1/ Your startup valuation, explained simply 👇

2/ Angels and Investors will buy newly issued shares (US: stock) in your company.

They will invest a dollar amount (say $1M) and buy shares at a certain Price Per Share (PPS) which is the value of one unit of equity (a share).

So far so trivial :-)

They will invest a dollar amount (say $1M) and buy shares at a certain Price Per Share (PPS) which is the value of one unit of equity (a share).

So far so trivial :-)

3/ Investors look at your existing business, assign a value to it. This the Pre-Money Valuation.

Post Money = Pre-Money + New Cash coming in

= the agreed value of your company + the cash that sits in your bank account immediately after the round.

Post Money = Pre-Money + New Cash coming in

= the agreed value of your company + the cash that sits in your bank account immediately after the round.

4/ To calculate the Price Per Share, take all the shares that exist prior to the round and divide by the number of shares in existence (# Pre-Money Shares).

Price Per Share = Pre-Money Valuation / # Pre-Money Shares

Price Per Share = Pre-Money Valuation / # Pre-Money Shares

5/ How many shares exist prior to the round? It is a question of agreed definition (and a source of confusion).

(a) In it for sure: existing shares + options that have been allocated.

(b) To be agreed: a number of options that have not yet allocated or even authorised yet.

(a) In it for sure: existing shares + options that have been allocated.

(b) To be agreed: a number of options that have not yet allocated or even authorised yet.

6/ Why the new options?

VCs calculate their return profiles based on ownership, and like to know how much they will own by the time you get to the next round.

VCs calculate their return profiles based on ownership, and like to know how much they will own by the time you get to the next round.

7/ So it is customary to “budget” say 18 months worth of options required for team building ... so that the ownership number is a “true reflection” of what the investors will own.

8/ The ownership that exists AFTER inclusion of all new options and all new shares is what is known as “Fully Diluted Ownership” and the resulting cap table is known as “Fully Diluted Equity”

Think of unallocated Options as “unseen dilution” or “yet to happen” dilution.

Think of unallocated Options as “unseen dilution” or “yet to happen” dilution.

9/ Usually in a term-sheet you will see wording such as: “the Pre-Money will include a number of Options such that the unallocated option pool represents 10% of the fully diluted equity”...

10/ This just means: "we will plug in a number of new options such that the unallocated number of options after the round is 10% — and these options will part of the Pre-Money Shares".

11/ You can see that having more options in the Pre reduces the Price Per Share of the round (and can do so quite significantly).

There’s nothing wrong with this, but some VCs might conveniently fail to explain that math to you and hope you focus only on the pre-money number.

There’s nothing wrong with this, but some VCs might conveniently fail to explain that math to you and hope you focus only on the pre-money number.

12/ When you compare two funding options from two different investors, always build the cap table and look at the effective price per share.

THE PRICE PER SHARE NEVER LIES.

It captures everything.

THE PRICE PER SHARE NEVER LIES.

It captures everything.

13/ I cannot resist to point you towards @nivi’s seminal “Option Pool Shuffle”. Throwback !

venturehacks.com/option-pool-sh…

And here is a simple cap table you can use. Everything is a variation on this - keep it simple.

docs.google.com/spreadsheets/d…

venturehacks.com/option-pool-sh…

And here is a simple cap table you can use. Everything is a variation on this - keep it simple.

docs.google.com/spreadsheets/d…

14/ Convertible Notes (SAFEs, Convers, SeedFast, ASI) are quasi-equity instruments that specify a fixed conversion price for the note into equity or specify a cap (where Conversion Price is lower of actual value or Cap).

15/ This is no different - don't get thrown off thinking this is complex - there is a Valuation specified for the company at which the shares will convert based on the rules of the note.

16/ What’s up with Pre-Money Note versus Post-Money Notes ?

In a Pre-Money Note, the PRE-money is fixed (and the Post-Money increases as you add more investors and cash).

In a Post-Money Note, the POST-money is fixed (and the Pre-Money decreases as you add more cash).

