Talk by Hunt Alcott: Are High-Interest Loans Predatory? Theory and Evidence from Payday Lending

Paper: dropbox.com/s/ibavoq0pvr8p…

Slides: dropbox.com/s/007niykbznui…

Paper: dropbox.com/s/ibavoq0pvr8p…

Slides: dropbox.com/s/007niykbznui…

Evaluating consumer protection policies

Many policies motivated by concerns that consumers don’t act in their own best interest or are “exploited” by firms

Must develop tools for:

• Measurement of alleged mistakes

• Behavioral welfare evaluation of proposed policies

Many policies motivated by concerns that consumers don’t act in their own best interest or are “exploited” by firms

Must develop tools for:

• Measurement of alleged mistakes

• Behavioral welfare evaluation of proposed policies

Should we restrict high-interest lending?

Are borrowers acting in their own best interest?

Two basic questions:

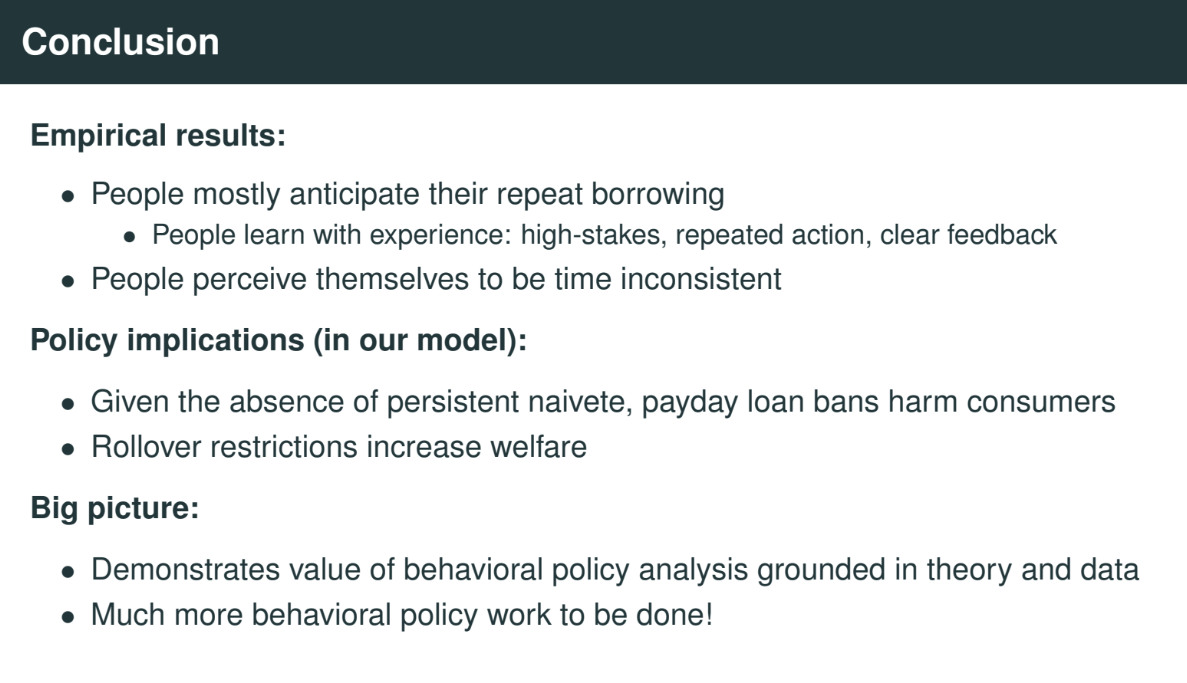

• Do people anticipate repeat borrowing?

• Do borrowers perceive themselves to be time consistent?

Are borrowers acting in their own best interest?

Two basic questions:

• Do people anticipate repeat borrowing?

• Do borrowers perceive themselves to be time consistent?

