A thread about Treasury Index month-end duration extensions 1/

On the last business day of the month, usually at 3pm, bond indexes get rebalanced. Securities issued during the month that fit the index criteria get added, and ones that no longer fit (most notably, ones that mature in less than a year) come out. 2/

The effect generally is to lengthen the duration of the index. And generally, the increases are biggest at the end of the quarterly refunding months of February, May, August and November, when auction sizes are largest. 3/

With auction sizes at record levels across the curve, a duration extension of 0.15yr has been projected for Sept. 1.

That's big. Until May (when the new 20-year bond debuted), the last one of that size was in 2009. 4/

That's big. Until May (when the new 20-year bond debuted), the last one of that size was in 2009. 4/

But the impact on duration of securities *leaving* the index usually is bigger than the impact of securities joining it. And because auction sizes have grown so much in recent years, the departures impact is poised to get larger still. 5/

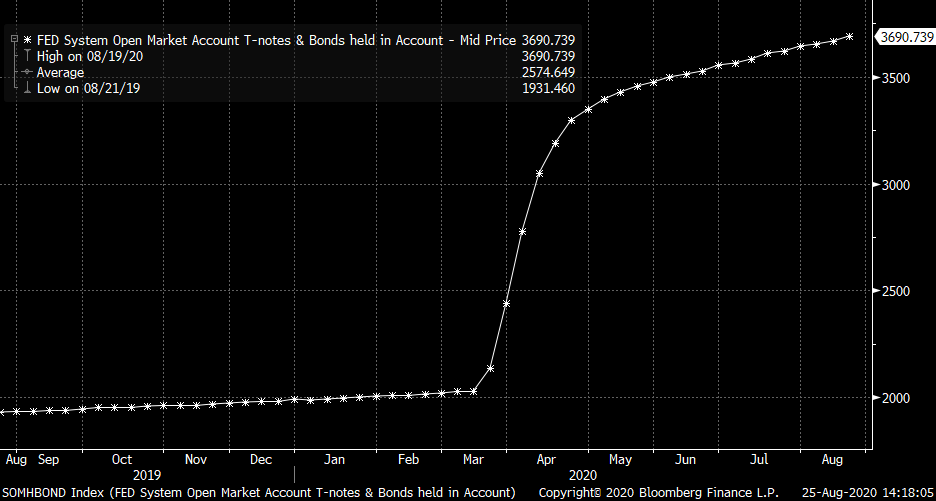

Index duration changes also reflect Fed purchases (SOMA holdings are excluded from the index) and reinvestment of coupon payments made during the month. Those things don't make a big difference tho, except in months like March and April this year, when SOMA ballooned. 6/

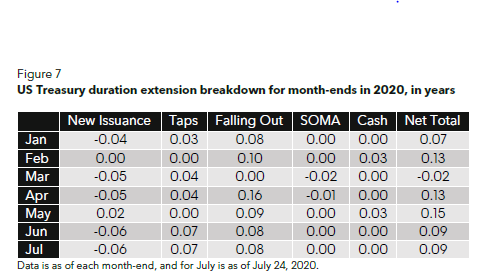

This table shows the composition of recent month-end duration changes to the index. 7/

For Sept. 1, the 0.15yr projected extension is made up of 0.02yr from new issues, 0.11yr from issues dropping out, and 0.02yr from coupon payments (with rounding error). 8/

The 0.11yr isn't the biggest this year only because in March, that part of the rebalancing was delayed. The purpose was to keep index funds in the corporate bond market, where liquidity was lousy, from having to sell securities, but it affected Treasuries too. 9/

In April, two months' worth of securities left the index, which added 0.16yr of duration in the rebalancing. 10/

These are the securities leaving the index this month, by CUSIP:

912810EK $9.5b (1991 30Y)

912828RC $66.7b (2011 10Y)

912828D7 $29b (2014 7Y)

9128282F $36.3b (2016 5Y)

9128284W $38.6b (2018 3Y)

912828YC $45.2b (2019 2Y)

912810EK $9.5b (1991 30Y)

912828RC $66.7b (2011 10Y)

912828D7 $29b (2014 7Y)

9128282F $36.3b (2016 5Y)

9128284W $38.6b (2018 3Y)

912828YC $45.2b (2019 2Y)

The point is: Treasury Index duration extensions are likely to skew bigger, not just because of bigger auction sizes for the longest-maturity instruments, but also because the amounts leaving the index are getting bigger. /END