The Made in 🇺🇸Tax Plan is out.

What is the problem & the plan to fix it? 1/10 👇👇👇👇 home.treasury.gov/system/files/1…

What is the problem & the plan to fix it? 1/10 👇👇👇👇 home.treasury.gov/system/files/1…

The labor share of US national income has been declining for years, representing a worrying trend for workers and a contribution to rising income inequality. This is exacerbated by a worldwide trend of governments shifting relative

tax burdens away from corporations 2/10

tax burdens away from corporations 2/10

U.S. corporate profits are at historic and comparative highs. The U.S. corporate sector is the most successful in the world: it hosts 37% of the Forbes 2000 companies by profit while the US accounts for 24% of world GDP. But corporate revenue has not seen a similar bonanza 3/10

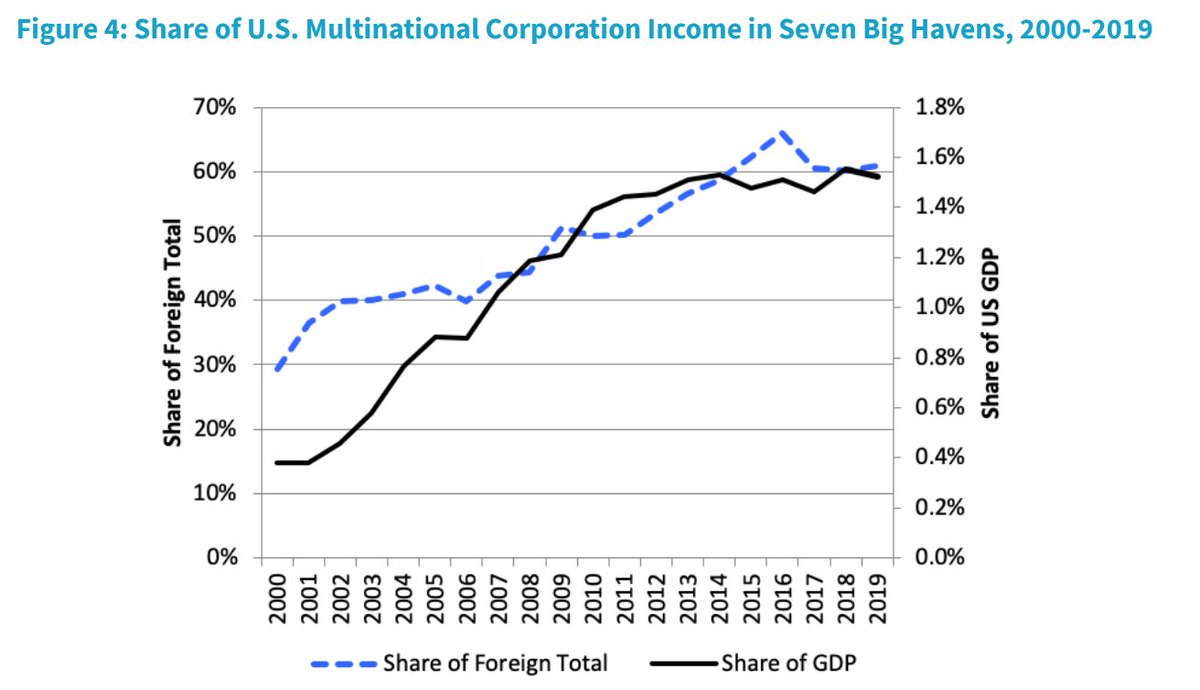

International tax rules have facilitated this trend. More U.S. profits are housed in tiny tax havens than in the economies of China, India, Japan, France, Canada, and Germany combined. Bermuda, a country of 64,000 people, shows 10% of all reported U.S. MNEs foreign profit. 4/10

What's the plan to fix it?

1⃣ Raise corporation tax rate to 28% "In addition to raising revenue to fund urgent fiscal priorities, raising the CT rate would also help attenuate inequality. The corporate income tax is one of the most progressive taxes in our tax system" 5/10

1⃣ Raise corporation tax rate to 28% "In addition to raising revenue to fund urgent fiscal priorities, raising the CT rate would also help attenuate inequality. The corporate income tax is one of the most progressive taxes in our tax system" 5/10

2⃣ Introduce a global minimum tax of 21% on US MNEs foreign profits on a country by country basis

3⃣ Introduce anti profit shifting rule (SHIELD) at a rate of 21% UNTIL there is a new rate agreed upon in the multilateral agreement at the @OECDtax

6/9

home.treasury.gov/system/files/1…

3⃣ Introduce anti profit shifting rule (SHIELD) at a rate of 21% UNTIL there is a new rate agreed upon in the multilateral agreement at the @OECDtax

6/9

home.treasury.gov/system/files/1…

4⃣ Patent Box is not an effective way to encourage research and development (R&D) in the US. It does not incentivize new domestic investment in R&D -it merely provides large tax breaks to companies with excess profits who are already reaping the rewards of prior innovation..

7/10

7/10

so the US Patent Box (FDII) which provides a preferential 13% tax rate will be REPEALED. Instead, $180 billion direct investment in R&D as part of American Jobs Plan. 8/10

5⃣ A 15% minimum book tax will apply to all large businesses to guarantee at least a minimum level of contribution irrespective of tax allowances (stock options etc) No more companies paying 0 federal taxes, despite reporting billions of $ in profits 2 shareholders. Clever. 9/10

Additional revenue from these and other measures will be used to fund the American Jobs Plan, a comprehensive proposal worth 1% of GDP aimed at increasing investment in infrastructure, the production of clean energy, the care economy, and other priorities. 10/10

• • •

Missing some Tweet in this thread? You can try to

force a refresh