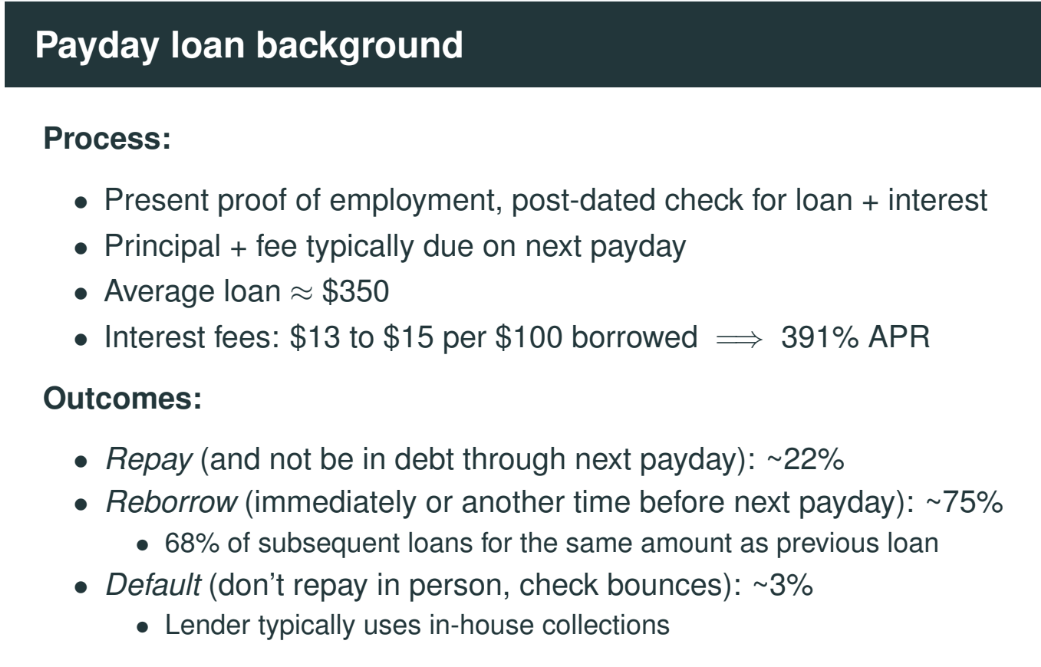

Payday loan background

Average loan $350, 391% APR

22% repay, 75% reborrow (roll over), 3% default

Average loan $350, 391% APR

22% repay, 75% reborrow (roll over), 3% default

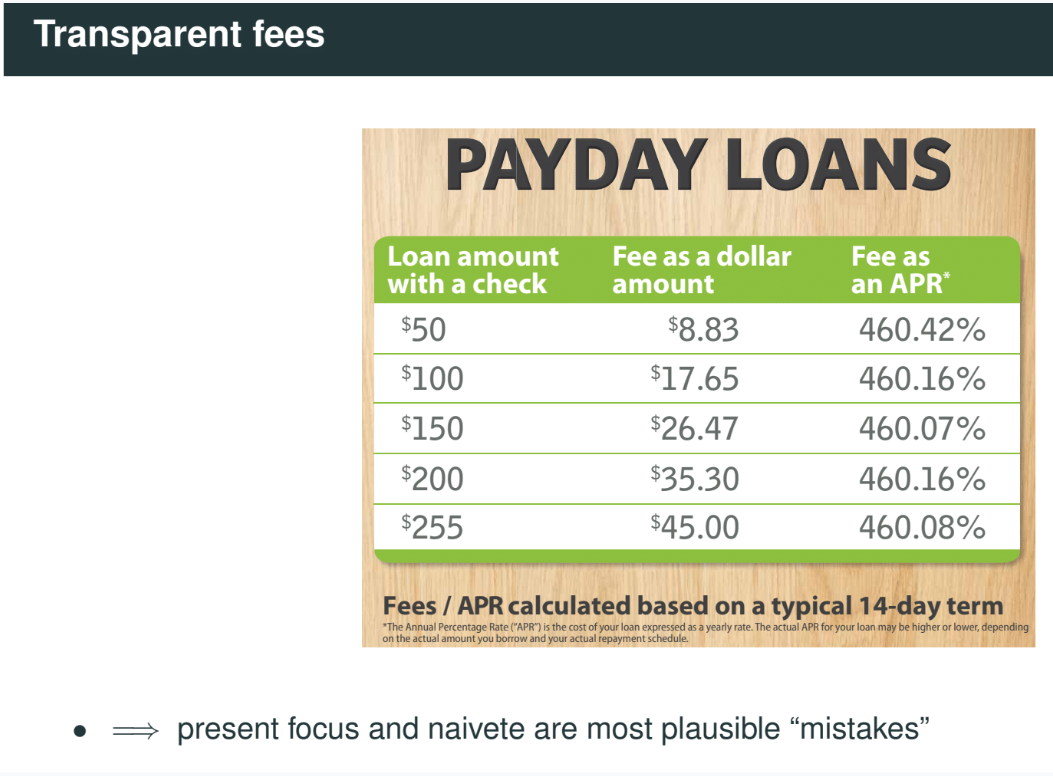

Fees are really transparent, no shrouded attributes

present focus and naivete are most plausible “mistakes”

present focus and naivete are most plausible “mistakes”

