I believe for most investors, the easiest way to improve their risk-adjusted returns is not to get better at "picking winners" but to get better at diversification and portfolio construction.

A short 🧵 on why that is and how to do it...

A short 🧵 on why that is and how to do it...

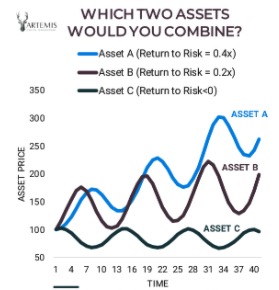

As a simple example, let’s say you have the ability to buy two assets out of a possible three choices.

The first two assets (Asset A and Asset B) have positive returns but are highly correlated; they track one another and the business cycle. Both do well when markets are up and poorly when markets are down.

The third asset (Asset C) loses money overall. It has a negative return. However, while asset loses money overall, it makes profits in periods where markets are falling. Its most substantial gains are reserved for the periods when the other assets are in crisis.

If you can only buy one asset, Asset A or Asset B is certainly the most appealing.

But, if you can buy two, what is the best overall portfolio?

But, if you can buy two, what is the best overall portfolio?

Obviously, this is a trick question.

Counterintuitively, the portfolio that combines the negatively correlated (Assets A+C) outperforms dramatically from a risk/reward perspective, even though Asset C has a negative yield.

Counterintuitively, the portfolio that combines the negatively correlated (Assets A+C) outperforms dramatically from a risk/reward perspective, even though Asset C has a negative yield.

In other words, anti-correlations is worth MORE than excess return.

In this example, by combining Assets A and C, which are negatively correlated to each other, when Asset C goes down, Asset A tends to go up, and vice versa.

In this example, by combining Assets A and C, which are negatively correlated to each other, when Asset C goes down, Asset A tends to go up, and vice versa.

By combining A+C, you can generate the same long-term returns as A+B with much less risk. Though it’s counterintuitive, that is how the math works out.

Most investors don't do this in practice though!

They think purely in terms of expected value: "I like this stock and that stock"

But, diversification math shows that you can combine lower returning individual assets for a higher portfolio return.

They think purely in terms of expected value: "I like this stock and that stock"

But, diversification math shows that you can combine lower returning individual assets for a higher portfolio return.

If you like this stock, can you then find something else you like less, but should behave in a negatively correlated way?

If you want to increase your return, it is safer* adding leverage to the balanced portfolio (Assets A+C) rather than using a portfolio that has correlated risks (Assets A+B).

I say safer with an asterisk because that obviously assumes that the correlations between A&C hold.

If A&C become correlated, then you can get in trouble.

If A&C become correlated, then you can get in trouble.

This is the other mistake most investors seem to make.

They think they have this diversified portfolio of domestic stocks, international stocks some index funds, some single names, a little fixed income, etc.

They think they have this diversified portfolio of domestic stocks, international stocks some index funds, some single names, a little fixed income, etc.

These portfolios seem diversified in good times but when you have a big crash and liquidity dries up, it turns out that you just had 20 barely different flavors of the same short volatility trade on.

Short volatility is just another way of saying "risk on" or "long GDP" - it is a bet on the good times continuing.

But, to get the benefits of diversification that allow you to compound wealth faster, you need something in your portfolio that is long volatility and benefits when markets go risk-off.

Obviously, I am talking my own book to some extent here as this is what @MutinyFund is trying to do, but even many sophisticated investors I know don't accept these two basic facts:

1. The returns of a portfolio are "other than the sum of its parts" - combining uncorrelated or anti-correlated assets can improve portfolio-level returns.

2. Using assets that are uncorrelated in "good times" but become correlated in a large drawdown =/= diversification.

2. Using assets that are uncorrelated in "good times" but become correlated in a large drawdown =/= diversification.

Some people believe that Asset C doesn't really exist which is a fair argument and worth taking seriously (though I disagree), but most don't even get to that point and miss the first two essential points!

All images used in this thread are from @ArtemisVol.

This argument is made much better and more persuasively in @vol_christopher's latest paper "The Allegory of the Hawk and the Serpent - docsend.com/view/taygkbn

I summarized the paper here: mutinyfund.com/thedragon/

This argument is made much better and more persuasively in @vol_christopher's latest paper "The Allegory of the Hawk and the Serpent - docsend.com/view/taygkbn

I summarized the paper here: mutinyfund.com/thedragon/

Most implementations of this grow out of Harry Browne's Permanent Portfolio which is worth looking at

joshkaufman.net/permanent-port…

joshkaufman.net/permanent-port…

My key takeaways on diversification and portfolio construction:

1. Investors should spend less time trying to "pick winners" and focus more on portfolio construction and diversification.

2. True diversification requires owning other assets than just stocks and bonds.

1. Investors should spend less time trying to "pick winners" and focus more on portfolio construction and diversification.

2. True diversification requires owning other assets than just stocks and bonds.

@threadreaderapp unroll