"Live the Library" with Charlie Munger - a thread.

After being inspired by @djrosent to finally sit down and read "Poor Charlie's Almanack" I spent a good chunk during quarantine reading it each morning.

I'll still be internalizing for a long time.

After being inspired by @djrosent to finally sit down and read "Poor Charlie's Almanack" I spent a good chunk during quarantine reading it each morning.

I'll still be internalizing for a long time.

https://twitter.com/djrosent/status/1252752719636381696?s=20

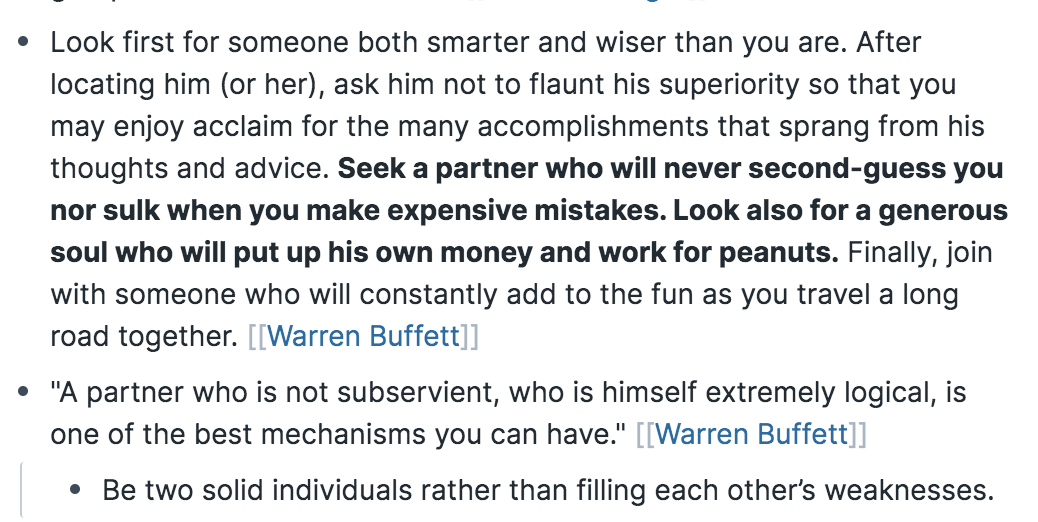

1/ Only right to start a conversation about Charlie Munger by diving into the relationship with Warren Buffett.

Don't find a partner who covers your weaknesses. Be two complete people. Maximize your strengths.

Then be better together.

Don't find a partner who covers your weaknesses. Be two complete people. Maximize your strengths.

Then be better together.

2/ "I’ve gotten paid a lot over the years for reading through the newspapers." (Charlie Munger)

Hot take: Buffett + Munger's success comes from being (1) information ingestion / output machines and (2) insurance float. Maybe I'm wrong?

Hot take: Buffett + Munger's success comes from being (1) information ingestion / output machines and (2) insurance float. Maybe I'm wrong?

3/ Convo between me and @LennyIce

Munger/Buffett had (1) insane computer-level information ingestion/output and (2) insurance float.

Similarly, my outside-in view is @awilkinson has (1) unbelievable honesty / delegation and (2) software margins.

Maybe over simplifying.

Munger/Buffett had (1) insane computer-level information ingestion/output and (2) insurance float.

Similarly, my outside-in view is @awilkinson has (1) unbelievable honesty / delegation and (2) software margins.

Maybe over simplifying.

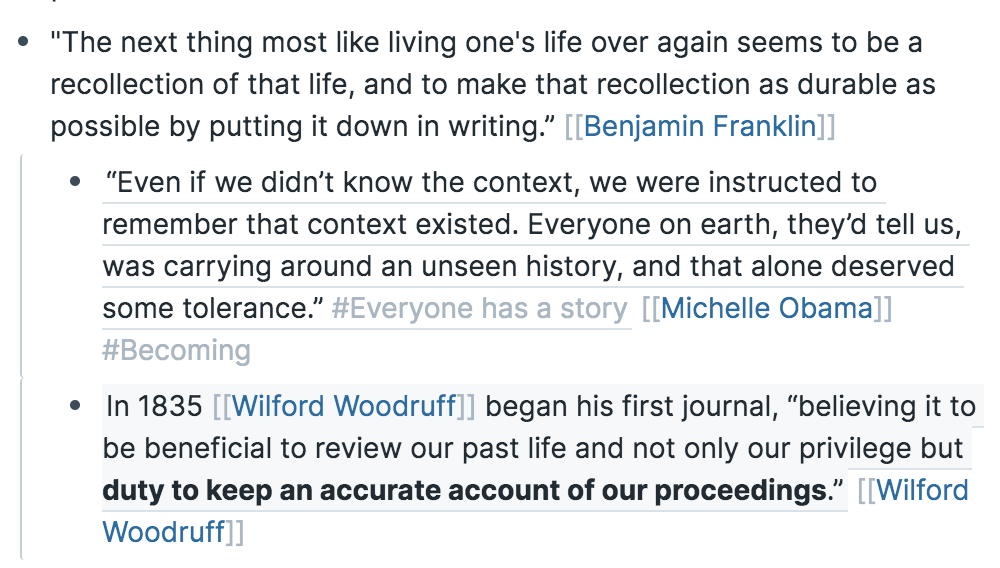

4/ Everyone should keep a personal history.

Journals. Letters. Notes. Emails.

Take a long-term view. Backwards and forwards. Learn about your parents; grandparents. And make life easier for you kids; grand-kids.

Journals. Letters. Notes. Emails.

Take a long-term view. Backwards and forwards. Learn about your parents; grandparents. And make life easier for you kids; grand-kids.

5/ Find the people who you can talk with for hours and leave wishing you had endless hours.

Hours that you could keep talking to them. Hours learning more deeply about the things they've just taught you.