Key survey questions

1. Do people anticipate repeat borrowing?

2. Do people want an incentive to avoid avoid future borrowing? (⇒ perceived time inconsistency)

3. How risk averse are people?

1. Do people anticipate repeat borrowing?

2. Do people want an incentive to avoid avoid future borrowing? (⇒ perceived time inconsistency)

3. How risk averse are people?

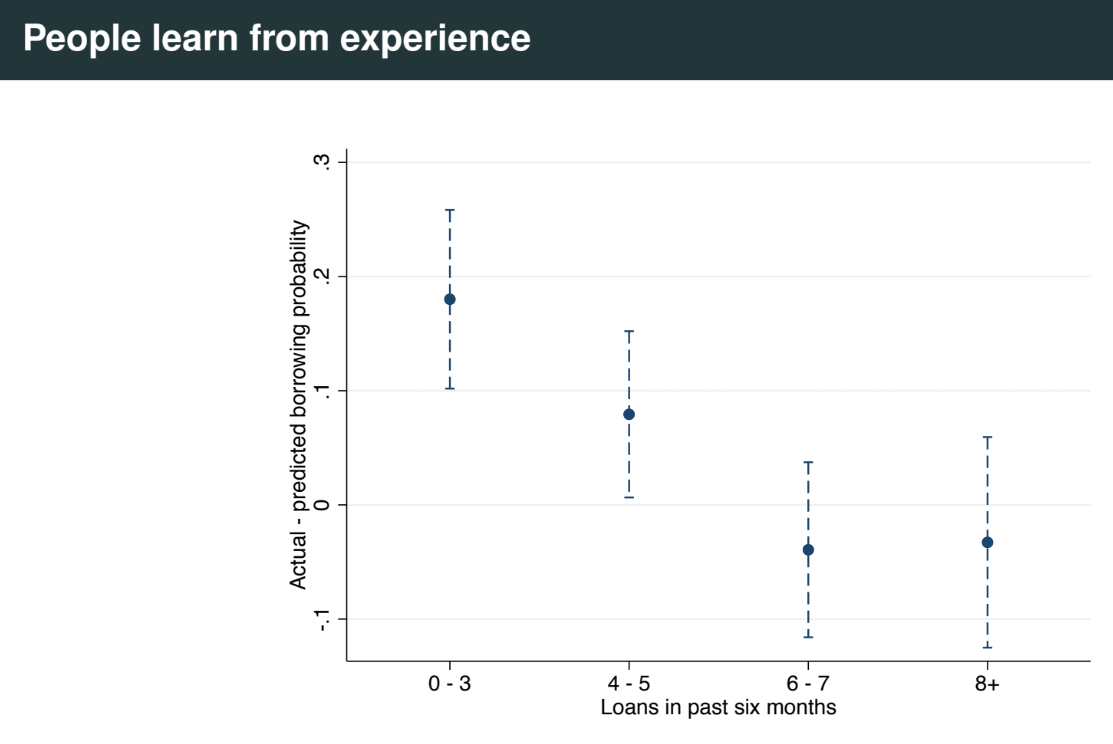

Do people anticipate repeat borrowing?

People borrow slightly more than expected (74% real vs 70% expected)

People learn from experience;

Most inexperienced quartile (0-3 loans in past 6 months) underestimate p(reborrow) the most

People borrow slightly more than expected (74% real vs 70% expected)

People learn from experience;

Most inexperienced quartile (0-3 loans in past 6 months) underestimate p(reborrow) the most

"This is an example of a situation where you have an opportunity to learn. Where it's high stakes and you have repeated easily observable feedback about your behavior and so this is exactly the sort of scenario where you would expect people to learn about their behavior "

