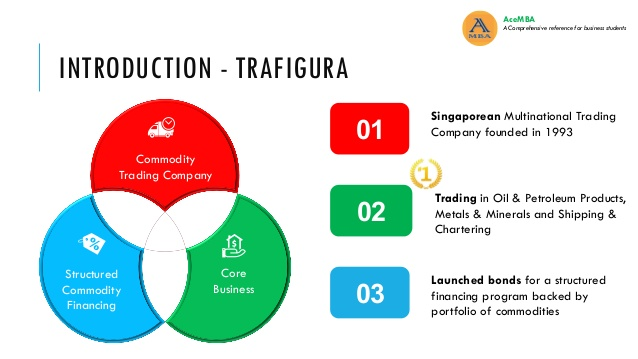

Its a Singaporean multinational oil company which is majority-owned by Trafigura and the Angolan Sonangol Group.

Its a Singaporean multinational oil company which is majority-owned by Trafigura and the Angolan Sonangol Group.

16 contd/ Puma Energy shareholding structure:

a. Trafigura: 49%,

b. Sonangol Holdings, a subsidiary of Angola's state-owned oil company: 28%,

c. Cochan Holdings LLC: less than 5%,

d. Private shareholders: remaining minority shares.

a. Trafigura: 49%,

b. Sonangol Holdings, a subsidiary of Angola's state-owned oil company: 28%,

c. Cochan Holdings LLC: less than 5%,

d. Private shareholders: remaining minority shares.

16 contd/ Trafigura Group is legally registered in Singapore and headquartered in Singapore. It is the world's second largest private oil trader after Vitol.

16 contd/ Cochan Holdings LLC is an investment group founded & controlled by an Angolan former army general & businessman Leopoldino Fragoso do Nasciment.

ft.com/content/9ebb30…

africa-confidential.com/article/id/123…

ft.com/content/9ebb30…

africa-confidential.com/article/id/123…

16 contd/ On March 2, 2020, Puma Energy announced the reduction of Cochan's from 15.5% to less than 5%.

pumaenergy.com/press-releases…

pumaenergy.com/press-releases…

16 contd/ iii. Total S.A imports & supplies to Total Zimbabwe retailers.

This is a French multinational integrated oil&gas company. It is one of the seven "Big Oil" companies in the world.

This is a French multinational integrated oil&gas company. It is one of the seven "Big Oil" companies in the world.

16/ iv. Vivon Energy supplies fuel to Engen Energy.

Vivon is a Shell licensee in Africa & its jointly owned by Dutch firm Vitol Africa BV & British-based private equity fund Helios Investment Partners. Shell was an initial shareholder at its formation.

shell.com/media/news-and…

Vivon is a Shell licensee in Africa & its jointly owned by Dutch firm Vitol Africa BV & British-based private equity fund Helios Investment Partners. Shell was an initial shareholder at its formation.

shell.com/media/news-and…

16/ v. Indigenous Petroleum Association of Zimbabwe (IPAZ) is alleged to have been formed in 2004 as a breakaway from multinationals (BP, Shell, Mobil, Caltex, Total & Engen) who dominated the Petroleum Marketers of Zimbabwe (PMZ).

17/ Zuva Petroleum, Trek, Petrotrade, Glow Petroleum, Ram Petroleum, Genesis Energy, Engen Energy, etc are all indigenous.

Who constitutes the Indigenous Petroleum Association of Zimbabwe (IPAZ)?

Are they PMCs or retailers?

Who is the importer of their fuel?

Who constitutes the Indigenous Petroleum Association of Zimbabwe (IPAZ)?

Are they PMCs or retailers?

Who is the importer of their fuel?

