Now for what I see as the most disappointing aspect to the Fed's framework review...the doubling down on inflation targeting.

I think the Fed rightly sees its primary error as one of insufficient accommodation, but the reasoning and remedy are both flawed

medium.com/@skanda_97974/…

I think the Fed rightly sees its primary error as one of insufficient accommodation, but the reasoning and remedy are both flawed

medium.com/@skanda_97974/…

The thrust of this framework review has primarily centered around inflation. The Fed believes that inflation outcomes will self-perpetuate through the ever-unfalsifiable belief in the role of inflation expectations. By committing to more inflation, expectations will shift too...

I fear that as the Fed tries to educate the public about what it means for inflation to "average 2%," there is only going to be more attention paid to a fickle noisy messy macro variable that does not serve as a reliable guide to real-time macroeconomic analysis.

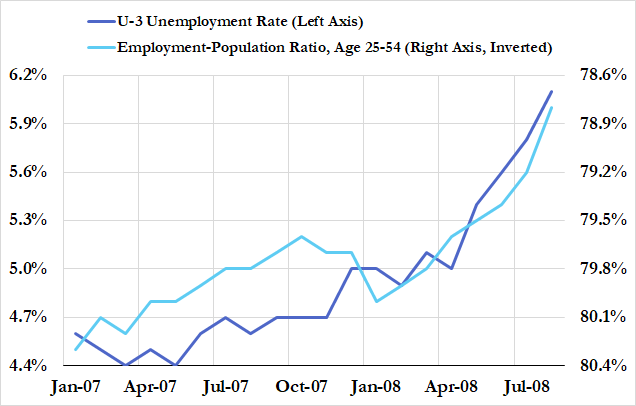

The summer of 2008 provides a very tangible example of what I'm talking about. The unemployment rate was rising, the economy was decelerating...but the Fed was reluctant to maximize accommodation out of fear of stoking higher inflation (such fears proved to be overstated).

A good framework should be robust to a variety of different scenarios. It's true that wage growth, inflation, and economic growth more generally are loosely correlated. But there might also be important divergences. How does average inflation targeting resolve this dilemma?

This is especially relevant to the current context. Employment remains historically depressed relative to population and estimates of the labor force, but by emphasizing average inflation, does a temporary spell of above 2% inflation (core or headline) warrant less accommodation?

I think if you asked Janet Yellen, she would say that this is compatible--that you can aim to average 2% while still delivering maximally accommodative policy to address historically low employment. But I doubt all FOMC members will see things similarly

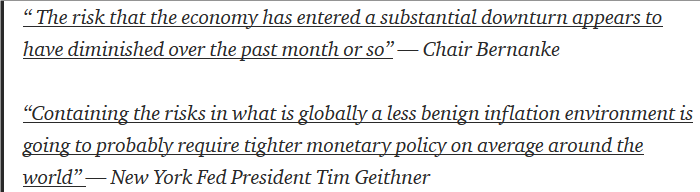

In the summer of 2008, even the dovish FOMC members were talking up the need for policy tightening. Bernanke was worried about high inflation and more complacent about mounting job losses. NY Fed President Tim Geithner was signaling a policy pivot...

wsj.com/articles/SB121…

wsj.com/articles/SB121…

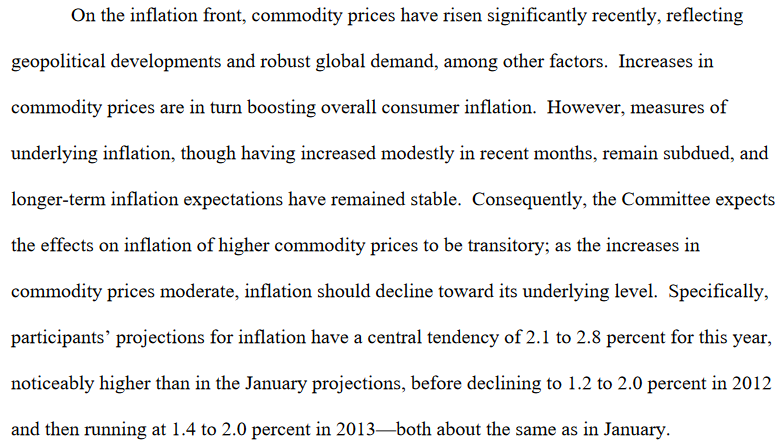

It shouldn't come as a surprise that financial markets bought into the inflation-centric framework and Fedspeak of the moment and extrapolated accordingly from the surge in commodity prices.