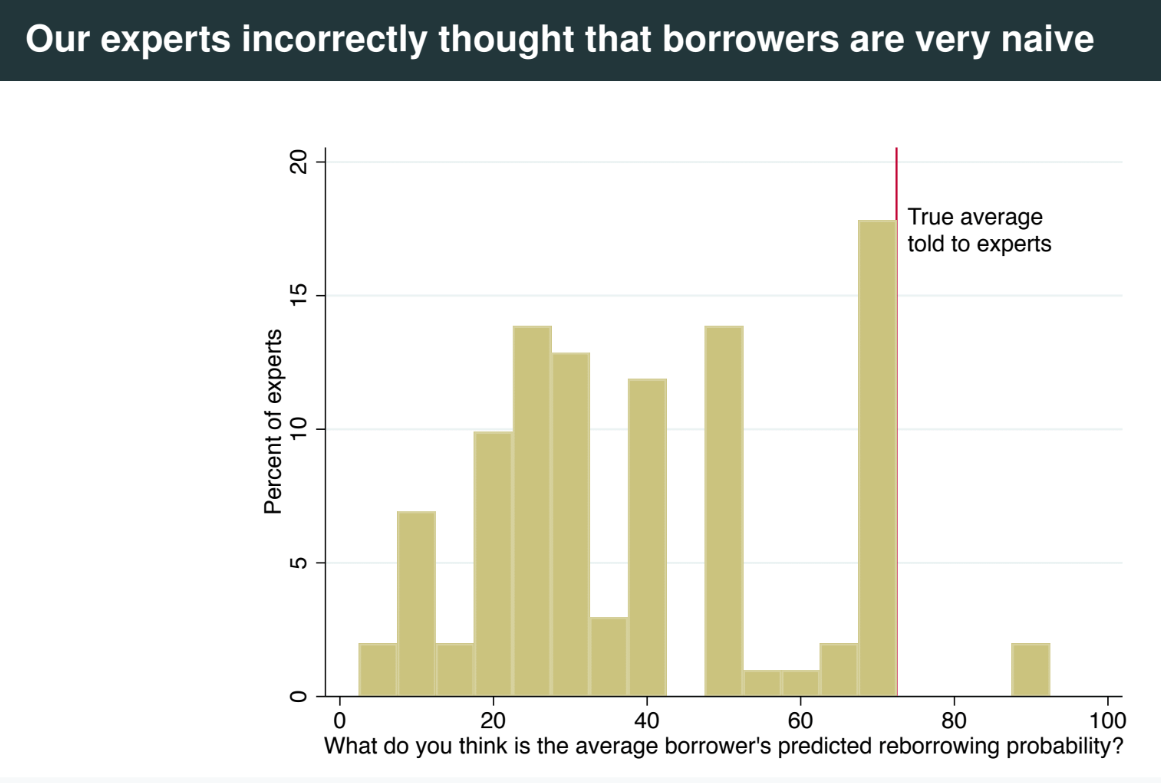

[not in talk, but in slide deck] The N=103 payday lending and behavioral economics experts, incorrectly thought that borrowers are very naive

(most inexperienced quartile of borrowers [#pt] with worst prediction, was off by 18%-pnts, would be 52% in this figure)

(most inexperienced quartile of borrowers [#pt] with worst prediction, was off by 18%-pnts, would be 52% in this figure)