Hours to do the things you're inspired to do after talking to them.

Hours that you could keep talking to them. Hours learning more deeply about the things they've just taught you.

Hours to do the things you're inspired to do after talking to them.

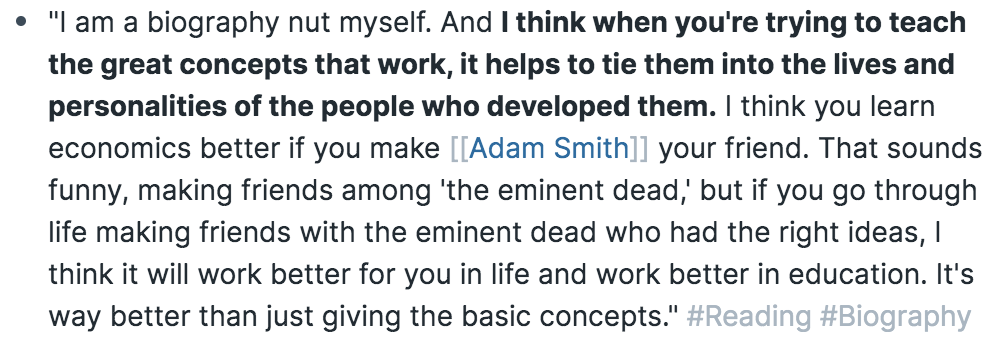

6/ I would rather read a biography about someone in a field than a book about the field itself.

"Everybody has a plan until they get punched in the face."

Learn how other people have dealt with the blows life deals them and maybe you'll handle yours that much better.

"Everybody has a plan until they get punched in the face."

Learn how other people have dealt with the blows life deals them and maybe you'll handle yours that much better.

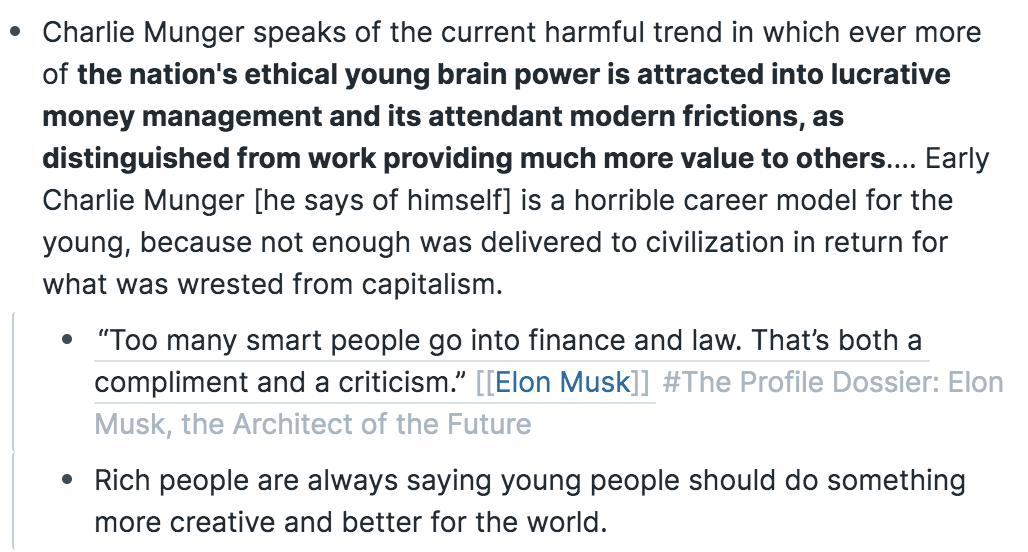

7/ Reminded me of the Elon Musk profile by @polina_marinova

"Too many smart people go into finance."

Timely this week when Elon Musk's net worth passes Warren Buffett.

No matter your career; ask yourself "What am I selling?" And then ask if you would buy it.

"Too many smart people go into finance."

Timely this week when Elon Musk's net worth passes Warren Buffett.

No matter your career; ask yourself "What am I selling?" And then ask if you would buy it.

8/ "Life's tragedy is that we get old too soon and wise too late. When you're finished changing, you're finished."

(Benjamin Franklin)

“Once you stop learning, you start dying.” (Albert Einstein)

(Benjamin Franklin)

“Once you stop learning, you start dying.” (Albert Einstein)

9/ "Take a simple idea and take it seriously." (Charlie Munger)

"The only way to win is to work, work, work, work, and hope to have a few insights." (Charlie Munger)

"The only way to win is to work, work, work, work, and hope to have a few insights." (Charlie Munger)

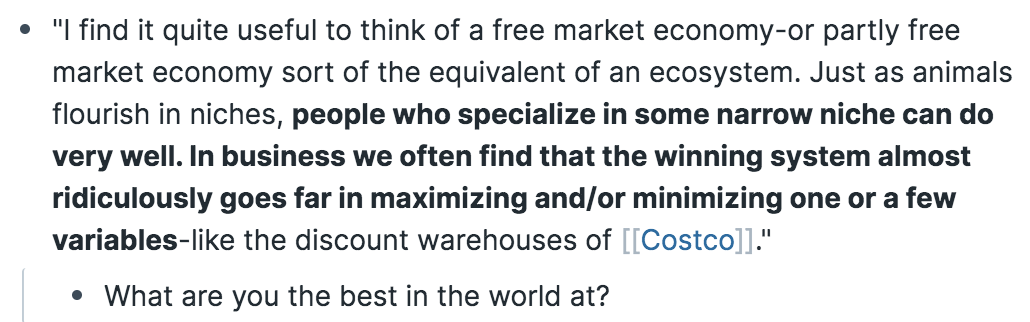

10/ "What are you the best in the world at?"

You don't have to know every business in and out. But you have to know something, and know it well.

You don't have to know every business in and out. But you have to know something, and know it well.

11/ Adopting a "spirit of humility."

