12 things you should look out for before buying health insurance

A thread 🧵

A thread 🧵

It’s a good idea to make sure your health is protected under an insurance policy so that you don’t shell out large sums of money for hospitalization and treatment. But buying an individual health insurance policy can be daunting in itself.

Websites and policy documents can be overwhelming. There’s a lot of loaded terms, there’s a whole bunch of things that your policy may or may not cover. It’s important to know and understand the details though, so you’re not surprised later.

In this thread, we'll talk about the things you absolutely need to watch out for when buying an individual health insurance policy for yourself or your family members :)

If you take an individual health insurance policy and the insurance company offers to pay up to ₹15 lakhs during the year whenever you’re diagnosed with a disease or meet an accident, that amount is the 'sum insured'.

With that understanding out of the way, let’s talk about everything else you need to watch out for.

1. Co-pay

You have to be a little wary of policies that come with co-pay. With co-pay, you need to pay a pre-decided amount from your own pocket whenever you make a claim.

The larger your expenses, the larger you’ll end up spending your own money, even with insurance.

You have to be a little wary of policies that come with co-pay. With co-pay, you need to pay a pre-decided amount from your own pocket whenever you make a claim.

The larger your expenses, the larger you’ll end up spending your own money, even with insurance.

For example, if your insurance provides a ₹15 lakh cover, and you undergo surgery that costs you around ₹5 lakhs. If your policy has a co-pay of 20%, you will end up paying ₹1 lakh from your own pocket.

2. Room rent limit

This is something you need to be conscious of when making choices during hospitalization. Let’s deep dive into what will happen if your policy doesn’t have a room rent limit and when it does.

This is something you need to be conscious of when making choices during hospitalization. Let’s deep dive into what will happen if your policy doesn’t have a room rent limit and when it does.

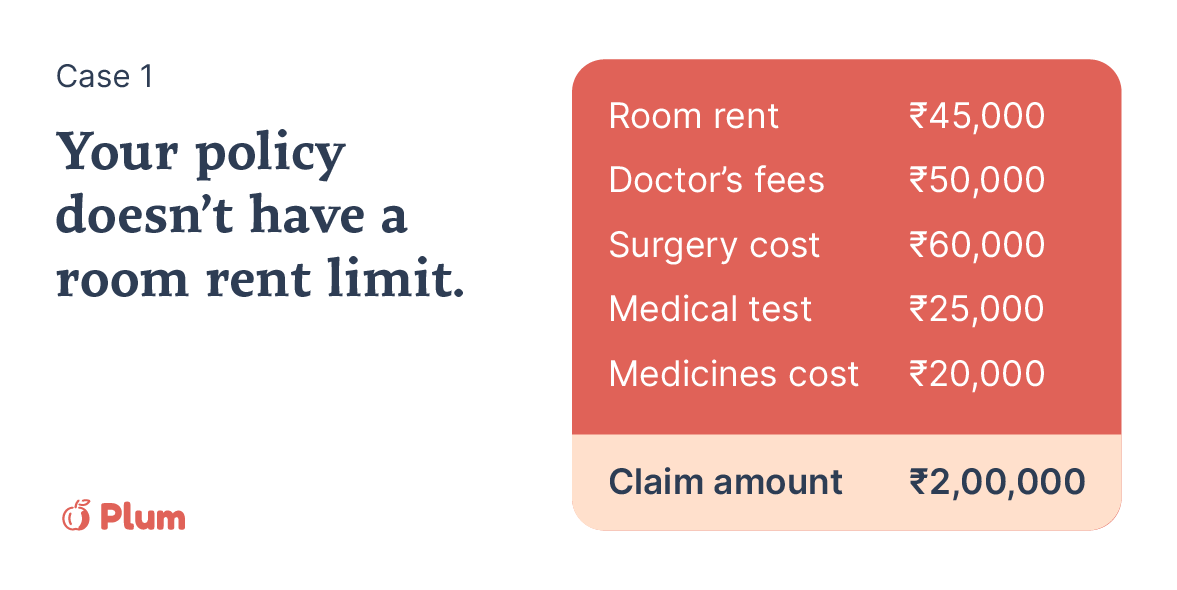

Case 1 - Your policy doesn’t have a room rent limit:

You have a health insurance cover of ₹15 lakhs, with *no room-rent limit*. You get treated for a condition that costs you ₹2 lakhs, and you paid ₹15,000 in room rent per day.

