1/ As promised yesterday, here's the final part of the thread on @mjmauboussin's recent report on "Public to Private Equity in the United States: A Long-Term Look".

Here's part 1 of the thread if you haven't read that yet (not necessary though):

Here's part 1 of the thread if you haven't read that yet (not necessary though):

2/ Public Equities

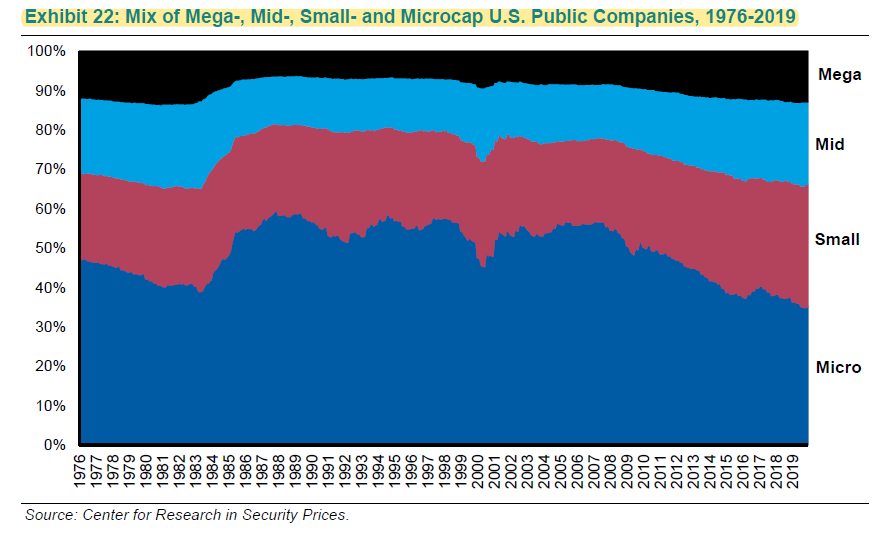

In the 90s, 15-20% small cap cos became medium/large cos every year. Today, it's half of that.

Median ROA gap between large and small cos was 15% in the 90s while today it has become 30-35%!

In the 90s, 15-20% small cap cos became medium/large cos every year. Today, it's half of that.

Median ROA gap between large and small cos was 15% in the 90s while today it has become 30-35%!

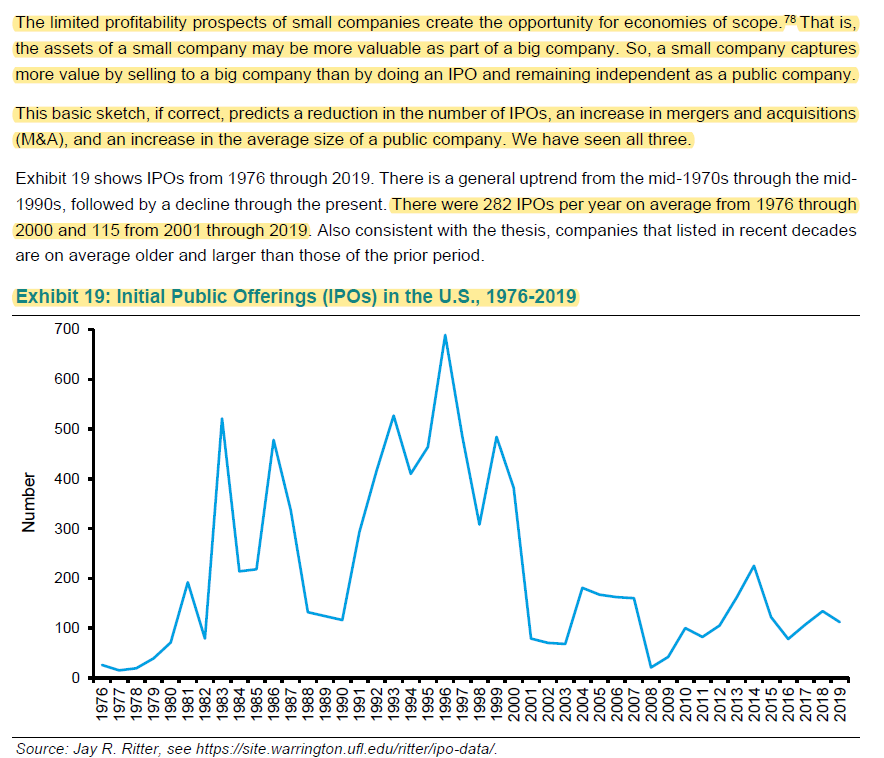

3/ Limited profitability prospects for small cos make them more valuable as part of a larger company i.e. more M&A, less IPO, and larger size of remaining companies.

