Okay, this is better than my tweet.

Rare to see this kind of Conor bait in print:

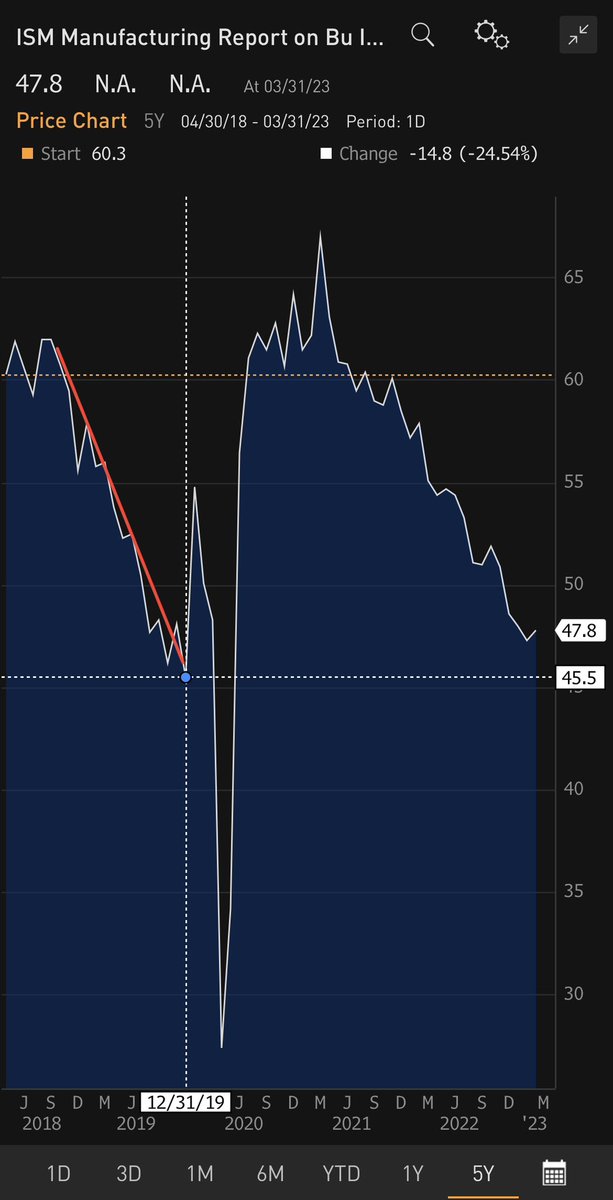

This is the closest thing to what I had in mind:

• • •

Missing some Tweet in this thread? You can try to

force a refresh