You have a health insurance cover of ₹15 lakhs, with *no room-rent limit*. You get treated for a condition that costs you ₹2 lakhs, and you paid ₹15,000 in room rent per day.

In this case, you can make a claim for up to 2 lakhs (which is the total cost of your treatment). All good here.

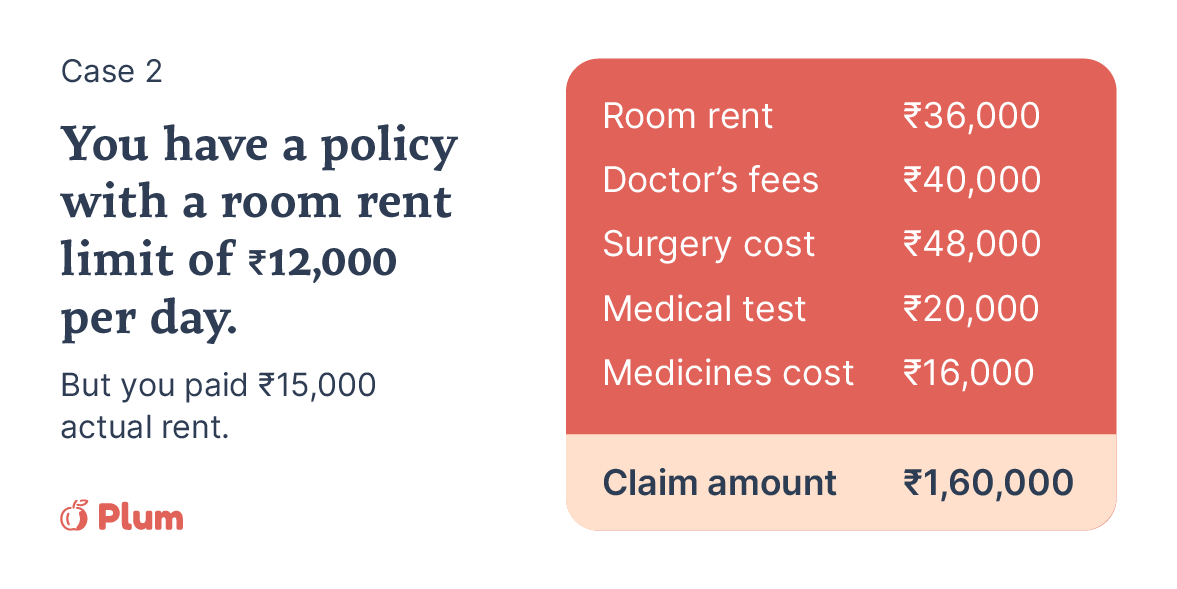

Case 2 - You have a policy with a room rent limit of ₹12,000 per day.

You have a health insurance cover of ₹15 lakhs, with a room rent limit of ₹12,000 per day. You get treated for a condition that costs you ₹2 lakhs, but you stayed in a room that costs you ₹15,000/day.

You have a health insurance cover of ₹15 lakhs, with a room rent limit of ₹12,000 per day. You get treated for a condition that costs you ₹2 lakhs, but you stayed in a room that costs you ₹15,000/day.

That's 3K more than the limit.

In this case, each component in your cost is proportionately deducted (12/15*cost), and therefore, you can only claim ₹1,60,000 of your total expenditure.

Check the attached image to understand how your claim amount gets reduced.

In this case, each component in your cost is proportionately deducted (12/15*cost), and therefore, you can only claim ₹1,60,000 of your total expenditure.

Check the attached image to understand how your claim amount gets reduced.

See what we mean? The amount you can claim is proportionately deducted based on the additional room rent you paid.

You might have thought the room rent doesn't matter as much - but it does.

You might have thought the room rent doesn't matter as much - but it does.

3. Initial waiting period

During this period after you purchase a policy, you cannot make any claim. It’s typically between 30 to 90 days. This waiting period is waived in the event of an accident that leads to immediate hospitalization.

