As a follow up to our thread on relevance, Netflix in the Media industry is a great example of dynamism within the context of moat relevance… 1/x

https://twitter.com/IntrinsicInv/status/1304447317622296581?s=20

This is the classic Christensen cultural/financial issue incumbents have in adapting to disruption... 2/x

bloom.bg/36aKtHk

bloom.bg/36aKtHk

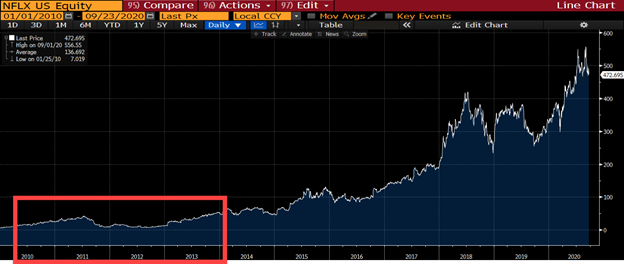

In contrast to Viacom+most incumbents, @Netflix’s culture enabled it to accept the pain of -75% decline in its stock price in 2011 to transition effectively from legacy DVD by mail… after winning rental battle with Blockbuster 3/x

To Streaming video... though the investment by pivoting cost it an 87% decline in operating profit from $400MM to $50MM, it opened up a larger more sustainable TAM supporting $NFLX next decade of growth runway… 4/x

@reedhastings leadership was key in successful decision & timing of pivot in conjunction with technology… in investor meetings during DVD heydays, everyone "knew" streaming would disrupt DVD business... "being early is no different than being wrong", but neither is too late! 5/x

Lessons from his prior company shaped $NFLX policies of “talent-density”, “leading with context not control”, “freedom & responsibility” in creating a culture of innovation, risk-taking, ownership, & accountability described in his book #NoRulesRules 6/x

bit.ly/3mUsoU3

bit.ly/3mUsoU3

Though @reedhastings comments focus on innovation above, they extend to other systemic process-driven frameworks prone to ossification, esp. linked to prior success & incentive structures, like business model, strategy, talent mix, go-to-market, capital allocation, etc. 7/x

Transition to streaming drove content/competitive strategy from *regional licensing* of 3rd party content to *global owned* originals, changes to business strategy/skills, while increasing capital intensity & morphing capital structure... "talent density" was indeed critical! 8/x

The successful flywheel underpinning $NFLX business model… 9/x

Using critical, differentiated in-house capabilities necessary to create competitive advantage in an orthogonal content delivery & business model vs industry incumbents, aka @HamitonHelmer type “counter-positioning”… 10/x

Driving scale in content to fuel flywheel momentum… growing subscribers/revenue @ 28%/35% CAGR 2012-19 meant $NFLX could grow its content spend at nearly 10x the incumbents over the time frame from $1.7B to $15B…11/x

Opportunistically utilizing cheap LT debt to accelerate scaling global subs, revenue, & content beyond its own cashflow, building its lead while incumbents were “still asleep at the switch”, enjoying cashflow from optimized, "walking dead" Pay-TV based business models… 12/x

@mjmauboussin articulates $NFLX’s financial dynamics in growth stage in his latest paper when describing $WMT ($HD fits description too), only its investments in stores while NFLX’s are in global content & tech infrastructure: 13/x

mgstn.ly/34eO58T

mgstn.ly/34eO58T

Framing $NFLX’s strategy this way starts to make sense with confirmation from industry veterans straddling both sides of the technology shift. 14/x

$NFLX’s results have become more clear and as its scale reaches a tipping point globally, with cashflows poised to turn positive in upcoming years demonstrated by widening gap between revenue and content spend... 15/x

Even in light of new expected competition from the only true, most worthy of legacy powers, $DIS with the force of #themouse and #babyyoda guided by the strategic hand of @RobertIger... 16/x

The irony of 2020 vs 2019 in DIS vs NFLX battle investors/media had set up as a narrative 17/x

on.ft.com/2GenZKv

on.ft.com/2GenZKv

Is that more consumer choice… 18/x

Has hastened the decline of legacy Pay-TV incumbent’s relevance... 19x

As streaming and other forms of entertainment have attracted away attention and freed up $$ to allocate to more relevant the alternatives (gaming, user generated content, social media)… 20/x

matthewball.vc/all/covidvideo

matthewball.vc/all/covidvideo

Than they have hurt Netflix’s position as a core service its subscribers value (thanks to its scale and consumer experience, it is the standard bearer for streaming video services): 21/x

Yet this is still early innings of global adoption of streaming, with a market that is broader than wired/satellite delivered video… 22/x

With enormous leverage to value creation in globally deployable business models with global relevance... 23/x

ben-evans.com/presentations

ben-evans.com/presentations

So let’s enjoy the show and see what comes next! 24/24

For a more depth look at Netflix, please check out our report on our blog, where we also have industry level analysis that led us to our thesis on Netflix and additional updates since.

intrinsicinvesting.com/2018/07/20/net…

intrinsicinvesting.com/2016/06/09/of-…

intrinsicinvesting.com/2016/08/16/of-…

intrinsicinvesting.com/2018/07/20/net…

intrinsicinvesting.com/2016/06/09/of-…

intrinsicinvesting.com/2016/08/16/of-…

• • •

Missing some Tweet in this thread? You can try to

force a refresh