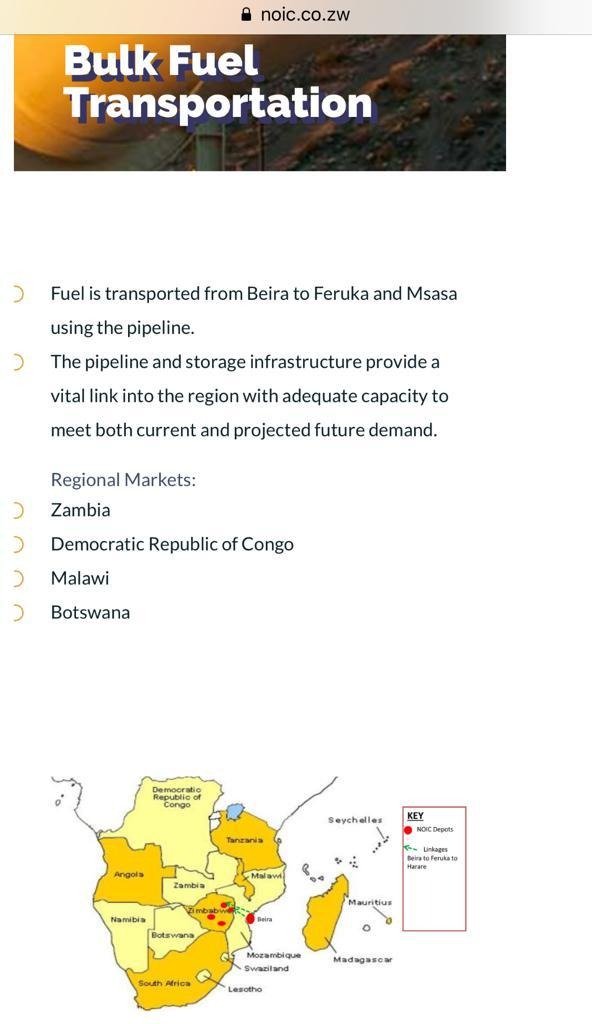

18/ All the petroleum products marketed in ZW are imported thru the Beira-Feruka-Msasa pipeline.

19/ The pipeline transports 90% of fuel into Zimbabwe while the balance of the fuel is imported by road pipeline. It has a carrying capacity of 6,5 million litres per day.

20/ The pipeline is into 2 parts: Mozambique operates the CPMZ (Companhiado De Pipeline Mozambique-Zimbabwe) pipeline from the coastal town of Beira to Feruka in Mutare while the NOIC operates the Feruka-Mabvuku-Msasa (FMM) pipeline to depots in Harare.

21/ The CPMZ pipeline was built in 1966 to carry crude oil from Beira on the Mozambican coast to then Umtali in Rhodesia. At Umtali, an oil refinery was built by a consortium in which the principle partners were Mobil, Caltex, Total, Shell and BP.

22/ "These were the first companies marketing petroleum products in the then Rhodesia. This Umtali refinery could produce virtually all the oil products that Rhodesia needed. However, after the imposition of...sanctions in November 1965, the refinery was starved of crude oil."

23/ A confidential memorandum within Mobil (Rhodesia) stated: "When orders for lubricants and solvents are placed on our South African associates [(i.e. Mobil (South Africa)], a carefully planned "paper-chase" is used to disguise the final destination of these products.

24/ This was necessary in order 2 make sure that there was no link btwn MOSA (Mobil SA) & MOSR (Mobile Rhodesia) supplies . . . . This 'paper-chase' ...was done primarily to hide the fact that MOSA is in fact supplying MOSR with products in contravention of U.S. sanctions"

25/ The Gvt of ZW & CPMZ signed an agreement in 1982, which resulted in the CPMZ converting the Beira-Feruka pipeline from conveying crude oil to refined fuel.

26/ The FMM pipeline was built from 1987-1990 as a joint venture between the Gvt of ZW thru its company Petrozim Line & Lonrho. This also involved over 1,000 companies from Botswana, Zambia, Malawi & Zimbabwe under the name called Beira Corridor Group or BCG Limited.

27/ "This was completed by 1990 and partly in response to this initiative the Swedish government facilitated the construction of the largest underground storage facilities in the southern Africa region at Mabvuku in Harare."

theindependent.co.zw/2020/02/07/why…

theindependent.co.zw/2020/02/07/why…

28/ The underground multi product storage facility at Mabvuku Depot has a total capacity of 360 million litres as the single largest fuel storage and distribution facility in Southern Africa.

29/ National Infrastructure Company of Zimbabwe (NOIC) provides bulk transportation through the pipeline, storage & handling facilities of petroleum products.

NOIC came into existence out of the disbandment of National Oil Company of Zimbabwe (NOCZIM).

