When US / China's GDP increased from $2.5 to $5 trillion, their stock market growth rates were between 17% - 28% annually during this journey (from @MotilalOswalAMC).

For India, it could be a similar story. Our Compounding story is about to be on hyperdrive. Sounds fundamental.

For India, it could be a similar story. Our Compounding story is about to be on hyperdrive. Sounds fundamental.

The scale of corrections in MidCap & Small Caps is hugeeee. Midcaps still 30% lower compared to 2018 start and Small caps, still 50% lower.

When they bounce back, its to ones guess how much they will catchup to.

When they bounce back, its to ones guess how much they will catchup to.

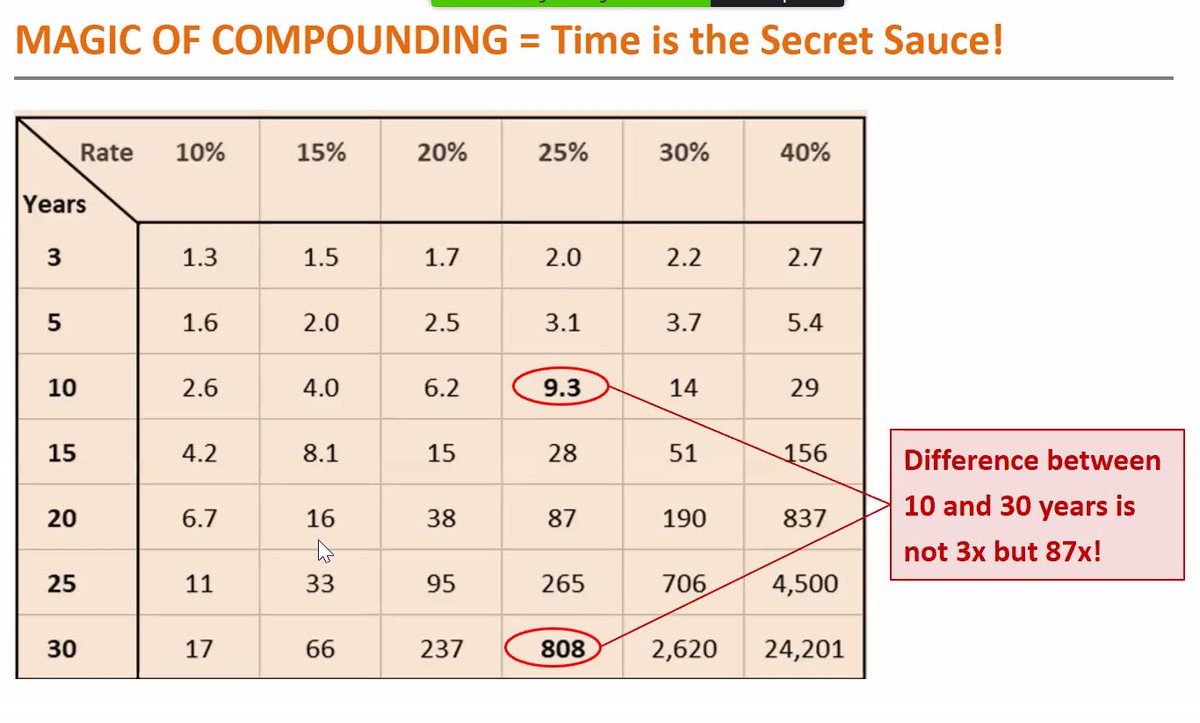

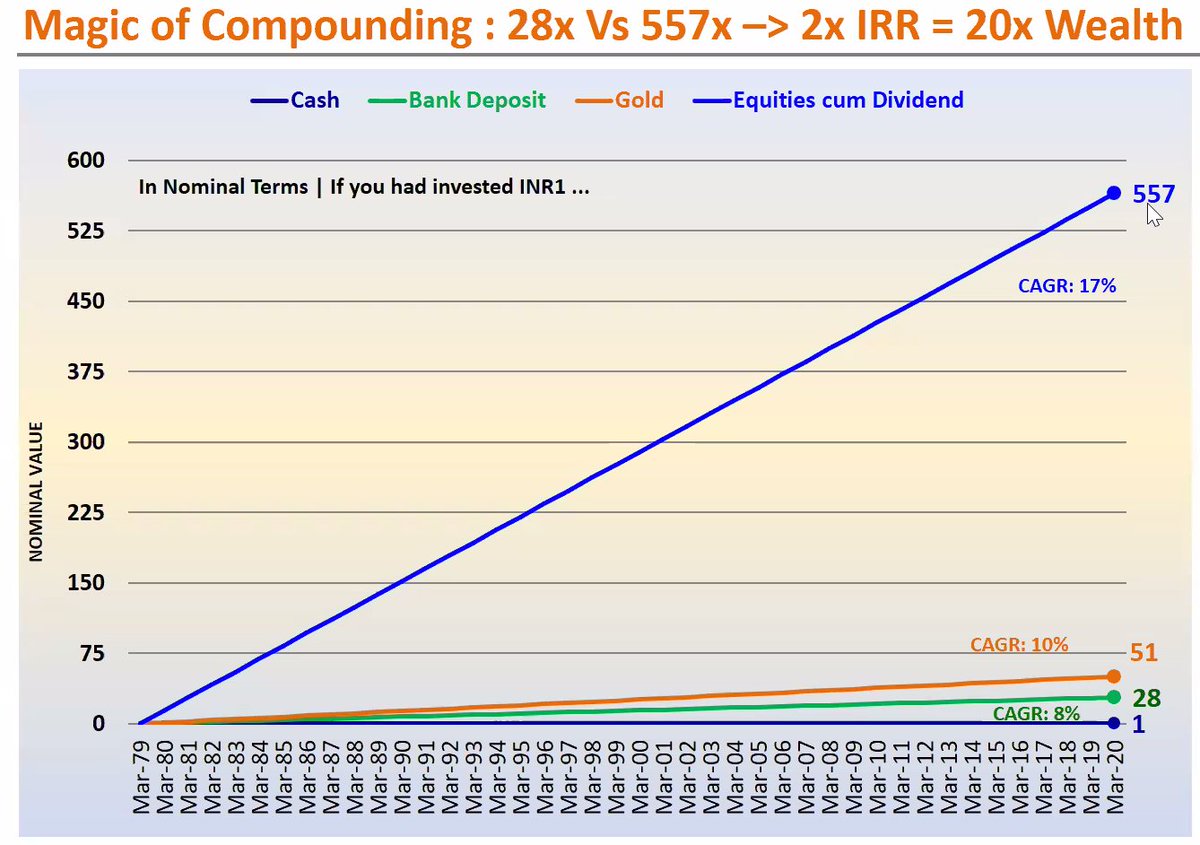

Magic of Compounding and right asset class. The longer you are invested in an investment, the more you get. E.g. even at 10% growth, in 5 yrs, your money becomes 1.6 times, but in 20 years, it becomes 6.7 Times and in 30 yrs, it becomes 17 times.