Everyone is convinced that they're so often right that they would exert significantly more energy to proving themselves right than working to see if they might be wrong.

Everyone is convinced that they're so often right that they would exert significantly more energy to proving themselves right than working to see if they might be wrong.

https://twitter.com/kwharrison13/status/1282115666435207173?s=20

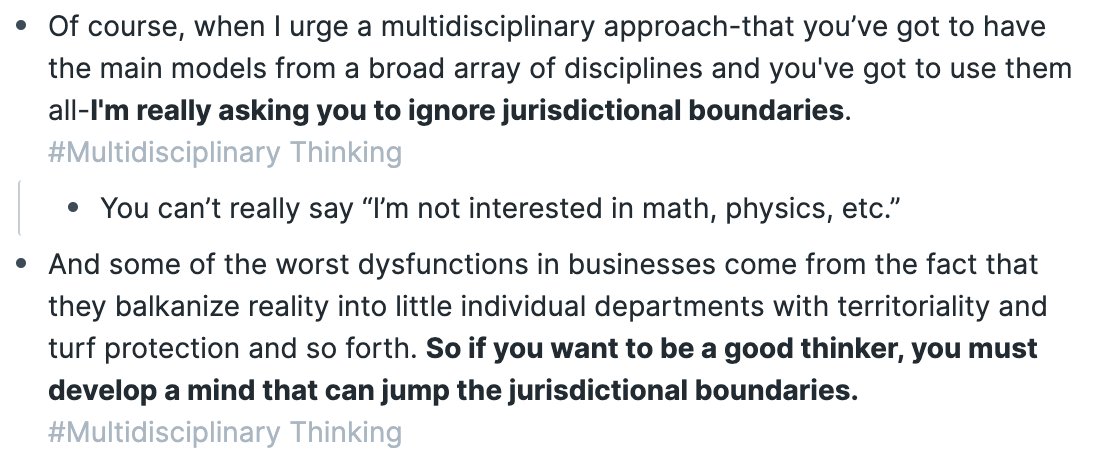

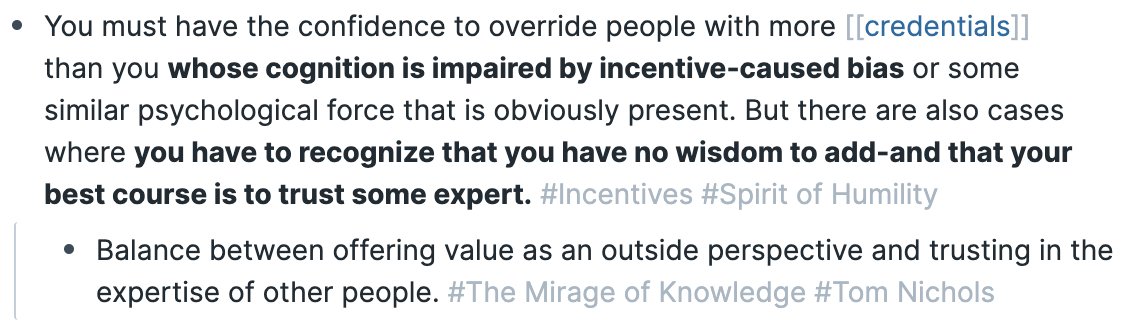

12/ People saying "I'm not good at math" or "I don't like reading fiction" are inherently bound by intellectual jurisdictions.

Multidisciplinary thinking is based on the ability to take any field and ask "what can I take from this?"

Be an idea thief.

Multidisciplinary thinking is based on the ability to take any field and ask "what can I take from this?"

Be an idea thief.

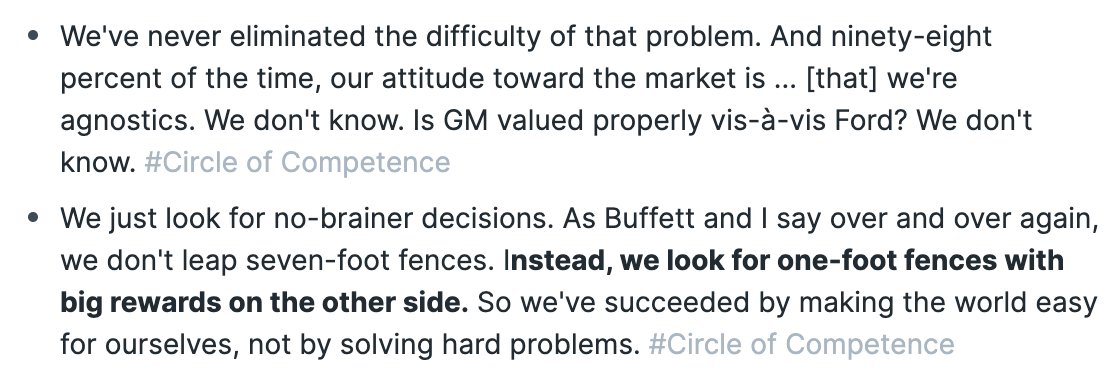

13/ We need people to solve hard problems.

But sometimes even the people solving hard problems need to stop and ask if they're jumping over seven-foot fences for no reason.

But sometimes even the people solving hard problems need to stop and ask if they're jumping over seven-foot fences for no reason.

https://twitter.com/chetanp/status/1297014703831445504?s=20

https://twitter.com/iramneek/status/1296049917404667904?s=20

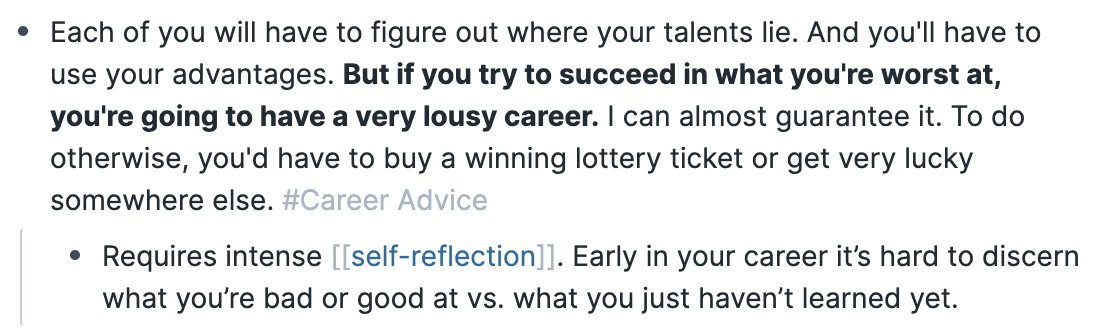

14/ When you're mapping out your career, ask yourself, "what can I be really good at?"

