1. New #fdd last week on forecast performance of simple crop weather models in forecasting US average corn yield. Interesting exercise farmdocdaily.illinois.edu/2020/07/the-ac…

2. Compared 2 models for May-Aug early season yield forecasts of corn: i) WAOB/USDA model, and ii) a similar model that TH and I developed. We reviewed the WAOB model is this article a week ago: farmdocdaily.illinois.edu/2020/07/unders…

3. Both models include trend, planting progress/late planting, June precip, July precip, and July temps. Some differences in data definitions and variables. Biggest is the WAOB use of a June precip shortfall measure. We use a standard quadratic.

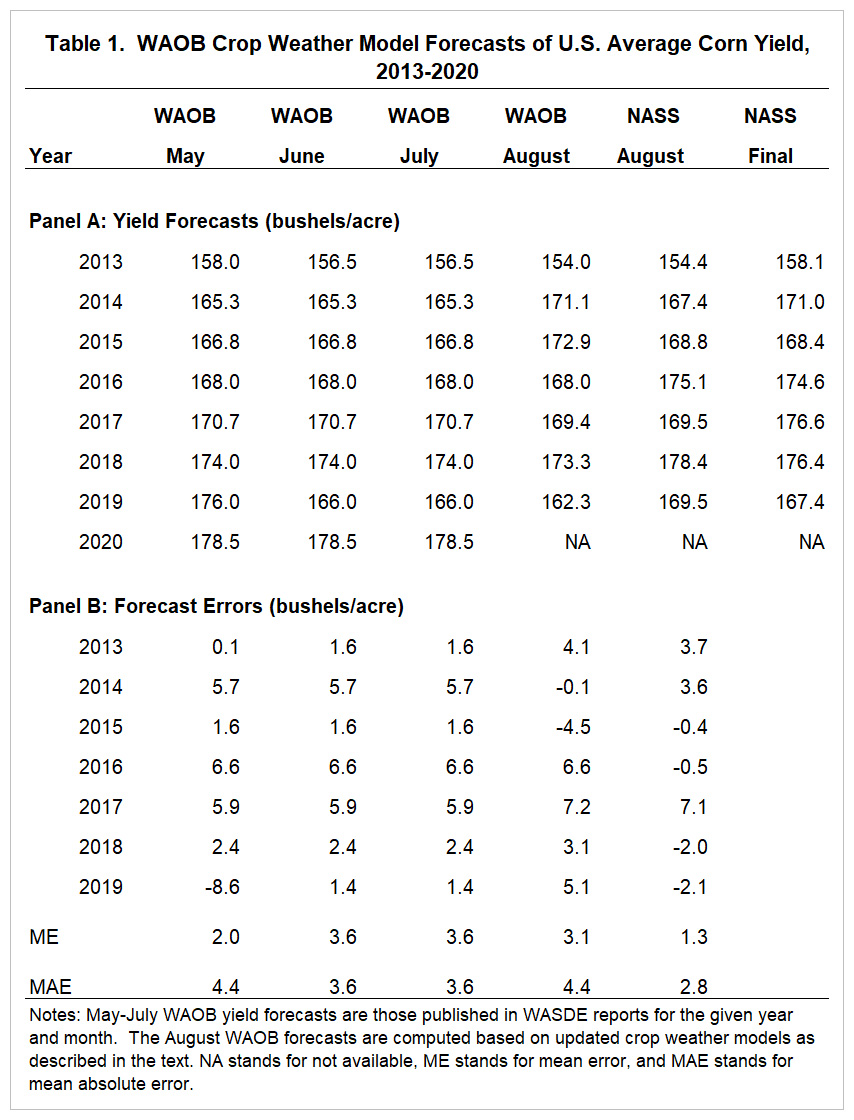

4. Here are the WAOB forecasts and forecast errors over 2013-2019. Started in 2013 because that was first year the WAOB used the model to make forecasts for the May, June, and July WASDE.

5. Most interesting thing about the WAOB crop weather model forecasts? I've been on the side that WAOB May-July corn yield forecasts in recent years have been on a shade optimistic when released. Wrong. ME (mean error) shows these "optimistic" forecasts were 2-3bpa too low.

6. Here are the parallel results for our simple crop weather model. Similar to WAOB model except for 2014. Our model made a huge forecast error that year, 20bpa too low! Ouch. Why? Our model puts more weight on July precip and it was oddly low in 2014 for a record yield.

7. Here the money chart from the article. Mean absolute errors (MAE) that show which forecasts were closest to the target (final yield). WAOB model clearly beat our modified version. And NASS August handily beats any of the models.

8. I think there is an important lesson here regarding NASS survey-based yield estimates in Aug-Nov. Lots of chatter that these are obsolete with the rise of "big data" private competitors. USDA/NASS not nearly as easy to beat as many think. Take that to the bank.

• • •

Missing some Tweet in this thread? You can try to

force a refresh