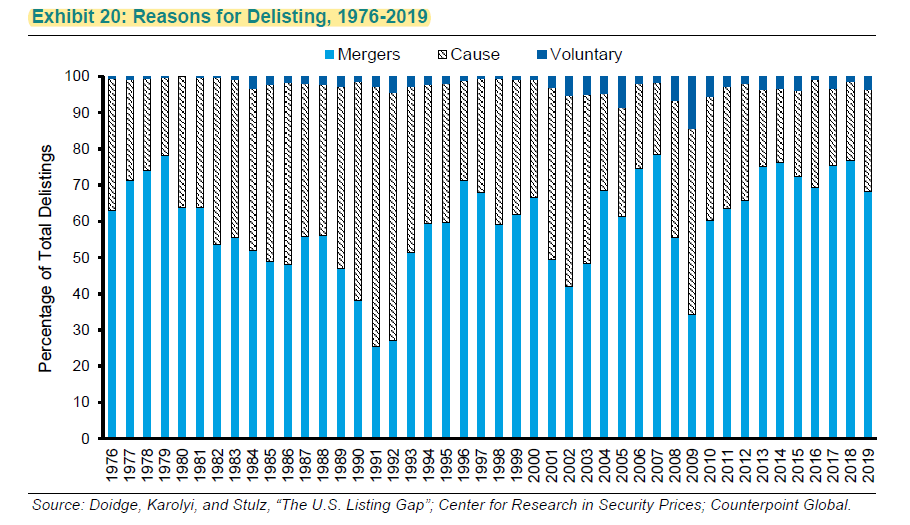

4/ "While there has been a decline in each size category, more than 90 percent of the stocks that have disappeared since 1996 were those of small- and micro-capitalization companies"

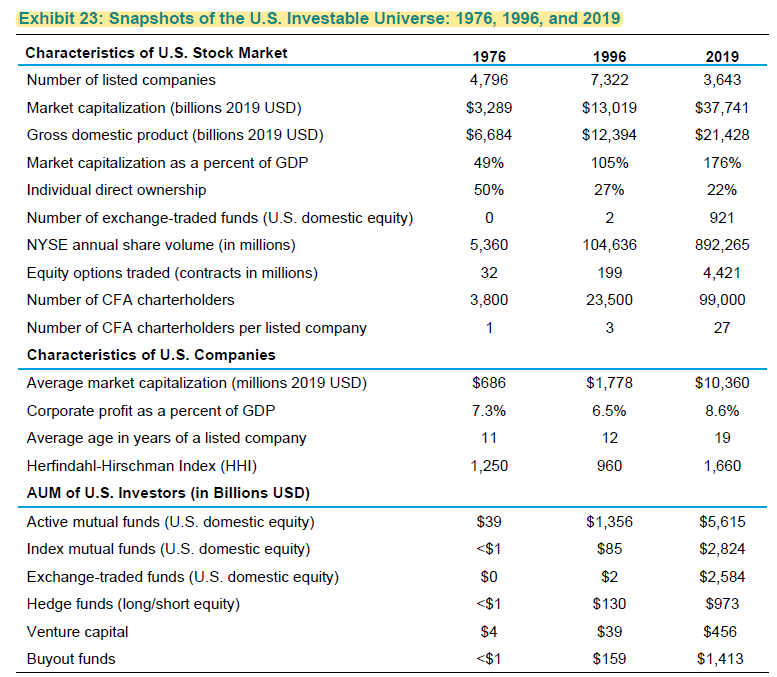

5/ Take the next minute to glance through this table. Lots of interesting inferences not suitable for a tweet.