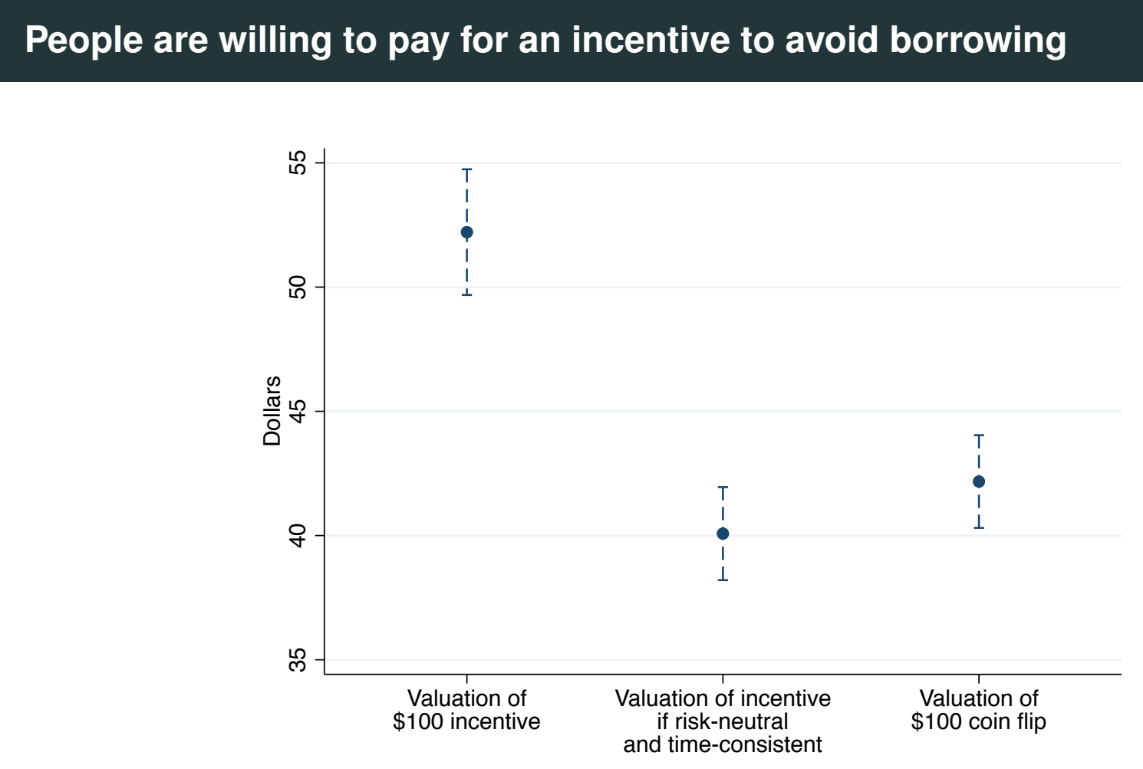

People are willing to pay for an incentive to avoid borrowing

People value $100 incentive at $52

Valuation if you were risk neutral and time consistent: $40. So a $12 (30%) difference on average

(explanation at 32:22 )

People value $100 incentive at $52

Valuation if you were risk neutral and time consistent: $40. So a $12 (30%) difference on average

(explanation at 32:22 )

Simpler, qualitative questions corroborate that;