NOIC came into existence out of the disbandment of National Oil Company of Zimbabwe (NOCZIM).

30/ Created in 1983, #NOCZIM was disbanded in 2010 due to massive corruption scandals as it is usual when the state gets involved in business transactions.

Out of NOCZIM came out: NOIC & its petroleum retailing subsidiaries: Petrotrade & later Genesis Energy.

Out of NOCZIM came out: NOIC & its petroleum retailing subsidiaries: Petrotrade & later Genesis Energy.

31/ A regulatory authority, Zimbabwe Energy Regulatory Authority (ZERA) was then created in 2011.

@zeraenergy

zera.co.zw

@zeraenergy

zera.co.zw

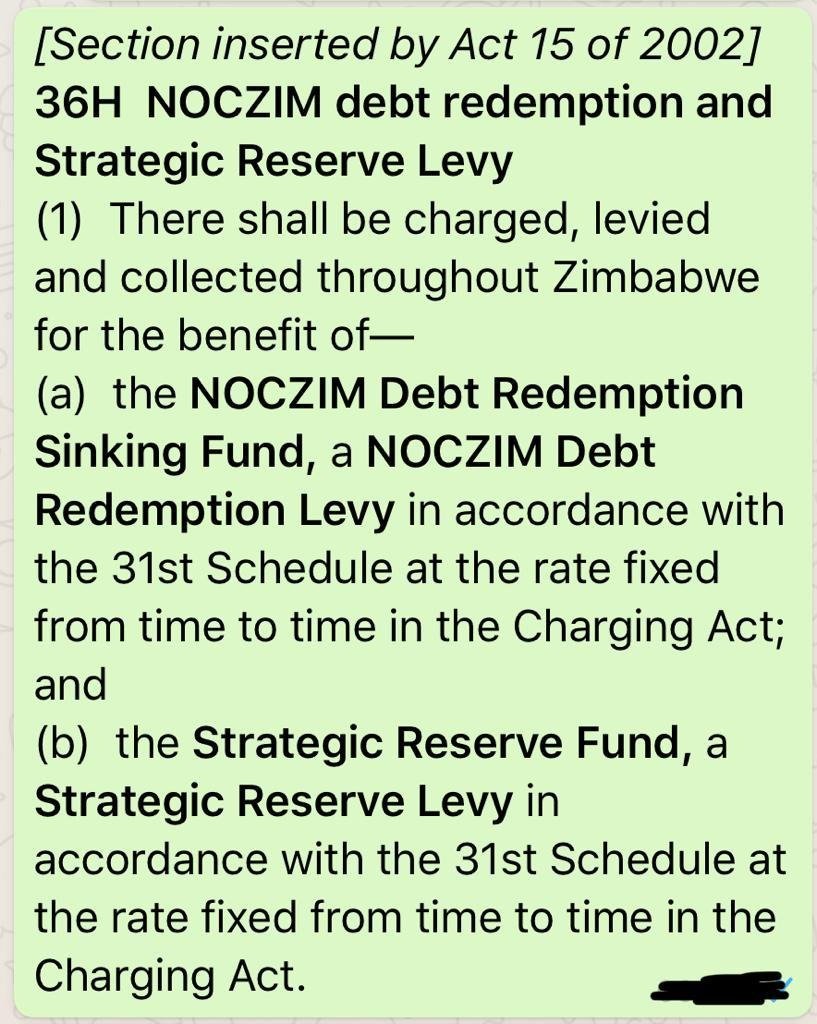

32/ The 1999 #NOCZIM corruption scandal led the Gvt to pass on its debts to the people of Zimbabwe by way of a #NOCZIMDebtRedemptionLevy introduced in 2003.

32 contd/ Finance Act: "The Noczim debt redemption levy was introduced by the Finance Act in 2003 to assist the company amortise its accumulated foreign debt that it has battled to settle despite previously enjoying monopoly over fuel trade."

