Neogames $NGMS 🎰🎰🎰

🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥

▫️SaaS provider of iLottery solutions

▫️70 % market share in US

▫️highly scalable & high margins

▫️profitable

▫️sticky business

▫️huge potential for further growth

▫️undervalued

🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥

A thread 1/x ⬇️

🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥

▫️SaaS provider of iLottery solutions

▫️70 % market share in US

▫️highly scalable & high margins

▫️profitable

▫️sticky business

▫️huge potential for further growth

▫️undervalued

🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥🔥

A thread 1/x ⬇️

Business Overview

▫️ $NGMS has multi-year contracts with state lotteries to develop and manage their iLottery program

▫️Revenues calculated as a % of gross gaming revenue (GGR) or net gaming revenue (NGR) generated via iLottery platform

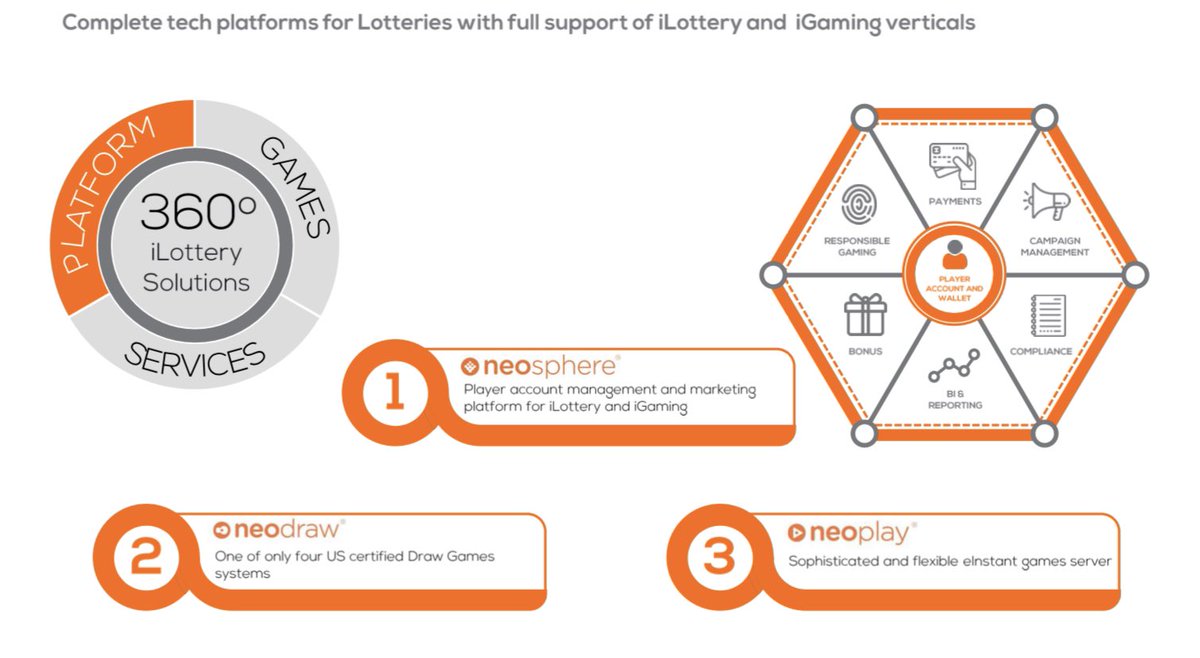

▫️ 360 degree iLottery solutions

▫️ $NGMS has multi-year contracts with state lotteries to develop and manage their iLottery program

▫️Revenues calculated as a % of gross gaming revenue (GGR) or net gaming revenue (NGR) generated via iLottery platform

▫️ 360 degree iLottery solutions

Technology platform

▫️neosphere: player account management and marketing platform for iLottery and iGaming

▫️neodraw: One of only four certified Draw Games systems

▫️neoplay: sophisticated and flexible eInstant games server

▫️neosphere: player account management and marketing platform for iLottery and iGaming