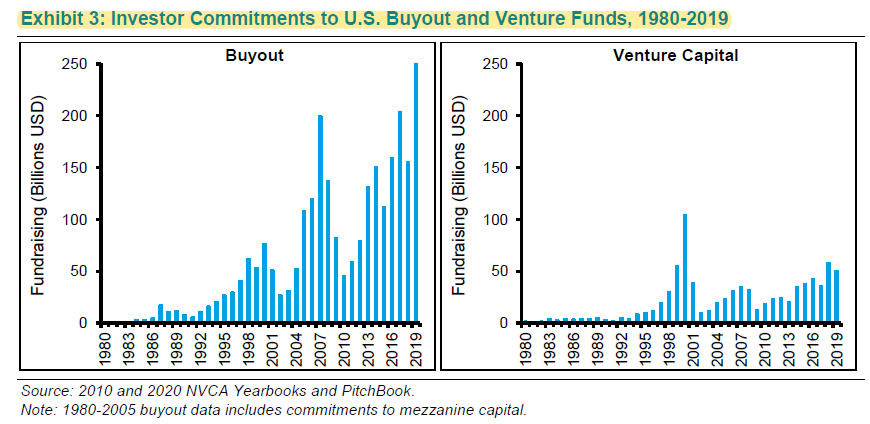

6/ Buyouts

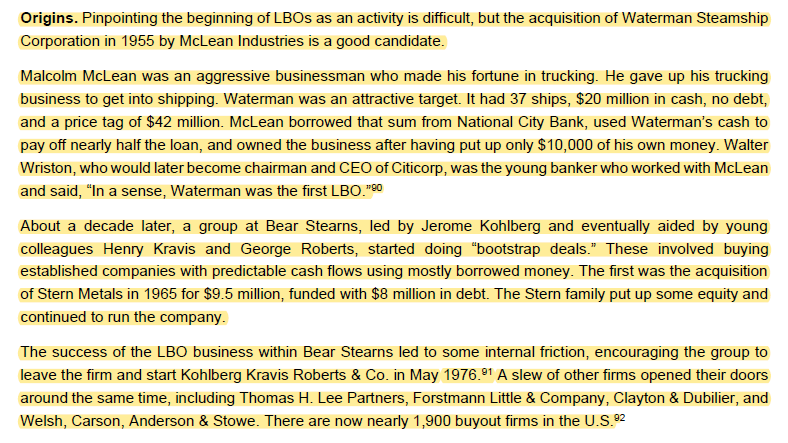

Interesting origin of LBO which started with a tidy $10,000 equity 65 years ago. From those humble origin buyouts have come a long as today there are ~1900 buyout firms in the US.

Interesting origin of LBO which started with a tidy $10,000 equity 65 years ago. From those humble origin buyouts have come a long as today there are ~1900 buyout firms in the US.

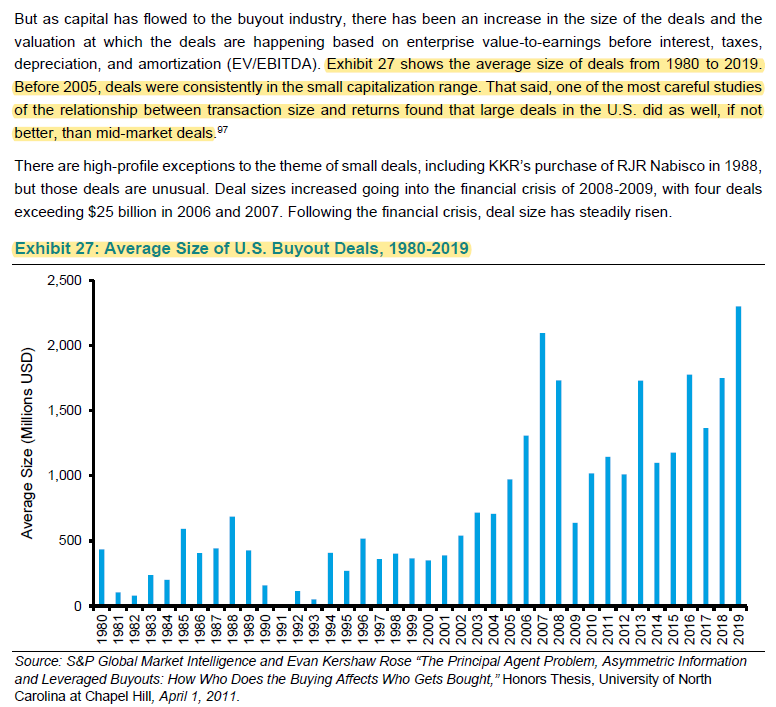

7/ Large deals did as well, if not better, than mid-market deals.