33/Here were the US$158m debts:

1. Arab Foreign Bank (LAFB) &Tamoil (bothLibyan firms) US$44m

2. ZIMRA US$29,3m

3. Nordbanken US$24,6m

4. Dread Stock US$16,3m

5. BP South Africa US$12,7m

6. Buffer Stock $11,850m

7. CPMZ US$9,3m

8. Engen US$6,980m

9. Caltex (Chevron) US$2,6m

1. Arab Foreign Bank (LAFB) &Tamoil (bothLibyan firms) US$44m

2. ZIMRA US$29,3m

3. Nordbanken US$24,6m

4. Dread Stock US$16,3m

5. BP South Africa US$12,7m

6. Buffer Stock $11,850m

7. CPMZ US$9,3m

8. Engen US$6,980m

9. Caltex (Chevron) US$2,6m

34/ From the data mined in 2010 by the Ministry of Energy&Power Development from ZERA, ZIMRA & the Parliament Budget Office show that close to US$200 million had been raised for the #NOCZIM debt redemption fund since 2013.

35/ Using ZIMRA data, it showed that ZW imported 1,873 billion litres of petrol & 3,536 billion litres of diesel btwn 2013 & 2016, yielding about US$173m in levies paid into the #NOCZIMDebtRedemptionFund.

How much has been raised for the period 2003-2013 &from 2017 to date?

How much has been raised for the period 2003-2013 &from 2017 to date?

36/ The Auditor General’s 2015 audit found that Gvt used proceeds from the fund 2 finance its operations, beyond the redemption levy’s specific purpose.

37/ From September 2014, the fund was making monthly payments of US$2,7m to pay off a US$67m loan for unspecified “government operations” without Treasury approval, the audit noted.

38/ "The Gvt raised nearly US$200m between 2013 and 2016 from NOCZIM debt redemption levy, enough to pay off the parastatal’s legacy debts, but continues to tax consumers & diverting the cash to other expenses. - The Financial Gazette June 22, 2017.

39/ Whats the situation with the #NOCZIMDebtRedemptionLevy? Ko sei isiri kupera? Inopera rinhi? Yave marii yabhadharwa so far? How much is still outstanding & to whom? How much has been collected from the time it started in 2003?

40/ Ko icho chinonzi “Strategic Reserve Levy” chii?

Imarii yaunganidzwa so far & since when?

In what form is the Strategic Reserve Fund?

How has it been used?

Have there been any audited financial statements of the fund?

Imarii yaunganidzwa so far & since when?

In what form is the Strategic Reserve Fund?

How has it been used?

Have there been any audited financial statements of the fund?

42/ #PetroleumFinancing & Pricing

i. End users of petroleum products in ZW are currently paying those licensed as retailers (service stations) in local currency (LX).

i. End users of petroleum products in ZW are currently paying those licensed as retailers (service stations) in local currency (LX).

42/ ii. Retailers pay using LX to #PetroleumMarketingCompanies (#PMCs), who are those with a procurement license to buy directly from importers.

To be a PMC, one needs to have a minimum of 25 of own or franchisee service stations.

To be a PMC, one needs to have a minimum of 25 of own or franchisee service stations.