But don't confuse what you're not good at vs. what you haven't learned yet.

People should try their hand at a lot more jobs than they currently do.

But don't confuse what you're not good at vs. what you haven't learned yet.

People should try their hand at a lot more jobs than they currently do.

https://twitter.com/kwharrison13/status/1282112358689542145?s=20

15/ Know when you should trust your gut because the experts are totally misincentivized. But also know when to trust expertise.

"In effect, you've got to know what you know and what you don't know. What could possibly be more useful in life than that?"

harvardmagazine.com/2018/03/death-…

"In effect, you've got to know what you know and what you don't know. What could possibly be more useful in life than that?"

harvardmagazine.com/2018/03/death-…

16/ "I’ve noticed that amazing books can’t be read quickly because I have to put the book down and think/process what I’ve learned." @AlexAndBooks_

"I needed to engage with the books I read on a much deeper level. I needed to make something out of them." @fortelabs

"I needed to engage with the books I read on a much deeper level. I needed to make something out of them." @fortelabs

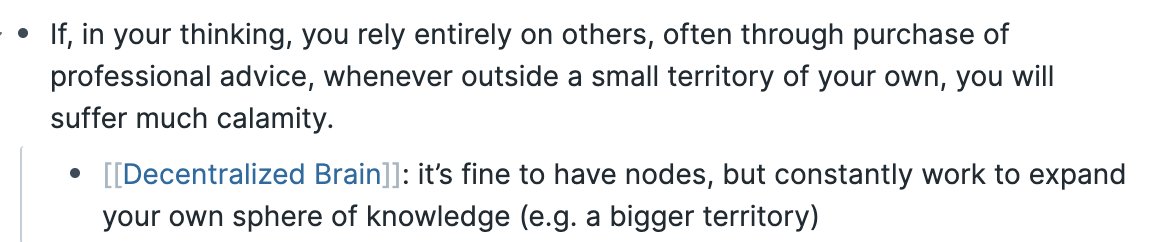

17/ I have this idea of building a "decentralized brain."

People are my nodes. I can't live a life as a lawyer so I have a lawyer friend as a node. I have a blockchain node. A history node. A physics node.

Then I work to expand my circle of competence so I'm not node dependent

People are my nodes. I can't live a life as a lawyer so I have a lawyer friend as a node. I have a blockchain node. A history node. A physics node.

Then I work to expand my circle of competence so I'm not node dependent

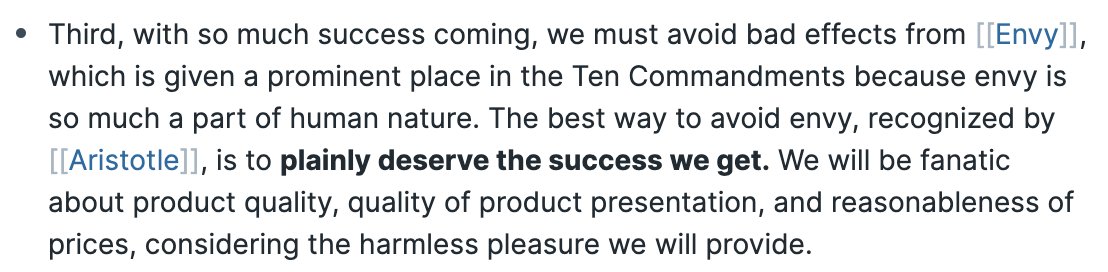

18/ People give Munger credit for the idea "deserve the partner you want."

But it's a remix from the album "Aristotle's Greatest Hits"

“The best way to avoid envy is to deserve the success you get.”

But it's a remix from the album "Aristotle's Greatest Hits"

“The best way to avoid envy is to deserve the success you get.”

https://twitter.com/Conaw/status/1294574651494952960?s=20

19/ One of the most powerful ideas I've seen recently:

"Before you deserve to hold a strong opinion you should be able to argue the counter-argument better than those who wish to disagree with you."

If you want to have faith in God, embrace religious apologetics

"Before you deserve to hold a strong opinion you should be able to argue the counter-argument better than those who wish to disagree with you."

If you want to have faith in God, embrace religious apologetics

20/ Teaching is not easy, nor should it be.

The best advice I've heard is "Simplify, and Intensify."

Side note: Have the humility to acknowledge when you could have done something better, even when you did well.

The best advice I've heard is "Simplify, and Intensify."

Side note: Have the humility to acknowledge when you could have done something better, even when you did well.