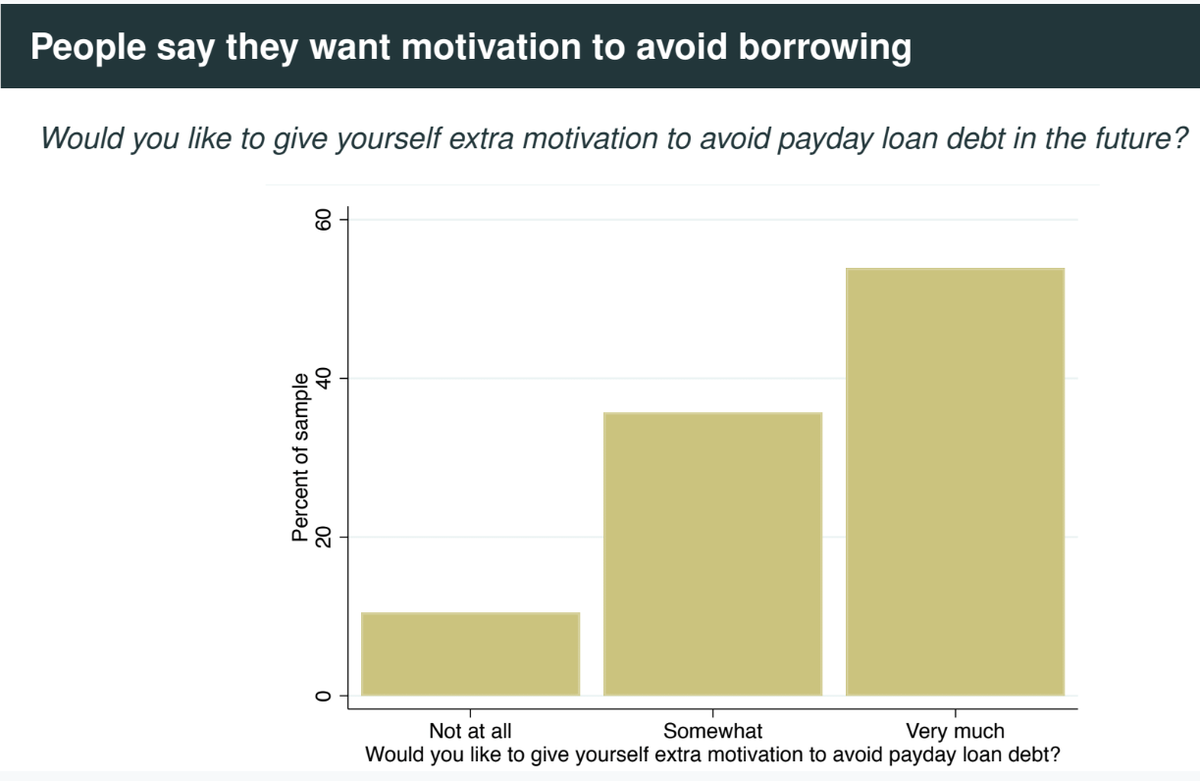

People say they want motivation to avoid borrowing

People say they want motivation to avoid borrowing

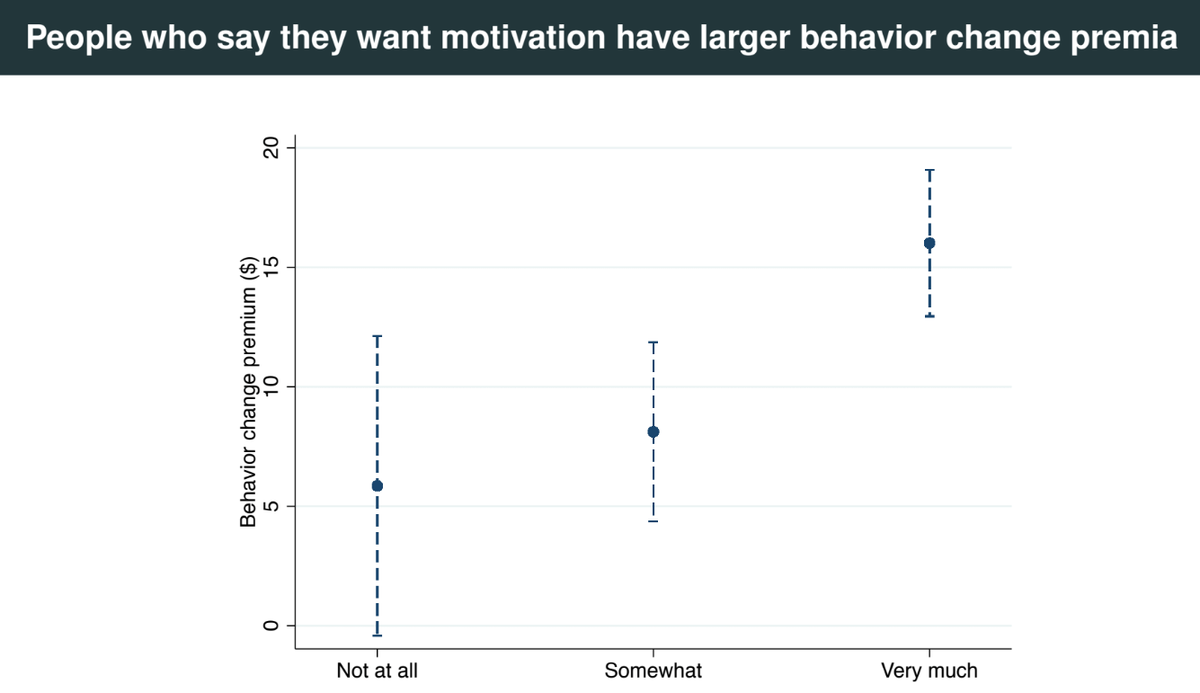

[not in talk] People who want legal restrictions have larger behavior change premia

(The behavior change premium on average was $12 see #pt)

(~37% don't want legal rollover restrictions, 35% neutral, 30% do want legal restrictions)

(The behavior change premium on average was $12 see #pt)

(~37% don't want legal rollover restrictions, 35% neutral, 30% do want legal restrictions)

I'm afraid I'm to economically naive to understand the Partially Naive Present Focus Model & how to identify and estimate naivete (β/β-tilde)

β <1: Present focus

Perceived present focus β-tilde

α = CARA (constant absolute risk aversion)

β <1: Present focus

Perceived present focus β-tilde

α = CARA (constant absolute risk aversion)