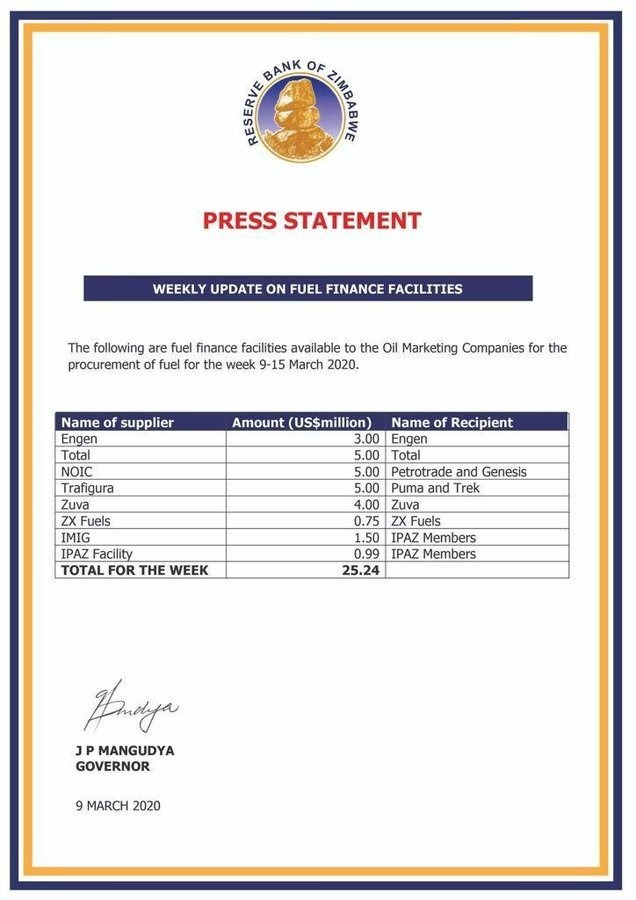

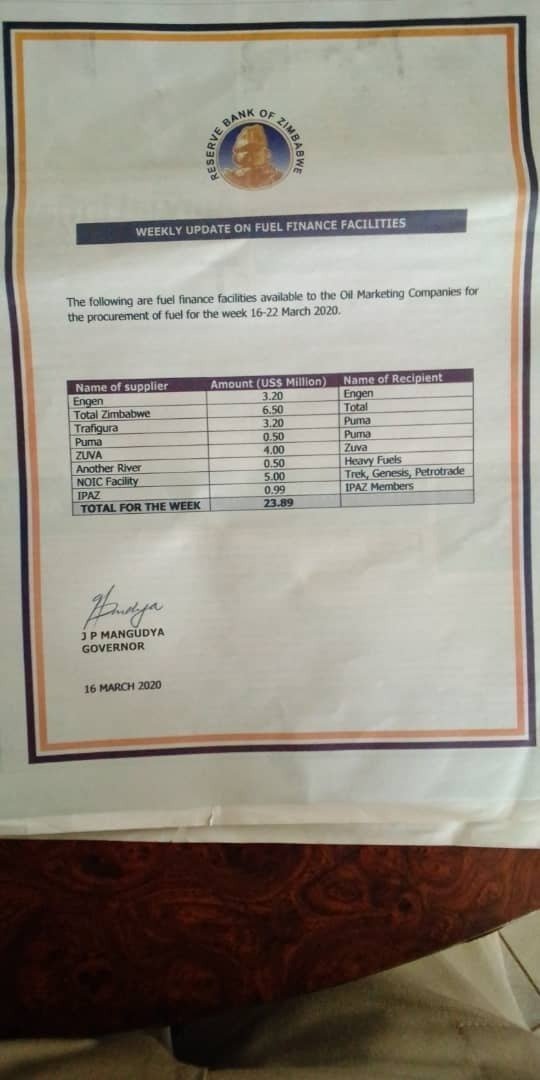

42/ iii. The PMCs (Procurer/Wholesaler) pay the importer in LX (they all have local accounts). The Wholesalers submit the LX to RBZ in exchange of FX only for the agreed allocation which is those press statements from RBZ that it published weekly in March 2020.

42/

iv. The state/RBZ has two sources of foreign currency (FX):

a) that which is expropriated from exporters &

b) that which is buys from the market (interbank or parallel).

v. Its this FX that the RBZ allocates thru the fuel financing facility.

iv. The state/RBZ has two sources of foreign currency (FX):

a) that which is expropriated from exporters &

b) that which is buys from the market (interbank or parallel).

v. Its this FX that the RBZ allocates thru the fuel financing facility.

43/ So end-users buy fuel in LX from retailers. The retailers then pay for the fuel from PMCs in LX, who are the wholesalers & are the ones licensed to procure from importers.

Based on an allocation system, the RBZ receives the LX from the importers & then pays them FX.

Based on an allocation system, the RBZ receives the LX from the importers & then pays them FX.

44/ Upon receipt of the FX, the importer gives NOIC a "release order," which is a written instruction to release fuel from Msasa for a named PMC.

45/ By implication, the fuel price is thus being determined by the state as the fuel can’t be sold at a market price.

If it was determined by the market, the cost of money to import fuel in ZW would be the parallel rate bcoz that’s where one can only get FX.

If it was determined by the market, the cost of money to import fuel in ZW would be the parallel rate bcoz that’s where one can only get FX.

46/ Without this state determination of the fuel price, the fuel would have been based on the prevailing parallel exchange rate.

Therefore, to keep the fuel cheap, the state determines the fuel price by financing the fuel importation FX requirements.