Listening to @BrentBeshore and @patrick_oshag on @InvestLikeBest talking about how they've been chatting for 10 hours and decided to record an episode, you can feel that same kind of friendship.

investorfieldguide.com/adventures/

investorfieldguide.com/adventures/

21/ "Increasing your confidence without increasing your accuracy is the most dangerous thing you can do." @verdadcap

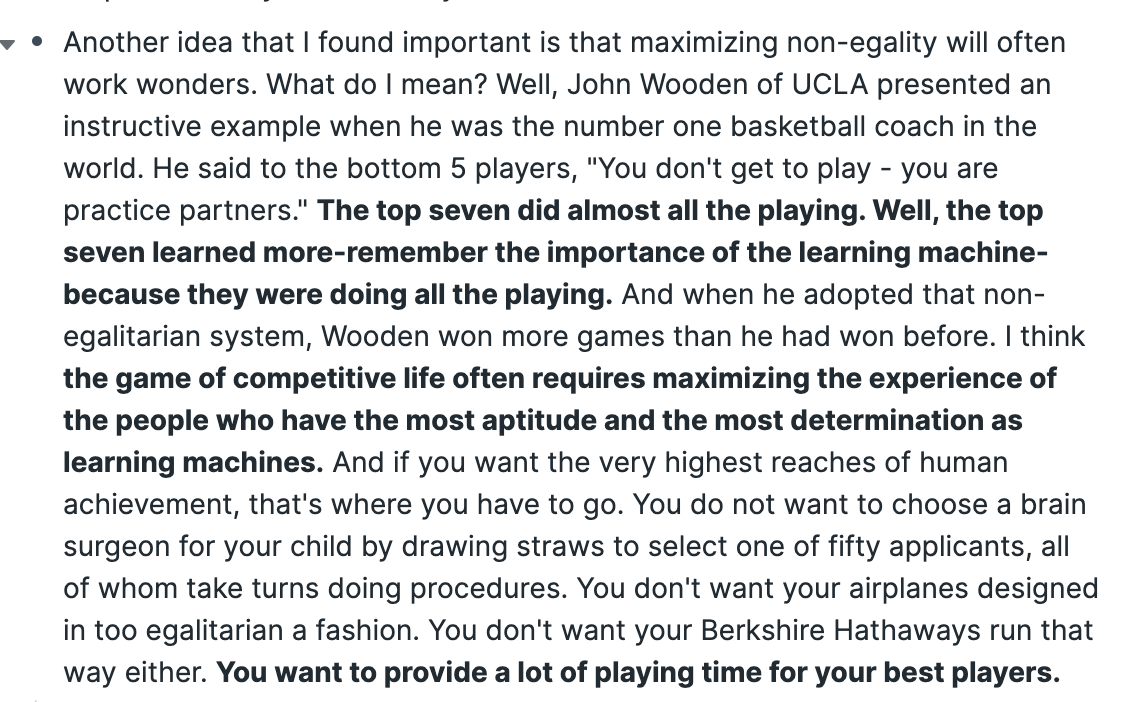

23/ If people weren't so distracted by all the money Charlie Munger had made as an investor they might spend more time thinking about the educational philosopher that he was.

24/ People have confused science and opinion because they're unsure and to become sure is far too complicated.

The ethos of "do whatever you want, harm no one" leads to the same ends of "take what you like, ban what you hate."

Our mental models need upgrades of reality checks

The ethos of "do whatever you want, harm no one" leads to the same ends of "take what you like, ban what you hate."

Our mental models need upgrades of reality checks

25/ Fascinating idea. A lot of the world's problems aren't getting solved because they exist in isolated silos.

Maybe we haven't cured cancer yet because the right marine biologist hasn't talked to the right nuclear physicist.

Maybe we haven't cured cancer yet because the right marine biologist hasn't talked to the right nuclear physicist.

https://twitter.com/kwharrison13/status/1269072518817525760?s=20

26/ People sometimes dismiss the idea of finding your "circle of competence" because it means you can't learn.

Expanding that circle is just as important as having one. But knowing what is in your circle of competence and what is NOT is the way to avoid overconfidence.

Expanding that circle is just as important as having one. But knowing what is in your circle of competence and what is NOT is the way to avoid overconfidence.

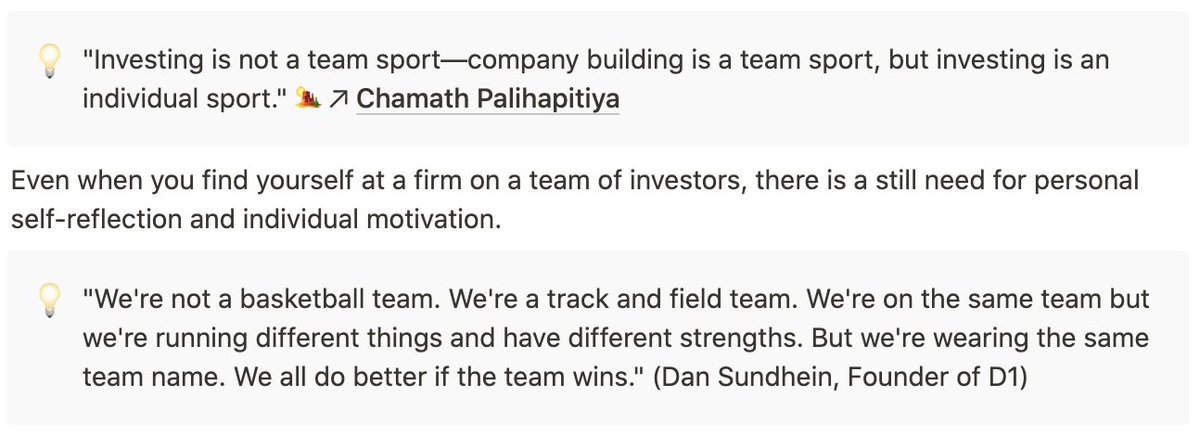

27/ "Investing is not a team sport." @chamath

"There is no limit to what a man can do or where he can go if he doesn't mind who gets the credit." Robert Woodruff, former CEO of Coca-Cola

One team, one dream? Or all about who gets the credit?

"There is no limit to what a man can do or where he can go if he doesn't mind who gets the credit." Robert Woodruff, former CEO of Coca-Cola

One team, one dream? Or all about who gets the credit?

