Coinbase just dropped the Q1 earnings and outlook. As expected higher revenue than in the entire 2020.

Q1 summary:

• ~$1.8 billion revenue

• Adjusted EBITDA of ~$1.1B

• Net income of $730-800M

• 56M verified users (+13M)

• 6.1M monthly transacting users (+3.3M)

Q1 summary:

• ~$1.8 billion revenue

• Adjusted EBITDA of ~$1.1B

• Net income of $730-800M

• 56M verified users (+13M)

• 6.1M monthly transacting users (+3.3M)

Growth over last quarter

• Revenue —> 207.6%

• Net income —> 312.9%

• Traded volume —> 272.0%

• Revenue —> 207.6%

• Net income —> 312.9%

• Traded volume —> 272.0%

Assets on Platform are ~$223B and $122B of that is coming directly from institutions.

Coinbase expects meaningful growth this year driven by increased institutional interest but admits that its insti revenue is inherently unpredictable

Coinbase expects meaningful growth this year driven by increased institutional interest but admits that its insti revenue is inherently unpredictable

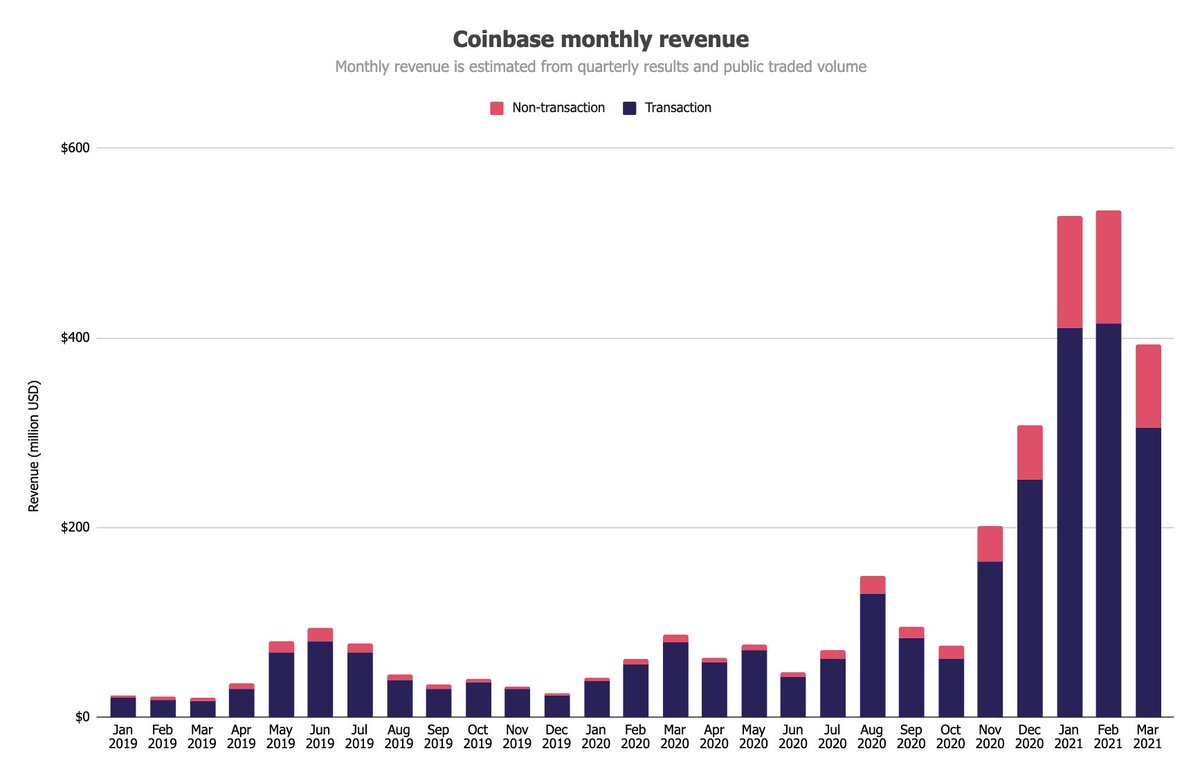

This is not unexpected but just to illustrate how crazy the growth has been, this chart says it all