@MotilalOswalAMC

@MotilalOswalAMC

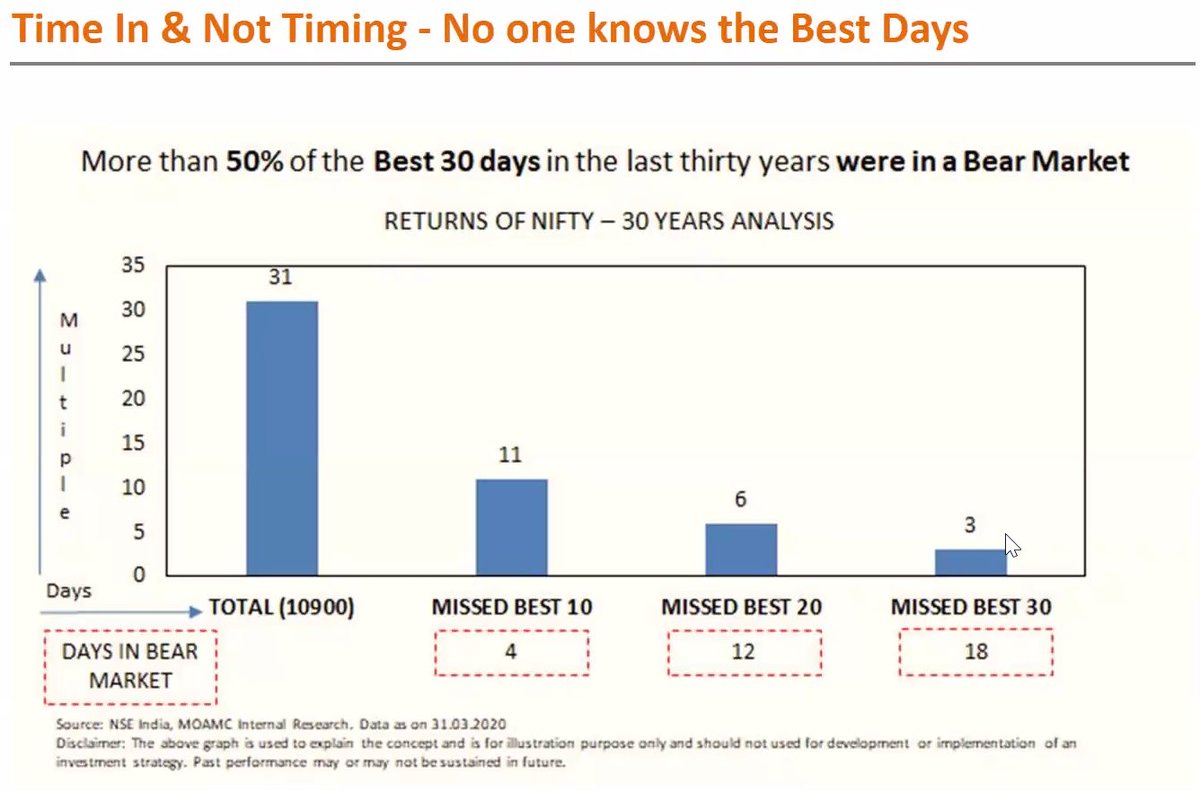

Timing the market is difficult. If you stay invested for long, you won't have to find those best 10-30 best days when most of the returns would ahve been made in last 30 yrs. If you stayed invested, the % would have been 31x. But missing out 10 best days, it would drop to 11x

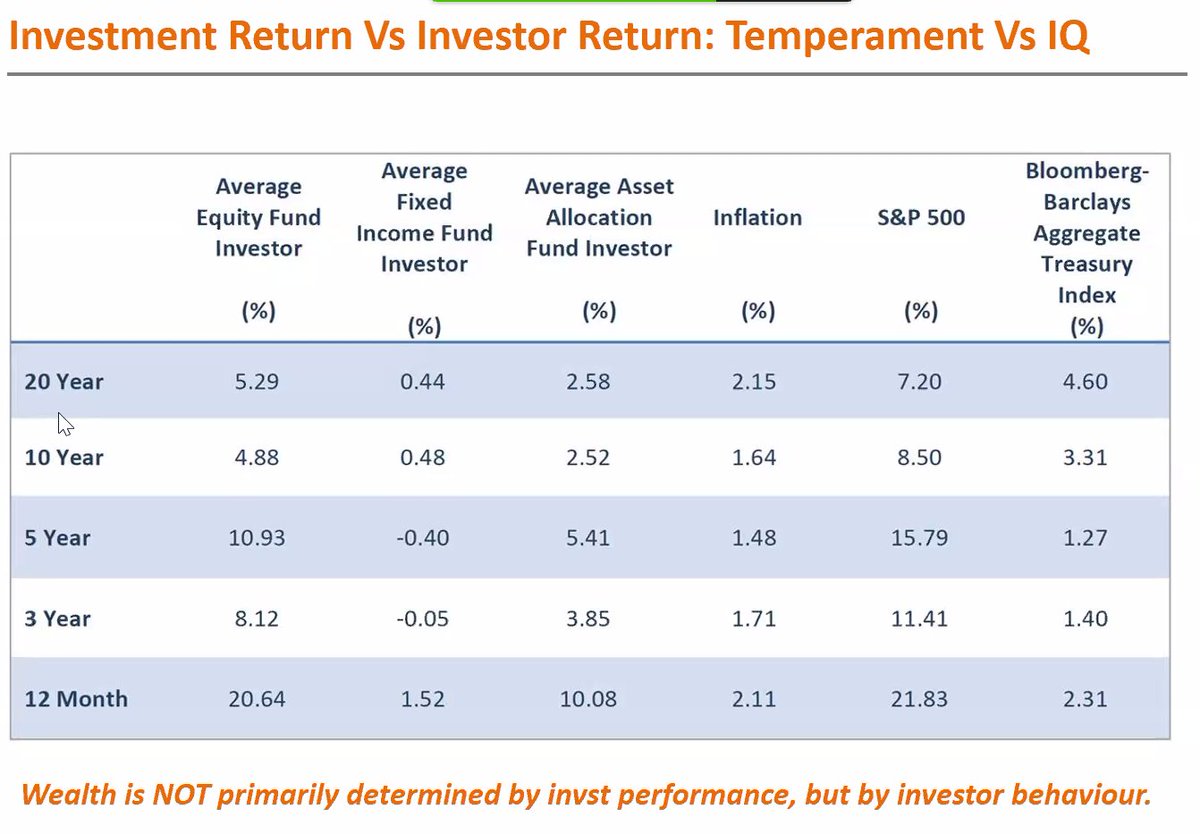

Investor returns were lesser than the underlying assets in the past by trying to time the market. E.g. In last 5 yrs, investors earned 10.93% vs S&P at 15.79%. All periods of time prove the same point. By moving in & out of the markets, investors loose best days of great returns

Too much of comparision of Equities vs other assets. Long term returns out of Equities vs Gold & FDs is clear in the chart below.

• • •

Missing some Tweet in this thread? You can try to

force a refresh