Spoiler alert: the Fed ultimately cut interest rates another 200bps by the end of 2008

Spoiler alert: the Fed ultimately cut interest rates another 200bps by the end of 2008

While it is a stretch to say that faster Fed cuts would have helped us avoid the worst phase of the global financial crisis (the Sumner view), the Fed's hawkishness in this period was clearly not helpful for mitigating the crisis and recession. Inflation distraction can be costly

2008 was a historically extreme scenario but it is not alone in terms of the policy dilemma it poses. 2011 had a very similar dynamic. Rising headline inflation but a stalling economy. Labor market and income growth dynamics were pointing in one direction, inflation in the other

While Chair Bernanke improved his communication regarding the importance of preserving the recovery and looking past inflation volatility, but not everyone saw it the same way

fraser.stlouisfed.org/files/docs/his…

fraser.stlouisfed.org/files/docs/his…

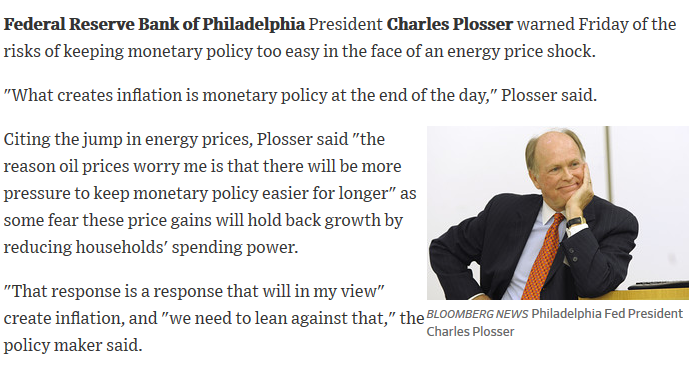

Philadelphia Fed President Charles Plosser was more concerned about how higher oil prices would ultimately be amplified through monetary policy into faster inflation.

blogs.wsj.com/economics/2011…

blogs.wsj.com/economics/2011…

Despite Bernanke's rhetoric about looking through inflation volatility, financial markets were not getting the message. I fear that when the rubber hits the road on "inflation averaging 2%," we are going to see similar problems in how markets interpret the Fed's reaction function

If you center the framework around inflation, you're at risk of making some serious errors. Even in 2011 the stakes were high. The Fed had (and ultimately did) come through with vital accommodation to cushion the blow from the Eurozone crisis and the shift to austerity.

The persistent inflation undershoot is indicative of something important but imperfectly so. We have had historically low nominal income growth (as well as low real output growth) over the same period. That provides a more tangible and meaningful illustration of the problem

The aggregation of everyone's paycheck (or revenue) is a more reliable business cycle barometer and more intuitive than the amalgamation of prices and methodologies that makes up PCE inflation. A missed opportunity to see the benefits of income targets

The Fed's newfound support for tight labor markets + the shift to an asymmetric treatment of employment are both positive steps. But if those shifts reflect something meaningful, it seems odd to center your strategy around a variable heavily divorced from labor market performance

I probably could do a separate thread on the procedural dimensions of this review. It seems really great that the Fed involved so many stakeholders that helped reshape their views of tight labor markets but noticeable absence of Congress and the White House is striking...

I'll end on this note: while there is value to operational independence, specifically in the execution of congressionally mandated goals, Paul McCulley's critique is worth revisiting regarding the limits of what the Fed should be defining for itself. cnbc.com/2018/10/17/mcc…