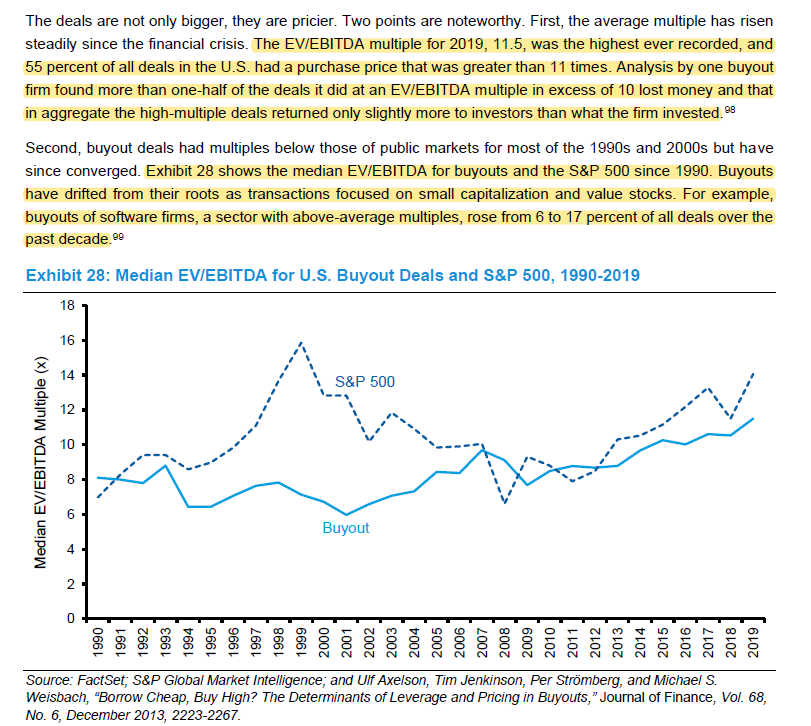

8/ Current EV/EBITDA multiple for deals: 11.5x. Word of caution: ~50% deals above 10x multiple lost money.

Besides interest rates, one driver of high multiples is greater proportion of software buyouts which are typically more expensive.

Besides interest rates, one driver of high multiples is greater proportion of software buyouts which are typically more expensive.

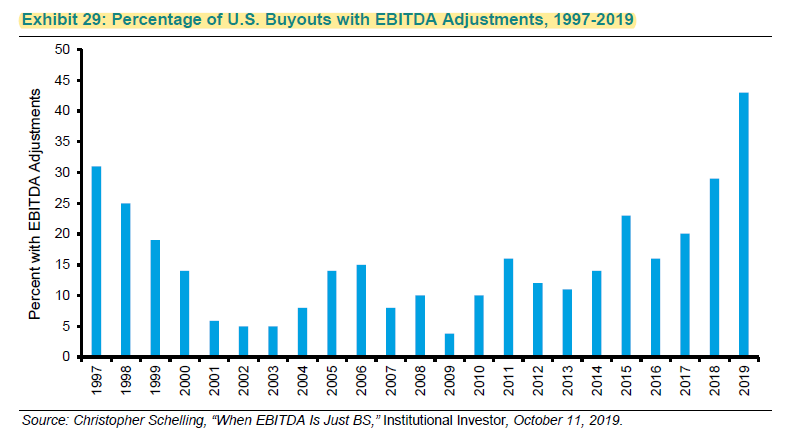

9/ ~40% deals now mention "adjusted EBITDA" rather than just EBITDA, the highest on record. Companies that forecast "adjusted EBITDA" miss those projections by an avg of 35% two years following the deal.

I guess we all should fear the word "adjusted".

I guess we all should fear the word "adjusted".