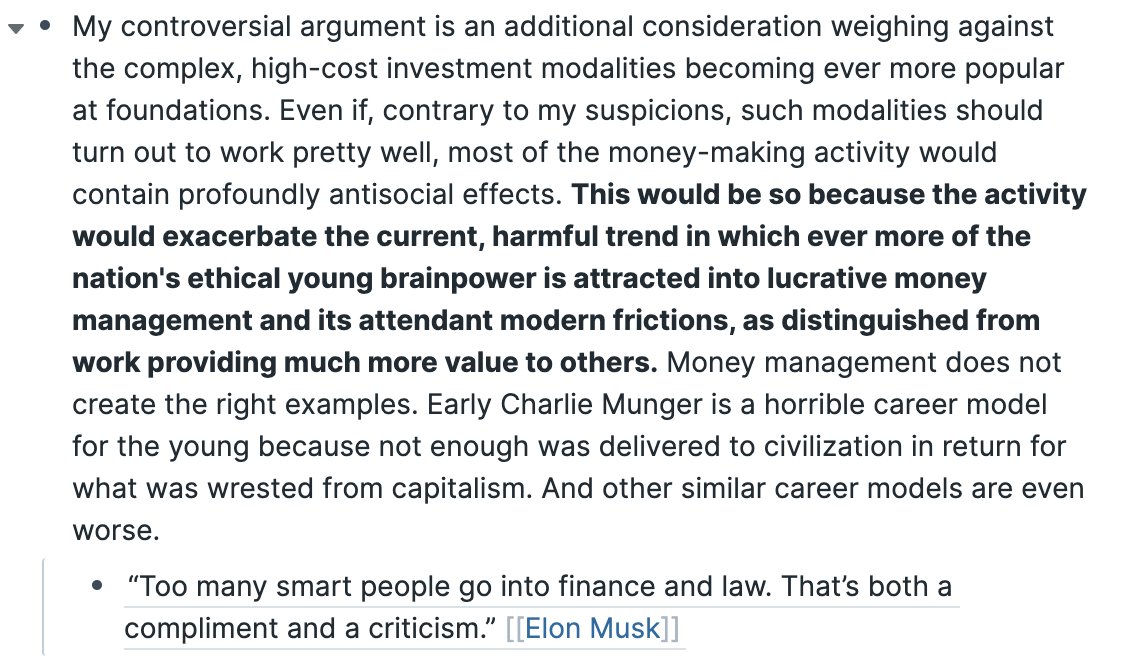

28/ “Too many smart people go into finance and law. That’s both a compliment and a criticism.” @elonmusk

credit: @polina_marinova

theprofile.substack.com/p/the-profile-…

credit: @polina_marinova

theprofile.substack.com/p/the-profile-…

29/ There is a difference between money managers that Munger and Buffett deride and an investor

The world needs fewer people who move money for making money's sake. The world needs more people allocating resources to the best ideas

cc @eriktorenberg

The world needs fewer people who move money for making money's sake. The world needs more people allocating resources to the best ideas

cc @eriktorenberg

https://twitter.com/kwharrison13/status/1296980915004928000?s=20

30/ @andy_matuschak has made a comment that he's amazed by how little knowledge workers spend time thinking about knowledge.

Eventually you will either pay the price in time and money to have a thinking tool (like @RoamResearch) or you will pay for not having one.

Eventually you will either pay the price in time and money to have a thinking tool (like @RoamResearch) or you will pay for not having one.

31/ "We all agree that pessimism is a mark of superior intellect." [[John Kenneth Galbraith]]

If you find yourself in a situation where you LOVE telling people why their ideas are stupid you probably need to seek satisfaction elsewhere.

If you find yourself in a situation where you LOVE telling people why their ideas are stupid you probably need to seek satisfaction elsewhere.

32/ People find countless ways to add complexity in hopes of finding specks when "with a little intelligence" you could find truly big ideas.

Big ideas don't have to be big $ amounts.

Big ideas don't have to be big $ amounts.

https://twitter.com/awilkinson/status/1262449756686540801?s=20

33/ The only thing you can know about a forecast with 100% certainty is that it is wrong.

Forecasting ought to be a difficult mental exercise where you're trying to understand effects of effects.

You're not looking for the right number. You're looking for the right magnitude.

Forecasting ought to be a difficult mental exercise where you're trying to understand effects of effects.

You're not looking for the right number. You're looking for the right magnitude.

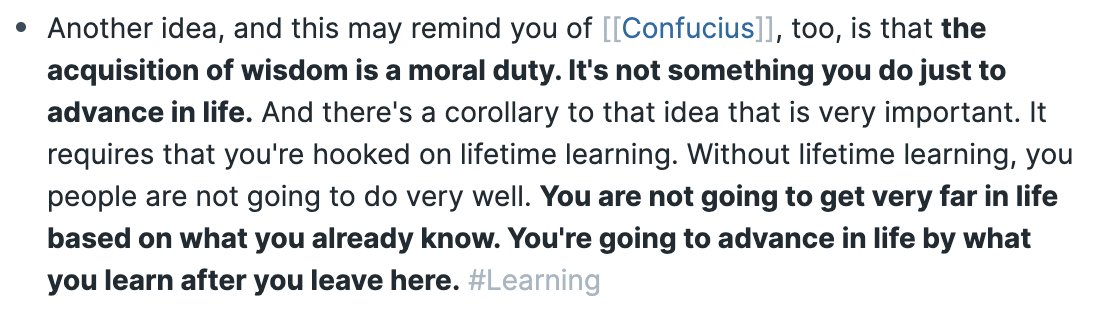

34/ "The acquisition of wisdom is a moral duty."

"An educated citizenry is a vital requisite for our survival as a free people."

"Where is the wisdom we have lost in knowledge? Where is the knowledge we have lost in information?"

"An educated citizenry is a vital requisite for our survival as a free people."

"Where is the wisdom we have lost in knowledge? Where is the knowledge we have lost in information?"