In a Pre-Money Note, the PRE-money is fixed (and the Post-Money increases as you add more investors and cash).

In a Post-Money Note, the POST-money is fixed (and the Pre-Money decreases as you add more cash).

17/ Benefit of a Post-Money Note: investors know exactly how much they will own (regardless of how much you decide to raise).

They are the simplest to grok but you of course have to make sure you don’t raise crazy amounts.

If I invest $1M at $10M post I KNOW I will own 10%.

They are the simplest to grok but you of course have to make sure you don’t raise crazy amounts.

If I invest $1M at $10M post I KNOW I will own 10%.

18 If you’re running multiple notes you MUST run an accurate cap table to ensure you’re not getting silly dilution over time.

[These can create some circularity and can be a bit tougher to model but it’s not rocket science].

[These can create some circularity and can be a bit tougher to model but it’s not rocket science].

19/ Notes are used for rolling closes and make life easy for founders.

In a classic "priced round", the round size is agreed, the investors are agreed and everyone comes in together, though sometimes you leave some flex for a second closing.

In a classic "priced round", the round size is agreed, the investors are agreed and everyone comes in together, though sometimes you leave some flex for a second closing.

20 The jargon may sound off-putting but the concepts are simple.

Understand the definitions and build the cap table. Ask the investor for their cap table so you are sure there’s no confusion.

Compare offers on an apple-to-apples basis by comparing the Price Per Share.

Understand the definitions and build the cap table. Ask the investor for their cap table so you are sure there’s no confusion.

Compare offers on an apple-to-apples basis by comparing the Price Per Share.

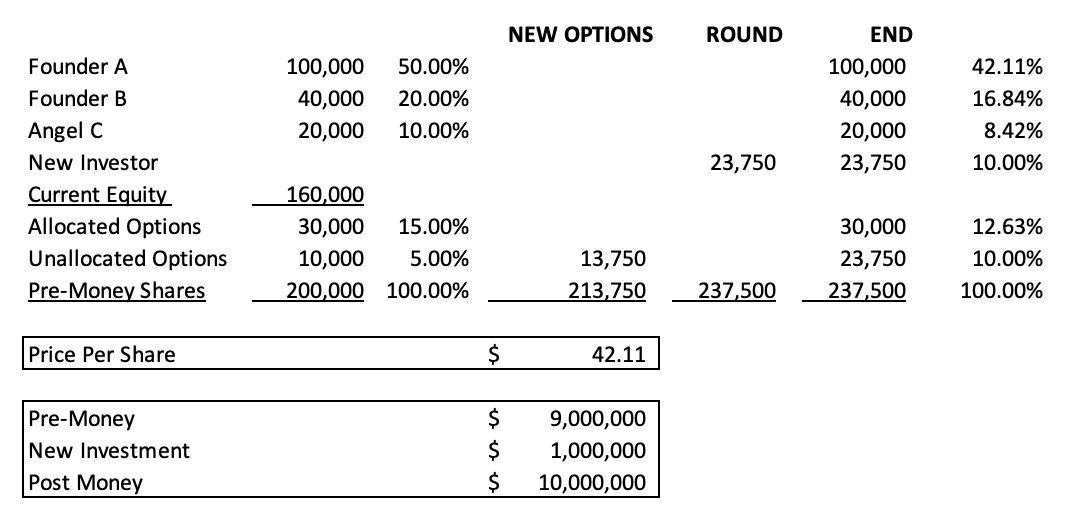

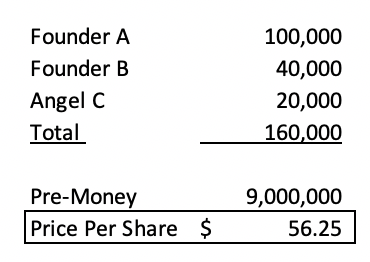

21/ Some illustrations - Before the Round (no options)

22/ Before the Round (with existing options)

23/ Before the Round (with existing AND new options) - PPS drops to $42.

24/ Post the round, after the investment