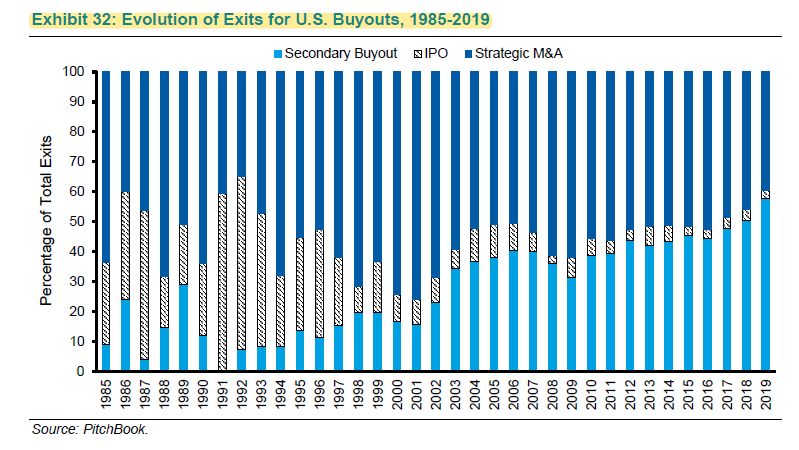

10/ For buyout firms, avg holding period was 7 yrs in '70s and '80s, then fell to 4 yrs in '08, and gradually rose to 5.5 yrs in 2019.

Most exits happen through a sale to a secondary buyout typically at a higher multiple.

Most exits happen through a sale to a secondary buyout typically at a higher multiple.

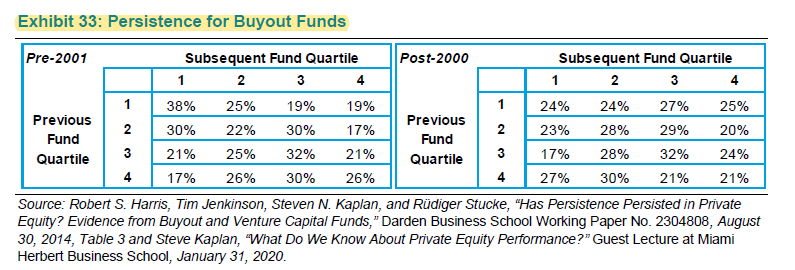

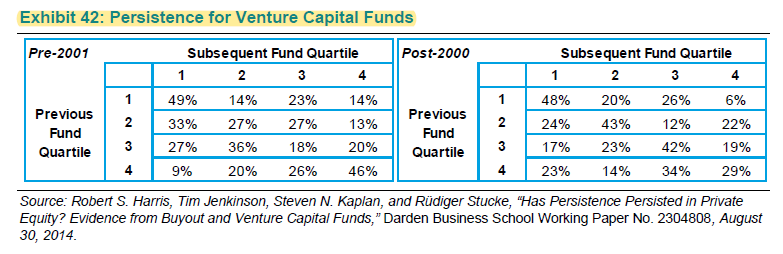

11/ Look at these tables closely. Pre and post-2000 depicts such a stark contrast when it comes to persistence of return. Post-2000 looks just random.

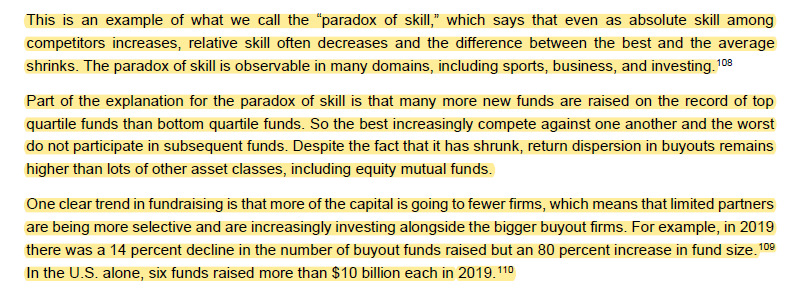

12/ Why is this happening? Paradox of skill.

I used the same idea to explain that "paradox of skill" is very much present in Cricket. If you follow the sport, you can read this thread.

I used the same idea to explain that "paradox of skill" is very much present in Cricket. If you follow the sport, you can read this thread.