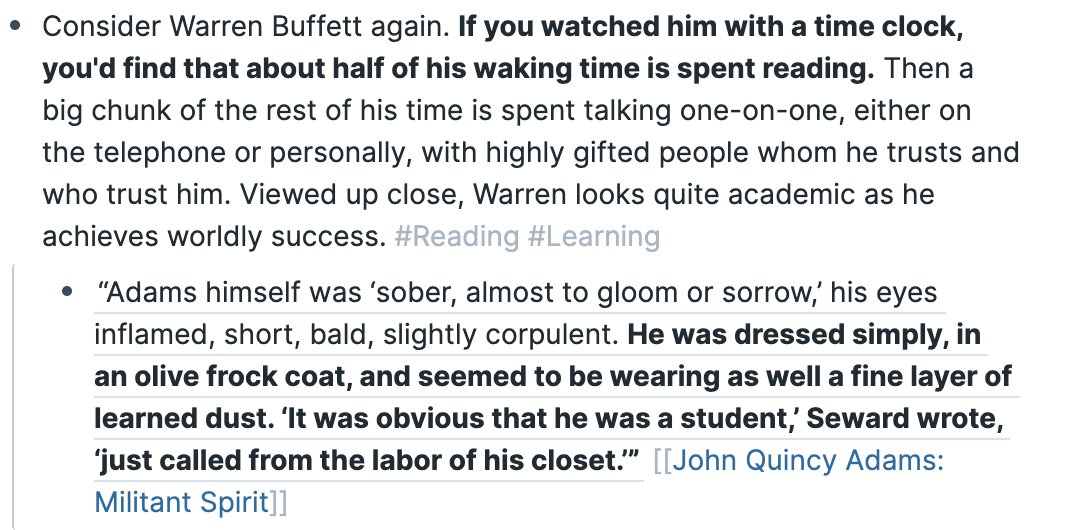

35/ Really smart people read as much as possible. They consume information from people, books, movies, experiences.

36/ “It is dangerous to be right in matters where established men are wrong." [[Voltaire]]

Find the balance between taking on contrarian stances you feel strongly about and having a spirit of humility to learn from those around you / more senior than you.

Find the balance between taking on contrarian stances you feel strongly about and having a spirit of humility to learn from those around you / more senior than you.

37/ In my religion I often ask myself "why I believe."

Invert, always invert.

"Why wouldn't I believe?" Explore the counterarguments to your belief and you'll come out stronger if you still hold that belief.

cc: @BrentBeshore

Invert, always invert.

"Why wouldn't I believe?" Explore the counterarguments to your belief and you'll come out stronger if you still hold that belief.

cc: @BrentBeshore

38/ Are you self-aware enough and incentivized correctly to acknowledge when you might not be the best player to play?

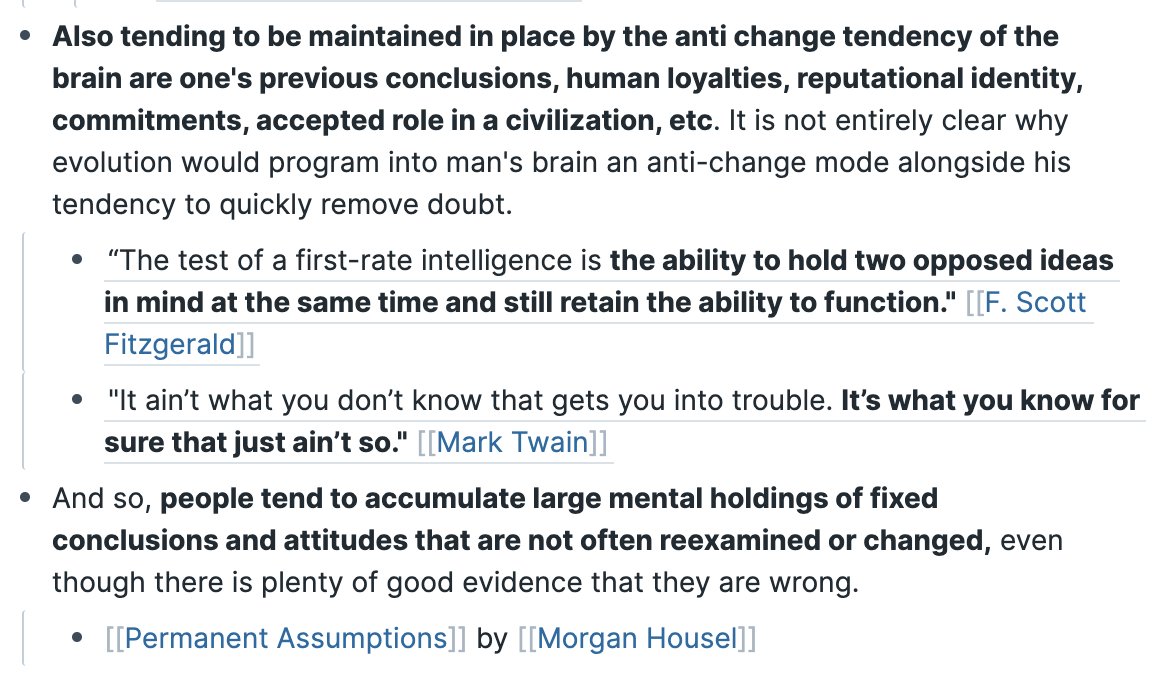

39/ When it comes to "human misjudgment" the gateway sin is refusing to change your mind because it forcibly locks down every other misjudgment and stops you from improving.