Policy Evaluation

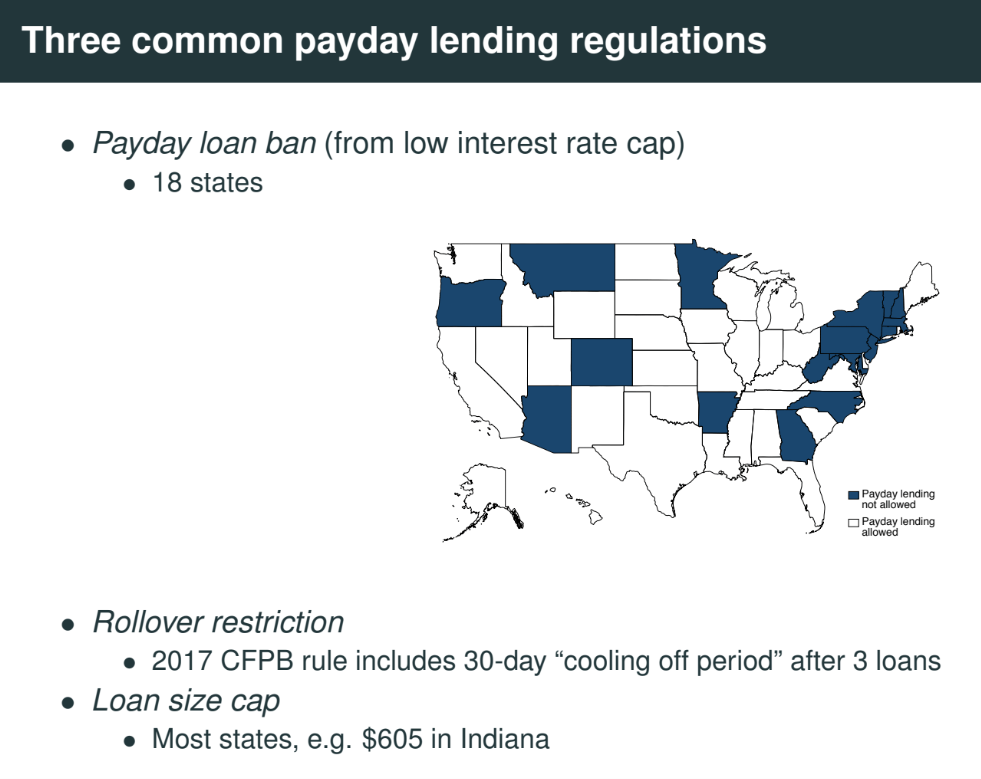

Three common payday lending regulations

1⃣ Payday loan ban (from low interest rate cap) (also in Netherlands, cap =14% APR; afm.nl/nl-nl/professi…)

2⃣ Rollover restriction

3⃣ Loan size cap

Three common payday lending regulations

1⃣ Payday loan ban (from low interest rate cap) (also in Netherlands, cap =14% APR; afm.nl/nl-nl/professi…)

