A v interesting data sheet from Mint on how returns from different assets have behaved since 2010 - a good enough time frame in the world of rapid disruption. My notes in this thread

.. (1/n)

.. (1/n)

1. Sabka time aayega - Each asset class ends up coming to the top slot and then after that sooner or later goes right at the bottom.

2. Gold - it has a negative correlation, i.e. if Gold is in extreme bull markets, Indian markets are not doing well.

.. (2/n)

2. Gold - it has a negative correlation, i.e. if Gold is in extreme bull markets, Indian markets are not doing well.

.. (2/n)

E.g. 2010-11 Gold gave 24% & 29% and Indian markets were either flat or rutting. Same in 2019-2020.

3. Gold doesn't always glow. Three years 2013-2015 - worse asset class

3. Real estate has barely been able to touch 20%, contrary to the belief that it is a multibagger

.. (3/n)

3. Gold doesn't always glow. Three years 2013-2015 - worse asset class

3. Real estate has barely been able to touch 20%, contrary to the belief that it is a multibagger

.. (3/n)

4. It has barely touched 20% in any year.

5. After Gold, the most volatile asset class is Small & Mid Caps. But then the returns are exceptional too. When this category underperforms, it can kill an entire portfolio if one is overweight in it. See over -30% in 2011, 17.

(4/n)

5. After Gold, the most volatile asset class is Small & Mid Caps. But then the returns are exceptional too. When this category underperforms, it can kill an entire portfolio if one is overweight in it. See over -30% in 2011, 17.

(4/n)

For this category, a -10% is very usual. But when it performs, it crosses 50%+ returns. We have seen -% in this category for 3 yrs now. Would 2021 be a repeat of 2014 / 17 for this category.

6. Some where in the middle is the debt category - Corp Bond / Credit Risk..

(5/n)

6. Some where in the middle is the debt category - Corp Bond / Credit Risk..

(5/n)

But 2020 showed many investor that this category can really burn you too via defaults.

7. Amazing contrast is International investment - No correlation with Indian equities. This is much better than Gold which is negatively correlated. 2019 & 20 are recent examples.

..

(6/n)

7. Amazing contrast is International investment - No correlation with Indian equities. This is much better than Gold which is negatively correlated. 2019 & 20 are recent examples.

..

(6/n)

The negative returns here are limited, but positives won't be as blazing as Indian Small / MidCaps. But this category ends up a really good way to decouple the linkage with India. E.g. 2019 & 20 - India is negative, International is up. 2017 - India is up, so is Int

..

(7/n)

..

(7/n)

This is my personal favourite to manage the risk without having to deal with negative correlation.

8. Lastly Govt Bonds - While default risk is relatively Zero, but the price movement in this category can roll many tummy. Investor generally come here for safety.

.. (8/n)

8. Lastly Govt Bonds - While default risk is relatively Zero, but the price movement in this category can roll many tummy. Investor generally come here for safety.

.. (8/n)

Safety is reflected in price of the asset. Even though there may not be a default, but this category can very well give close to 0 returns, if not negative (see 2017). I won't be surprised if 2021 shows us one such year too.

.. (9/n)

.. (9/n)

learnings > #assetallocation is only thing which can help. One can't forecast which asset will be at top / bottom next. If you hv a good mix and rebalance your investments, one + asset category will shield the - for that year to give smooth return journey.

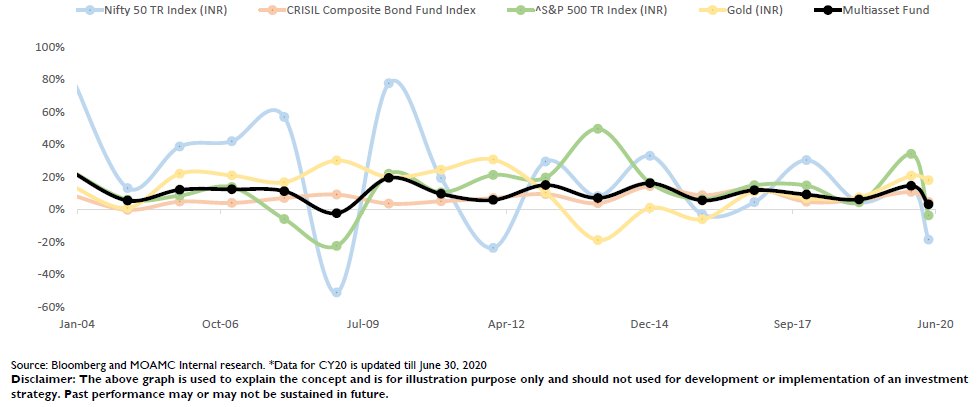

Lastly, the screenshot is obtained from a ppt of @MotilalOswalAMC See how a balanced portfolio (in Black) will tone down sharp movements of different asset classes, giving a much smoother and Positive investment journey.

• • •

Missing some Tweet in this thread? You can try to

force a refresh