Q2 and FY 2020 Projections Update (Thread)

I'm projecting GAAP NI of $166M, adjusted EPS of $2.30, and for most analysts to be utterly confused about how Tesla pulled off these kind of numbers during a pandemic when their primary plant was shut down for half the quarter.

I'm projecting GAAP NI of $166M, adjusted EPS of $2.30, and for most analysts to be utterly confused about how Tesla pulled off these kind of numbers during a pandemic when their primary plant was shut down for half the quarter.

My delivery estimate is 100,500 units as discussed in the thread linked below. If you think this is too high, please hold that thought, as we'll do a sensitivity with lower deliveries at the end. What I really want to walk through in detail is FSD.

Most analysts out there isolate regulatory credits so that they can adjust those out and have a better understanding of the "real" gross margins of the auto business. I contend that we should be doing the same thing for FSD revenues, although it is admittedly much harder.

FSD prices are increasing over time, and there is good reason to believe that with additional functionality, take-rates and upgrades will continue to grow as well. If this is true, FSD will account for a growing portion of automotive gross margin.

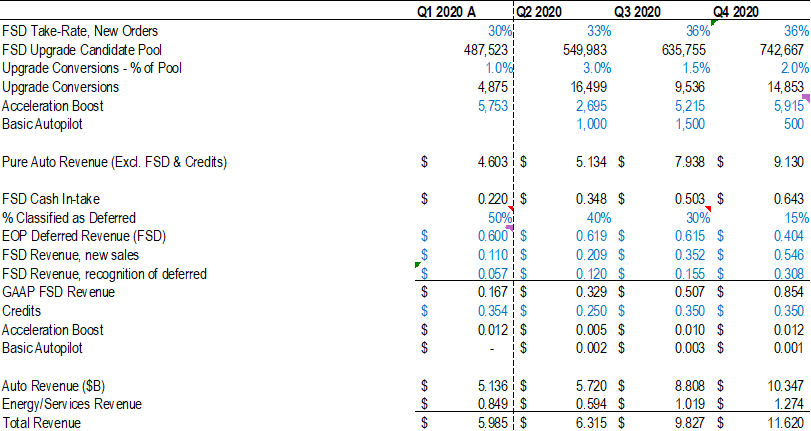

For the past several quarters, I have been estimating FSD take rates, as well as the percentage of sales which are GAAP recognizable in order to isolate that portion of automotive gross margin. Tesla gave me a gift last quarter by disclosing that FSD revs were ~50% recognizable.

In Q1 there was not very much new functionality added to autopilot, and in fact Tesla disclosed that only $57M of deferred revenue was recognized. Tesla also disclosed late last year that take rates for FSD were around 27%.

Taking these data points, we can start to model out FSD revenues, as well as how many people have not purchased FSD, and who are therefore candidates for future revenue should they opt for an upgrade. Here's the top level build-up for Automotive revenues.

In contrast to Q1, in Q2 there was LOTS of progress made on FSD. City-street driving was rolled out in the US, and additional functionality was made available in other geographies. This means that it is highly probable that the amount of FSD revenue classified as deferred...

will drop. I'm projecting decline from 50% to 40%, which may be conservative. Even so, this one change allows Tesla to immediately recognize $120M of the $600M in deferred revenue currently on their balance sheet. On top of that, new FSD sales will be more profitable.

Additionally, the improved functionality and impending price increase will prompt some portion of the pool of previous "Non-Takers" to opt for an upgrade. I've estimated this to be 3% of the pool of ~500K upgrade candidates.

Combining the FSD upgrades, recognition of deferred revenue, and the recognition of new sales, I expect total GAAP FSD margin to double quarter over quarter from $167M to $329M. Bearing in mind that this is all pure margin revenue, this will be a trojan horse in the Q2 numbers...

as I can guarantee you that wall street analysts are not modeling out this level of detail, especially since Tesla does not provide these details. Aside from getting an accurate view of FSD margins, the other thing this modeling allows us to do is to isolate Tesla's core...