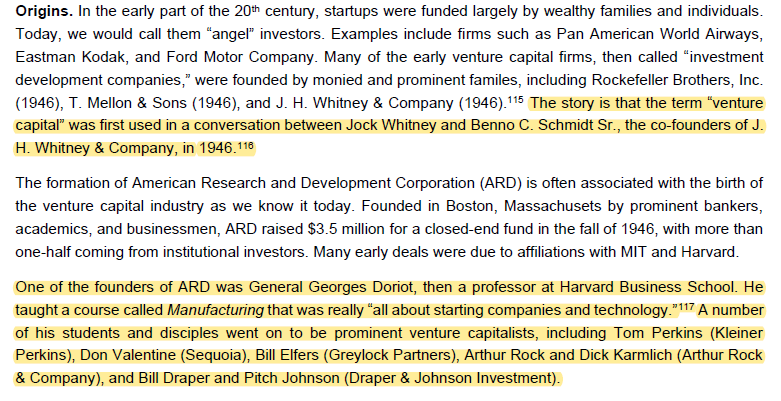

13/ Venture Capital

I had no idea a HBS Professor, who taught a course called "Manufacturing", influenced the likes of Tom Perkins and Don Valentine.

I had no idea a HBS Professor, who taught a course called "Manufacturing", influenced the likes of Tom Perkins and Don Valentine.

14/ Incredible factoids

# of IPO in 1969 = ~20% of total public companies today

~50% US VC AUM is in the Bay Area, 75% after including NYC and Boston i.e. VC AUM is very, very geographically concentrated. Total US VC AUM is $455 Bn with $120 Bn dry powder.

# of IPO in 1969 = ~20% of total public companies today

~50% US VC AUM is in the Bay Area, 75% after including NYC and Boston i.e. VC AUM is very, very geographically concentrated. Total US VC AUM is $455 Bn with $120 Bn dry powder.

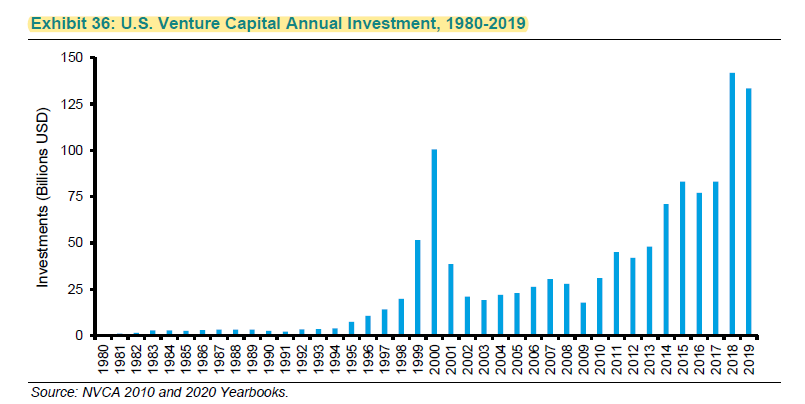

15/ It took 18 years to surpass dot com level VC investments.

Buyout firms can scale their AUM more easily than VC firms although their fees are comparable i.e. 2-20 structure.

Buyout firms can scale their AUM more easily than VC firms although their fees are comparable i.e. 2-20 structure.

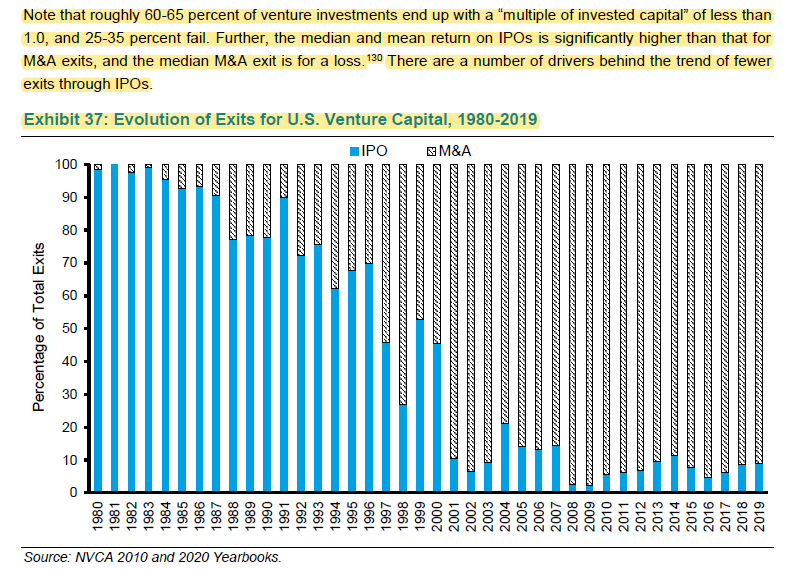

16/ Super-majority of VC exits happen via M&A and the median M&A exit for a loss.