2⃣ Rollover restriction

3⃣ Loan size cap

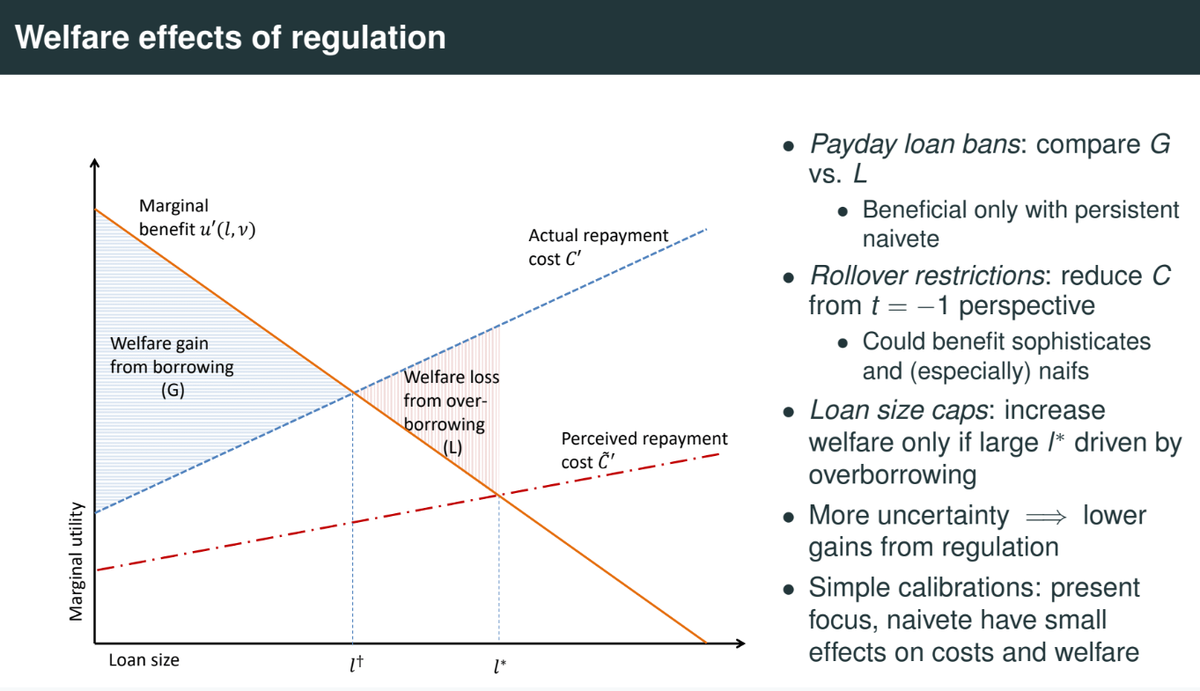

Welfare effects of regulation

"One way to think about banning payday lending is to think about whether the welfare gain from borrowing (blue triangle G) is larger than the welfare loss from over-borrowing (red triangle L)"

"One way to think about banning payday lending is to think about whether the welfare gain from borrowing (blue triangle G) is larger than the welfare loss from over-borrowing (red triangle L)"

51:26: "imposing a higher fee on borrowing is another way to think about what a ban on payday lending would do.

Instead of eliminating all high cost borrowing it just forces people to go to an even higher interest rate source of high cost borrowing"

Instead of eliminating all high cost borrowing it just forces people to go to an even higher interest rate source of high cost borrowing"

Numerical simulations, calibrated with empirical data

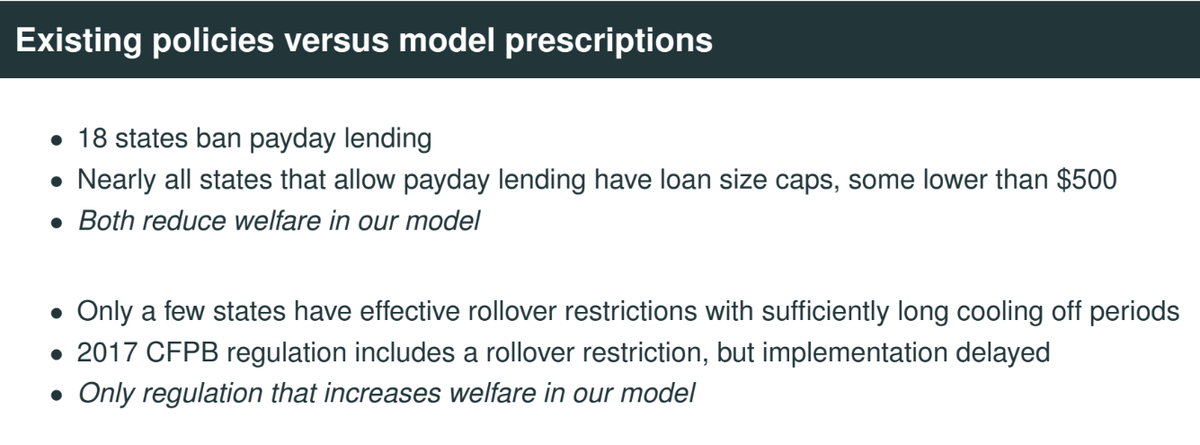

Payday ban and loan size caps REDUCE welfare in the model

Rollover restrictions do increase welfare (encourage faster pay back)

Payday ban and loan size caps REDUCE welfare in the model

Rollover restrictions do increase welfare (encourage faster pay back)

Conclusion

At 57:22 (Q&A) two possible outcomes of ban on payday lending are modeled: (1) there is no high cost borrowing anymore (2) shift to other forms of high(er) cost borrowing