Therefore, to keep the fuel cheap, the state determines the fuel price by financing the fuel importation FX requirements.

47/ Since it’s not market based and that the state doesn’t enough FX at its disposal, there is going to be a deficit at all times leading to fuel shortages.

This is why even during lockdown, there are still fuel shortages bcoz the RBZ doesnt have the FX to finance it.

This is why even during lockdown, there are still fuel shortages bcoz the RBZ doesnt have the FX to finance it.

48/ There is a likelihood that some retailers can sell fuel at FX-based prices & then pay PMCs in LX.

There is also a likelihood that PMCs can sell to bulk end users like corporates at FX-based prices & starve the retailers.

There is also a likelihood that PMCs can sell to bulk end users like corporates at FX-based prices & starve the retailers.

49/ How is the state able to monitor if all the fuel procured through that FX allocation arrangement is sold at state-determined price?

50/ The state is funding the cost of fuel & therefore determining the price at which the fuel shld be sold. The amount of funding isnt up to the supply requirements of the market & therefore this is constraining the demand of the product.

51/ When the state is determining, fixing & controlling all the 4 factors of a product: cost, price, supply & demand, it ceases to be a viable commercial business.

52/ The only source of FX for the state/RBZ is the surrendered FX from exporters' earnings.

53/ The RBZ ends up with lots of LX from PMCs thru importers. It uses the LX to buy FX from the interbank or parallel market bcoz expropriated amounts are never enough.

54/ This results in 2 effects:

i) fuel price is kept low & highly regulated by ZERA since PMCs are allocated artificially priced FX; &

ii) parallel market rates are constantly pushed upwards as the RBZ seeks FX to buy to allocate for fuel.

i) fuel price is kept low & highly regulated by ZERA since PMCs are allocated artificially priced FX; &

ii) parallel market rates are constantly pushed upwards as the RBZ seeks FX to buy to allocate for fuel.

55/ This means the RBZ is using LX in its left hand side (from importers having been paid by the PMCs) to pay for the FX in its right hand (from expropriation of exporter earnings & what it buys from both interbank & parallel markets).

56/ The state is in a quandary:

i. By allocating FX it doesnt have or produce. Any statist allocation system will cause serious shortages.

ii. If it is to stop the allocations, it means it has to stop the expropriation of FX earnings from exporters&gold miners.

i. By allocating FX it doesnt have or produce. Any statist allocation system will cause serious shortages.

ii. If it is to stop the allocations, it means it has to stop the expropriation of FX earnings from exporters&gold miners.

56/

iii. This will improve the supply of FX into the market from exporters.

iv. The RBZ monetary behaviour of starving the market of FX by the surrender policy & at the same time go into the same market to buy FX at the parallel rate will keep the exchange rate UNSTABLE.

iii. This will improve the supply of FX into the market from exporters.

iv. The RBZ monetary behaviour of starving the market of FX by the surrender policy & at the same time go into the same market to buy FX at the parallel rate will keep the exchange rate UNSTABLE.

56/

v. Keeping the exchange rate stable makes it easier for the state to allow PMCs to buy FX from the market where one finds FX.

The fixed interbank rate of 25 would have been unthinkable in June 2018.

For the period 2009-2016, there were hardly fuel shortages.

v. Keeping the exchange rate stable makes it easier for the state to allow PMCs to buy FX from the market where one finds FX.

The fixed interbank rate of 25 would have been unthinkable in June 2018.

For the period 2009-2016, there were hardly fuel shortages.

With this thread, I humbly request the media to be factual on the subject of fuel shortages.

@fortunechasi @zimlive

@ZimFact @newswireZW @kukurigoZW @NewsDayZimbabwe @HeraldZimbabwe @SundayMailZim @DailyNewsZim @WeArePindula @zeraenergy @official_MOEPD @ZimTreasury @MinOfInfoZW

@fortunechasi @zimlive

@ZimFact @newswireZW @kukurigoZW @NewsDayZimbabwe @HeraldZimbabwe @SundayMailZim @DailyNewsZim @WeArePindula @zeraenergy @official_MOEPD @ZimTreasury @MinOfInfoZW

Please pay attention to posts #33-40 and #42-56.

Hard decisions need to be taken!

Hard decisions need to be taken!