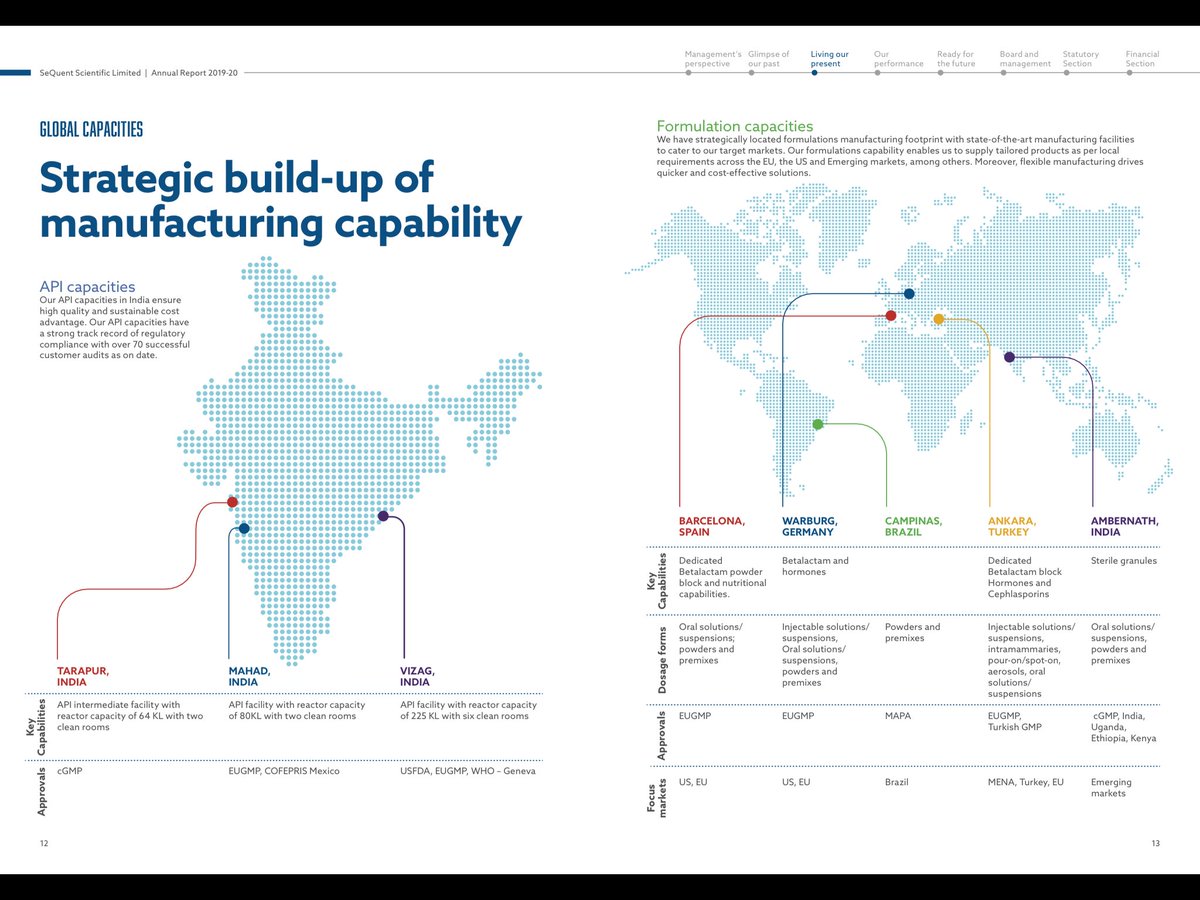

#AR2020 Rarely comes AR which confuses if its well written to entice you or something special. A potential Long-Term story (rare for me) barring few concerns. Must read to know industry #sequentScientific. Thanks to @unseenvalue n @punitbansal14 for bringing this story to us🙏

• • •

Missing some Tweet in this thread? You can try to

force a refresh