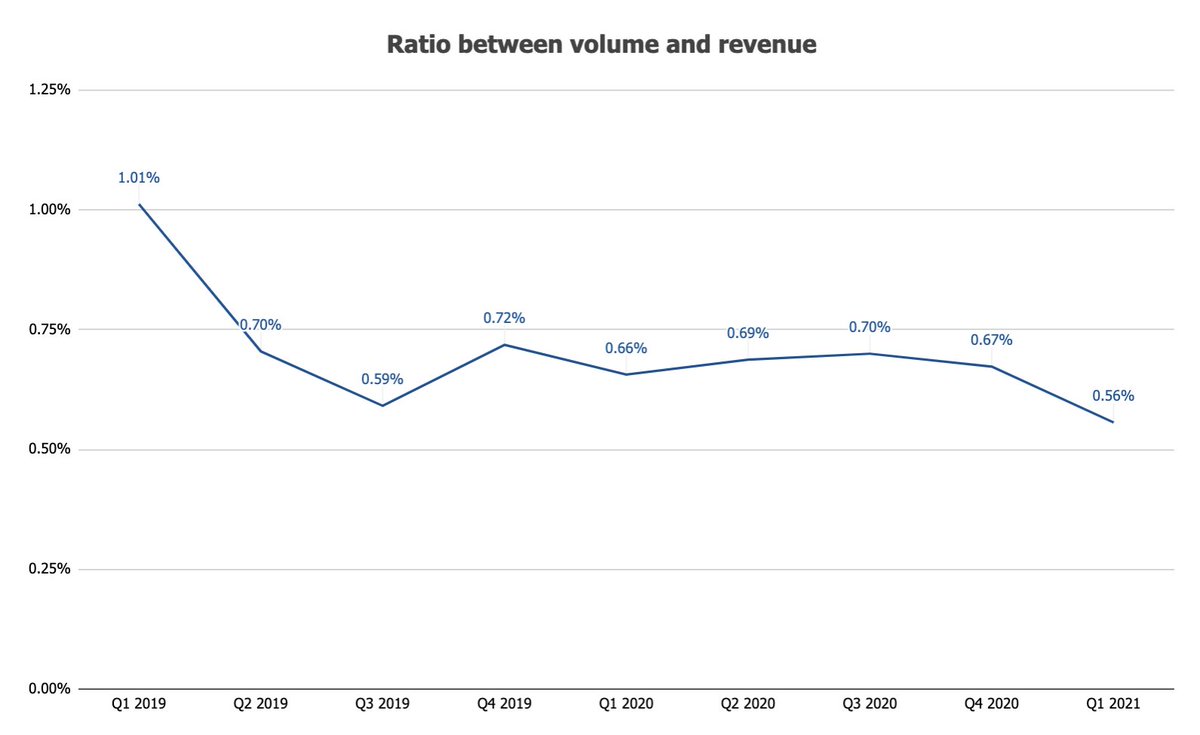

As expected, the ratio between volume and revenue has declined from 0.67% to 0.56%. This is simply because way more volume also means way more market makers and fees get skewed lower. But the ratio is still higher than I expected, which means more retail has come!

Talk about another absolutely bonkers chart of monthly active users

Unfortunately, this is about everything that Coinbase has given out right now. We were hoping for a more comprehensive update. If you want to read our analysis of these numbers tomorrow morning, become The Block Research member.

theblockcrypto.com/promotions/res…

theblockcrypto.com/promotions/res…

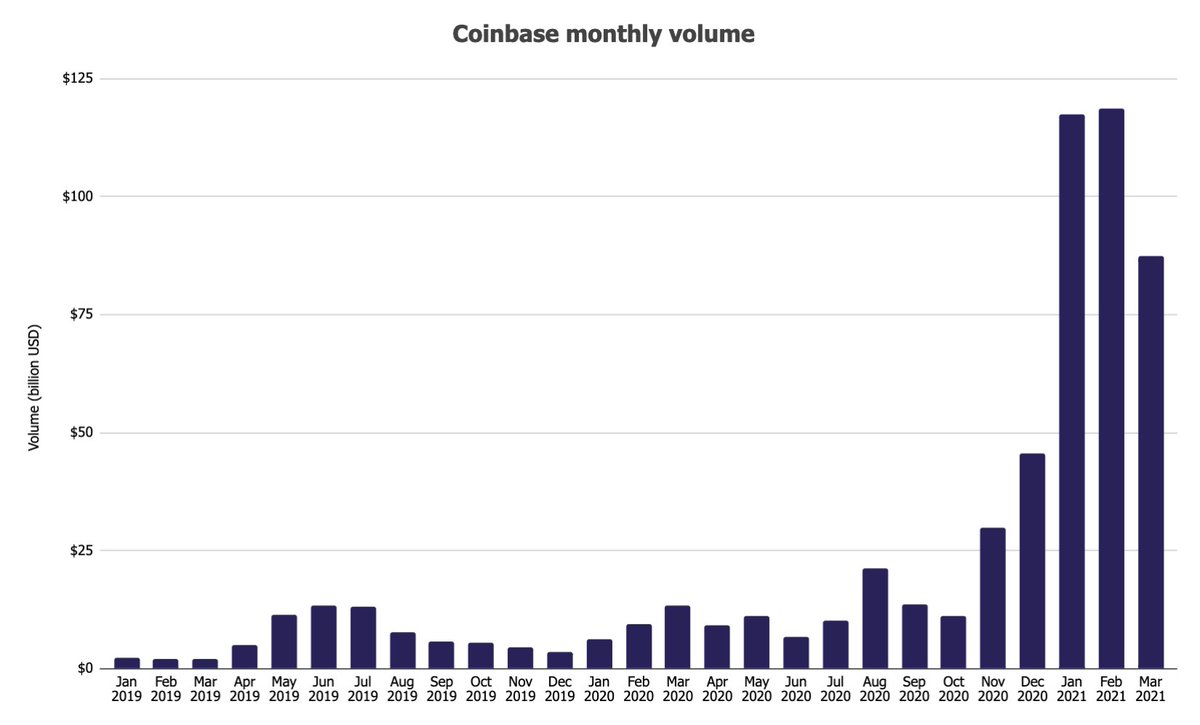

One last thing I will add since I'm seeing a lot of that - projecting revenue forward by assuming constant volume growth makes no sense to me. Coinbase volume is incredibly cyclical and if markets slow down a bit, it's totally possible we even see a decline. Just watch volume

• • •

Missing some Tweet in this thread? You can try to

force a refresh