https://twitter.com/kwharrison13/status/1318552255314956290?s=20

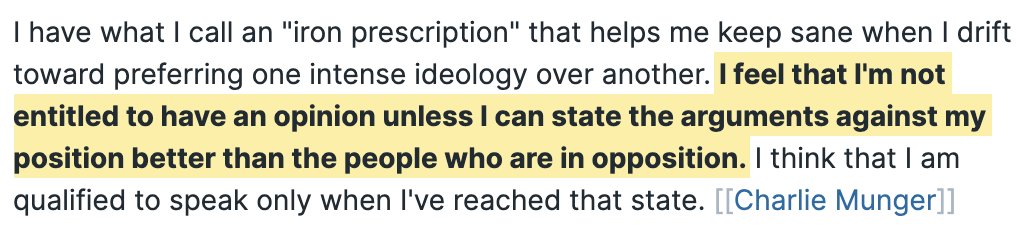

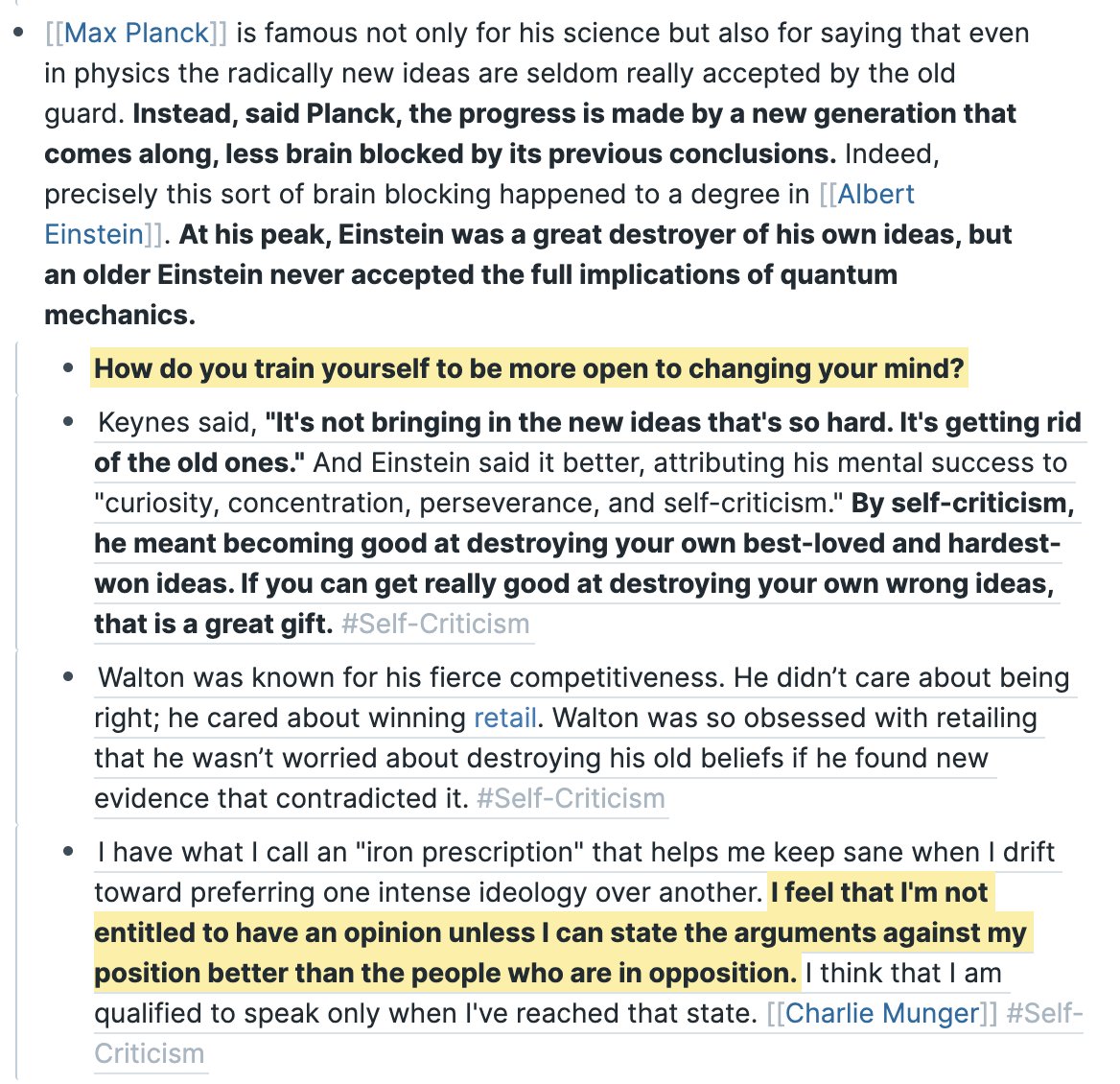

40/ "Self-Criticism" may be one of the most important ideas I've taken away from Charlie Munger.

"I feel that I'm not entitled to have an opinion unless I can state the arguments against my position better than the people who are in opposition."

"I feel that I'm not entitled to have an opinion unless I can state the arguments against my position better than the people who are in opposition."

41/ Rome vs. Athens. Practical vs. imagination.

"Part of the problem is clearly foresight, a failure of imagination." @pmarca

“Too many smart people go into finance and law. That’s both a compliment and a criticism.” @elonmusk

"Part of the problem is clearly foresight, a failure of imagination." @pmarca

“Too many smart people go into finance and law. That’s both a compliment and a criticism.” @elonmusk

42/ Munger has me thinking about fairness. In a world where we wish we had more fairness the deepest regions of my @RoamResearch graph brought me these gems:

43/ Past successes will lull you into a false sense of ability. The only antidote is self-reflection and post-mortems on your own past successes.

theverge.com/2020/1/8/21056…

theverge.com/2020/1/8/21056…

44/ Marriage in a nutshell:

Ben Franklin: "Eyes wide open before marriage and half shut afterwards."

Munger: "See it as it is and love it anyways."

Thomas S. Monson: "Choose your love and love your choice."

Ben Franklin: "Eyes wide open before marriage and half shut afterwards."

Munger: "See it as it is and love it anyways."

Thomas S. Monson: "Choose your love and love your choice."

• • •

Missing some Tweet in this thread? You can try to

force a refresh