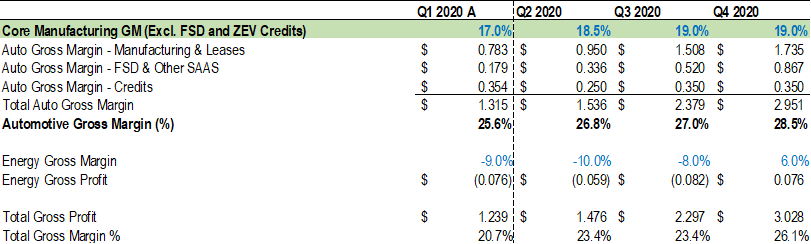

automotive manufacturing margin. In other words I can take the revenue build-up from above, and strip out the FSD and Credit revenues from historical periods. When I did that for Q1, I calculated a Core Manufacturing Gross Margin for Tesla of 17.0%.

We also know that the MIC Model 3 and the Model Y are significantly higher margin products than the US-made Model 3. In Q1, those high margin products accounted for approximately 18% of total deliveries. In Q2 those should account for closer to 50% of total deliveries!

This has significant implications for the Core Manufacturing Margin. This line item could very well be north of 20% given the huge shift from Q1 to Q2, however I have modeled a modest increase from 17.0% to 18.5%.

Now adding all the pieces back together, including $250M of credit sales, we have total Automotive Gross Margin of over $1.5B, and 26.8% as reported. If Tesla is able to achieve these figures, they will leave many analysts completely dumbfounded, and $TSLAQ crying fraud.

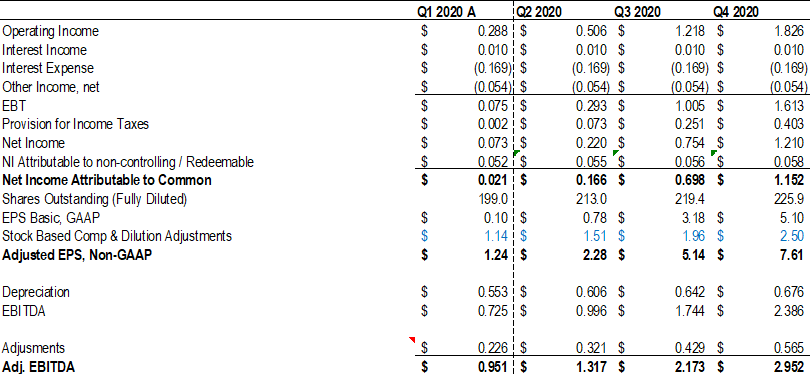

The rest of the forecast is less exciting, but I'm projecting a decline in Energy & Services revenue and margin, given the restrictions with Coronavirus. I also expect a 10% decrease QoQ on SG&A, as the company tightened its belt in response to the pandemic.

After lenghty consultation with both @ICannot_Enough and @jamescranecpa, I've landed on a slight acceleration of some of the vesting of the CEO SBC tranches, meaning $79M in Q2.

This leads to $500M of Operating Income, $166M of GAAP NI, $1.3B in Adjusted EBITDA (hat tip @freshjiva) and an all-around good quarter for the Tesla Bulls.

Now, I can understand if all that seems overly bullish to you, so I'd also like to include an alternate "bear" using different assumptions but the same overall methodology. Assuming 80K deliveries, a 27% FSD take rate, flat Core Manufacturing Margin and only $50M of credit...

revenues, Tesla would post a GAAP loss and miss S&P inclusion, but would still beat adjusted EPS estimates by nearly $2. This seems possible to me, but honestly all of the assumptions seem to conservative. The fact that my bear case is higher than analyst estimates...

and my base case is an absolute blow-out gives me a lot of confidence on the upside potential of the stock in the near- to medium-term. @threadreaderapp unroll