While IPOs are limited in number, the avg return is much higher than M&A exits.

While IPOs are limited in number, the avg return is much higher than M&A exits.

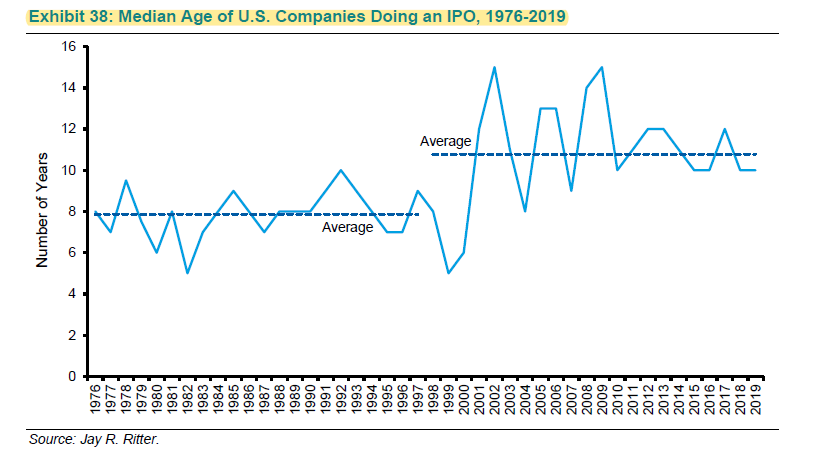

17/ Companies stay private for far longer than they used to. Median age of firm before IPO increased 50% from 1976-2000 to 2001-2019.

18/ There are 225 unicorns in the US worth $662 Bn in aggregate.

But these valuations are often exaggerated. In some estimates, unicorn valuations are on avg ~50% above the fair value.

But these valuations are often exaggerated. In some estimates, unicorn valuations are on avg ~50% above the fair value.

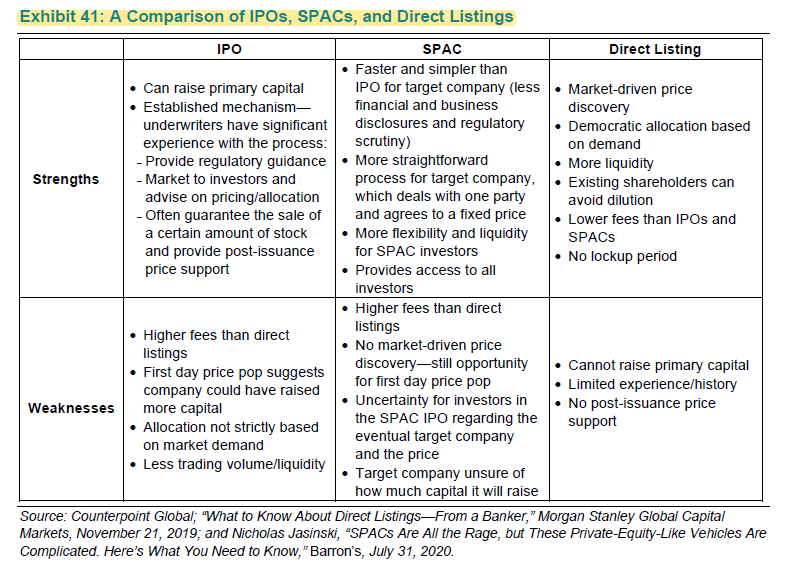

19/ Strengths and weaknesses of IPO, SPAC, Direct Listing

20/ Unlike buyout firms, VCs exhibit robust persistence. Some argue successful VCs enjoy preferential access because of their past success/reputation which helps their return persist.

21/ The dispersion of returns in VCs also makes it clear if anyone justifies the fees in the whole investment management industry, it's the top quartile VCs.

22/ Where from here?

