Le he seguido dando vueltas a la exposición de motivos de la reforma tributaria. La conclusión a la que estoy llegando es que como dice el refrán "de eso tan bueno no dan tanto". Los supuestos beneficios de la RT son, en un su mayoría, resultado de mezclar 🍐con 🍎. Otro 🧵

La defensa de los méritos de la reforma se centra en este cuadro. Este muestra que el 10% más pobre del país aumenta sus ingresos un 68% mientras que el 10% mas rico reduce sus ingresos en un 4% en 2023. Redistribución!!!

El problema es que esas cifras que muestran una supuesta redistribución no están calculadas en el mismo escenario. Son resultado de la comparación de la situación de los mas pobres y los mas ricos en dos escenarios diferentes. 🍐y 🍎.

Y que tan diferentes son esos escenarios? Pues son el equivalente a comparar una situación donde todo sale bien, incluyendo que la selección Colombia gane la Copa del Mundo 2022, a que todo salga muy mal, incluyendo que Santa Fe salga siempre campeón en el torneo nacional.

El escenario CPL (donde todo sale bien) incluye (al menos) tres supuestos claves. Primero, que la reforma, gracias a confianza inversionista (¡) disminuye tasas de interés. Segundo, inversión publica aumenta PIB potencial. Tercero, un mercado laboral al revés.

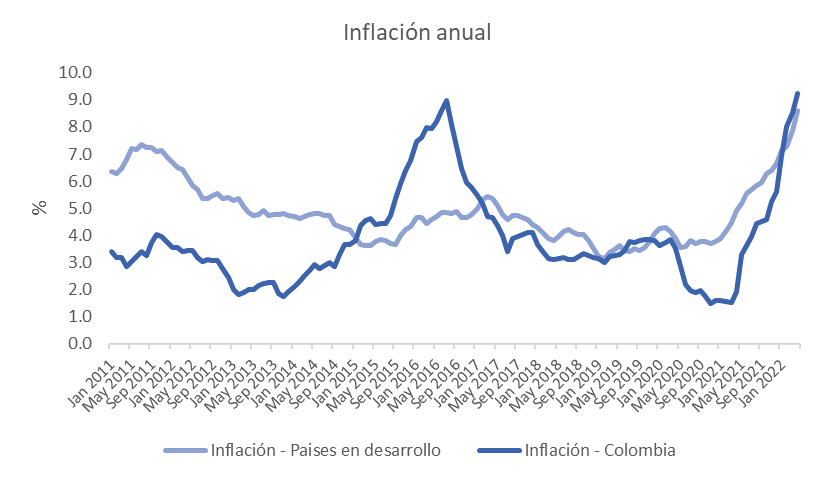

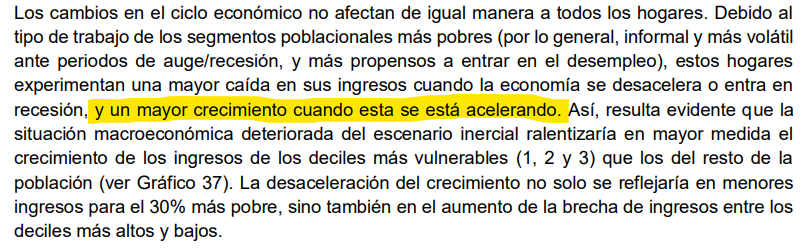

Como así que al revés? Modelo pareciera asumir una situación donde los mas vulnerables son los primeros en perder su empleo e ingresos (correcto) pero que en una recuperación son los primeros en recuperar empleo e ingresos (incorrecto). Normalmente son los últimos.

Y porque esto es importante? Porque entre menores tasas de interés, crecimiento turbo cargado y un mercado laboral que privilegia a los mas vulnerables (y tradicionalmente menor preparados) es lo que explica el rápido crecimiento de ingresos de deciles mas bajos en CPL.

Que pasa mientras tanto en el escenario Santa Fe (donde sale todo mal). Tasas de interés mas altas, default de deuda (ya saben, el castrochavismo 2022 no se lleva bien con los mercados), menor inversión pública, menor PIB potencial, y menor empleo.

El famoso 68% de ingresos mas altos sale de comparar el ingreso del decil mas bajo en los escenarios CPL y Santa Fe. Es decir que mezcla tres cosas. Además de transferencias, incluye diferencias de crecimiento y empleo entre ambos escenarios extremos para el decil 1.

El crecimiento y empleo parecen representar al menos las dos terceras partes de ese 68% si comparamos escenario CPL con inercial gasto (proxy Santa Fe) en 2023. El ultimo 30% se explicaría por transferencias y empleo (sin modelo no es posible separar efectos y deciles).

Al final del día, como el 68% sale de esta cuestionable comparación entre 🍐y 🍎, con muchos supuestos detrás de cada escenario, las cifras de impacto distribucional y de pobreza presentadas en la EM deben ser desagregadas con cuidado.

Esta desagregación requiere dos cosas. Primero, modelo utilizado para las proyecciones de crecimiento, con todos sus supuestos, de tal manera que pueda ser replicado. Segundo, como lo hace el CBO en Estados Unidos, hacer un análisis estático que aislé impacto distributivo de RT.

Ese análisis estático probablemente muestre efecto positivo del programa de transferencias. Sin embargo, no va a ser el citado 68% sino una cifra mucho menor. Esto tiene implicaciones importantes para lo que pase en otro extremo de distribución del ingreso.

Hay otro par de cosas que se me quedan en el tintero para otro dia. De momento, lo que se necesita es que el MinH comparta su modelo y cifras para poder debatir en igualdad de condiciones, con transparencia y evitar confundir al público.

Actualización de la discusión sobre la base de nueva información:

https://twitter.com/danielmunevar/status/1384360219677974529?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh