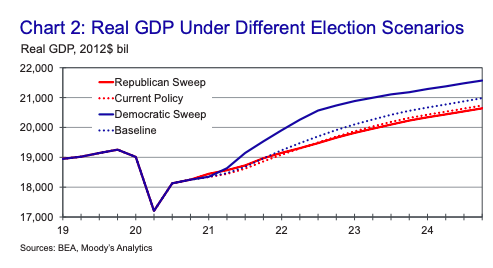

Moody's Analytics — not a partisan organization — says that the economy will be much stronger if Biden wins than if Trump hangs on. What's interesting, and a bit bittersweet for those of us who remember the last crisis, is why they say this 1/ moodysanalytics.com/-/media/articl…

Basically they say that under Biden government spending will be higher, that this will lead to faster recovery, and that with low interest rates debt won't be a problem. And this seems to be conventional wisdom across much of the spectrum 2/

But the same thing was true in 2010; yet all the Very Serious People were calling for fiscal austerity, saying that it would improve confidence, and warning about the dangers of debt 3/ nytimes.com/2010/07/02/opi…

It now seems to be almost universally acknowledged that this was a serious mistake; but somehow we got there without anyone admitting that they were wrong before. Oh well 4/

And, of course, if we have a Biden presidency Republicans will suddenly rediscover the evils of budget deficits and try to sabotage things as much as possible 5/

• • •

Missing some Tweet in this thread? You can try to

force a refresh