During this period after you purchase a policy, you cannot make any claim. It’s typically between 30 to 90 days. This waiting period is waived in the event of an accident that leads to immediate hospitalization.

4. Waiting period for pre-existing diseases

This applies to pre-existing diseases (like diabetes) present when a health insurance policy is bought. The insurer will accept your claims for treatment related to these diseases only if the waiting period you agreed upon has passed.

This applies to pre-existing diseases (like diabetes) present when a health insurance policy is bought. The insurer will accept your claims for treatment related to these diseases only if the waiting period you agreed upon has passed.

5. Sub-limits on specific treatments

This means that the insurer applies a limit on the amount you can claim for treatments for specified conditions and diseases.

This means that the insurer applies a limit on the amount you can claim for treatments for specified conditions and diseases.

If you’re getting treated for kidney stones and the hospital charges you ₹80,000, but the insurer has a sub-limit of ₹60,000 for that treatment, you can’t claim the entirety of the amount you spent.

Tiring to look for these things already, isn’t it? Yeah, but you certainly need to be aware, or else, you’ll be surprised and disappointed when you make a claim later.

Save yourself that shock by going through the rest of this thread and also bookmarking it :)

Save yourself that shock by going through the rest of this thread and also bookmarking it :)

6. Free-look period

After you buy a policy, you can cancel it within a certain free-look period, stating your reasons.

However, the insurer will not refund any medical tests, stamp duty charges done during this period.

The free-look period is typically 15 to 30 days.

After you buy a policy, you can cancel it within a certain free-look period, stating your reasons.

However, the insurer will not refund any medical tests, stamp duty charges done during this period.

The free-look period is typically 15 to 30 days.

7. Pre and post hospitalization expenses

This is the facility given by the insurer to you, for covering your pre and post-hospitalization expenses.

This is the facility given by the insurer to you, for covering your pre and post-hospitalization expenses.

We suggest you get a policy that covers expenses at least 30 days before hospitalization and at least 2 months after hospitalization.

This will go a long way in saving you a lot of money (and stress!)

This will go a long way in saving you a lot of money (and stress!)

8. Daycare procedures

This means single-day treatments like eye surgery, etc. are covered by your health insurance policy.

Several common treatments require single day hospitalization, so you need to totally make sure that these are covered.

This means single-day treatments like eye surgery, etc. are covered by your health insurance policy.

Several common treatments require single day hospitalization, so you need to totally make sure that these are covered.

9. No-claim bonus

If you don't make any claim in a year, the insurer will reward you by increasing your coverage amount (with a max limit).

No claim bonuses are good-to-have on your policy.

If you don't make any claim in a year, the insurer will reward you by increasing your coverage amount (with a max limit).

No claim bonuses are good-to-have on your policy.

10. Domiciliary hospitalization

If your policy has a domiciliary cover (quite some insurance-speak!), it means that you can claim money when you are treated at home.

This is great during these times because it’s really difficult to find hospital beds during the pandemic.

If your policy has a domiciliary cover (quite some insurance-speak!), it means that you can claim money when you are treated at home.

This is great during these times because it’s really difficult to find hospital beds during the pandemic.

11. Moratorium period

If you’ve completed 8 years of coverage, the insurer cannot reject an eligible claim, for any reason except for proven frauds and exclusions made in the policy documents.

If you’ve completed 8 years of coverage, the insurer cannot reject an eligible claim, for any reason except for proven frauds and exclusions made in the policy documents.

This rule is effective from 1st April 2020 and every insurer has to comply with this rule. This is one more great reason to keep renewing your policy consistently!

12. Free health check-up

If you spot these words, it means the insurance company provides you with a free health check-up.

If you spot these words, it means the insurance company provides you with a free health check-up.

The offer may or may not depend on whether you made claims during a certain period. Only specific tests are covered and check-ups should take place at their network hospitals.

That’s all the things we think you should look out for - and we hope this helped! Is there anything else one should be mindful of when purchasing a policy?

Oh and btw, high five to @wiredmau5 whose tweets on health insurance some time ago inspired us to write this thread!

We don't have SoundCloud! But check out plumhq.com to get your team enrolled in a group health insurance policy and give them the gift of good health :)

• • •

Missing some Tweet in this thread? You can try to

force a refresh