▫️neodraw: One of only four certified Draw Games systems

▫️neoplay: sophisticated and flexible eInstant games server

Neogames Studio

▫️350+ proprietary games

▫️15 years of experience

▫️30+ new games per year

▫️award winning games

▫️Driving the majority of iLottery GGR

▫️350+ proprietary games

▫️15 years of experience

▫️30+ new games per year

▫️award winning games

▫️Driving the majority of iLottery GGR

Operational Services

▫️payments managements

▫️compliance

▫️Tech operations

▫️Customer support

▫️Data analysis

▫️Marketing & CRM

▫️payments managements

▫️compliance

▫️Tech operations

▫️Customer support

▫️Data analysis

▫️Marketing & CRM

iLottery market

▫️Long sales cycles

▫️Long term relationships (4-7 year contracts)

▫️high vendor switching costs

▫️growth alongside traditional lottery

▫️Preference for turnkey solutions

▫️Revenue share contracts - customer (state lotteries) responsible for marketing spend

▫️Long sales cycles

▫️Long term relationships (4-7 year contracts)

▫️high vendor switching costs

▫️growth alongside traditional lottery

▫️Preference for turnkey solutions

▫️Revenue share contracts - customer (state lotteries) responsible for marketing spend

USA

▫️market leader with 70 % market share

▫️currently 77 % of the US with access to lottery but without access to iLottery

▫️further legislation expected in many states

▫️huge potential for further growth

▫️50/50 JV (NPI) with Pollard Banknote to serve the US market

▫️market leader with 70 % market share

▫️currently 77 % of the US with access to lottery but without access to iLottery

▫️further legislation expected in many states

▫️huge potential for further growth

▫️50/50 JV (NPI) with Pollard Banknote to serve the US market

Growth driver

1️⃣ Existing market penetration expansion

2️⃣ Winning new US Turnkey Contracts

3️⃣ Growing Game Studio Customer Base

4️⃣ Expanding the scope of existing contracts

5️⃣ Expanding geographical presence and range of offerings

1️⃣ Existing market penetration expansion

2️⃣ Winning new US Turnkey Contracts

3️⃣ Growing Game Studio Customer Base

4️⃣ Expanding the scope of existing contracts

5️⃣ Expanding geographical presence and range of offerings

Financials 2020

▫️Revenue +67 %

▫️NPI contributed 16 % of revenue (+ 375 %🔥)

▫️adj. EBITDA + 141 %

▫️48.8 % EBITDA margin

▫️first profitable year

▫️Guidance for '21 expects Revenue growth of 32-40% but additional contracts or further deregulation ist not included

▫️Revenue +67 %

▫️NPI contributed 16 % of revenue (+ 375 %🔥)

▫️adj. EBITDA + 141 %

▫️48.8 % EBITDA margin

▫️first profitable year

▫️Guidance for '21 expects Revenue growth of 32-40% but additional contracts or further deregulation ist not included

Valuation 📈

▫️EV/S '21 of ~12

▫️P/E '21 of ~ 74

▫️estimated profit growth of over 74% for '21 and over 90% for '22

▫️PEG Ration < 1

▫️additional opportunities through further contracts not included in estimations

▫️EV/S '21 of ~12

▫️P/E '21 of ~ 74

▫️estimated profit growth of over 74% for '21 and over 90% for '22

▫️PEG Ration < 1

▫️additional opportunities through further contracts not included in estimations

Summary 🎰🎰🎰

Regarding the sticky business with long term contracts, the market leadership in NA, the growing online gambling market, ongoing legislations, high margins and high profitable growth $NGMS is pretty undervalued imo and offers good returns.

⬇️

Regarding the sticky business with long term contracts, the market leadership in NA, the growing online gambling market, ongoing legislations, high margins and high profitable growth $NGMS is pretty undervalued imo and offers good returns.

⬇️

The whole online gambling market is set to grow rapidly in the next years. With $EVO (Casino), $KAMBI (Betting) and $NGMS (State Lotteries) the fastest growing categories are covered with B2B providers which offer better margins and profitabilty compared to operators like $DKNG

• • •

Missing some Tweet in this thread? You can try to

force a refresh