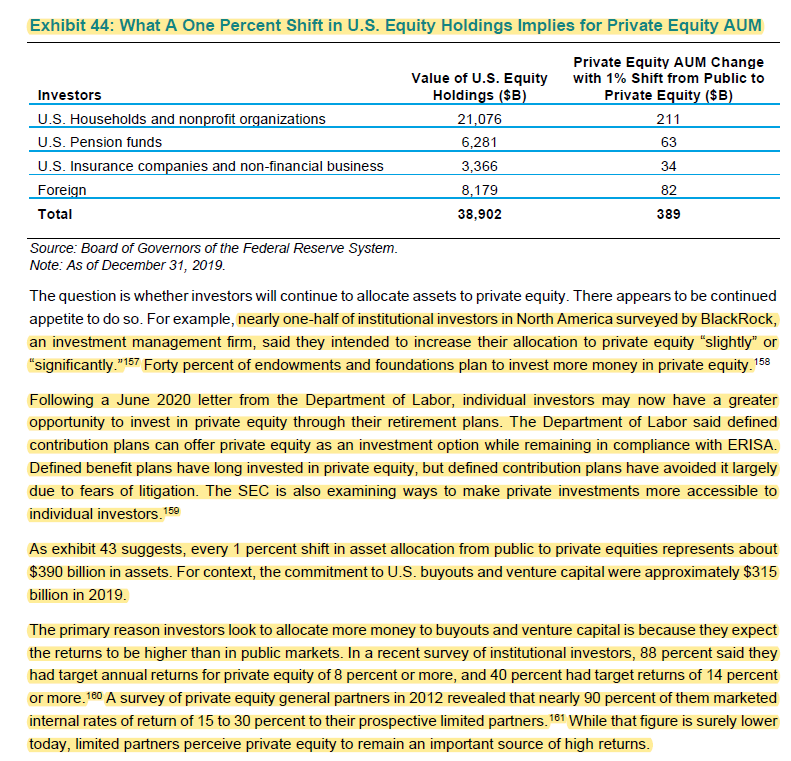

Regulatory tailwinds can ensure PEs can enjoy the good times to persist although high valuations remain a concern.

Regulatory tailwinds can ensure PEs can enjoy the good times to persist although high valuations remain a concern.

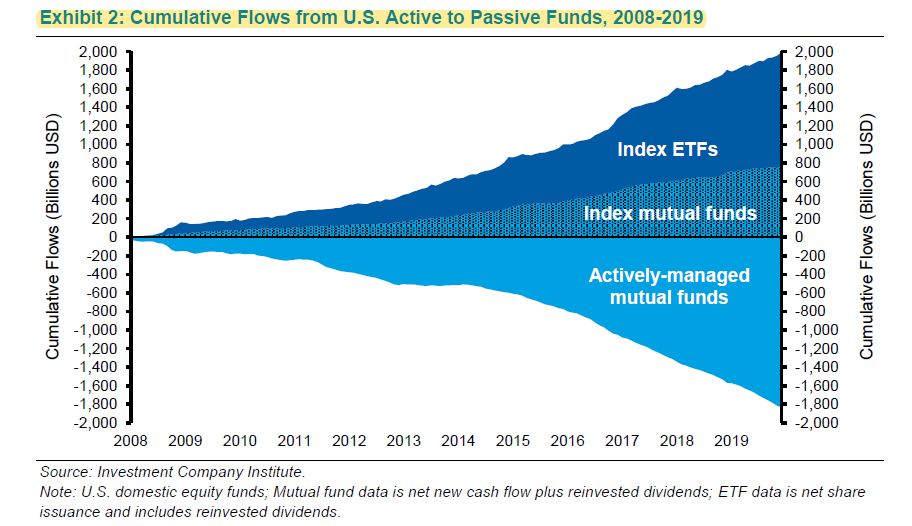

23/ Also, more competition for the fees is coming with a very familiar face in the charge again: Vanguard.

If those persistence numbers remain random as it did for last 20 years, PE firms have very little right to enjoy 2-20 fees.

If those persistence numbers remain random as it did for last 20 years, PE firms have very little right to enjoy 2-20 fees.

End/ Finally, just wanted to thank @mjmauboussin and Dan Callahan for writing this fascinating piece and making it available for everyone. Much appreciated.

Have a great weekend, everyone!

Have a great weekend, everyone!