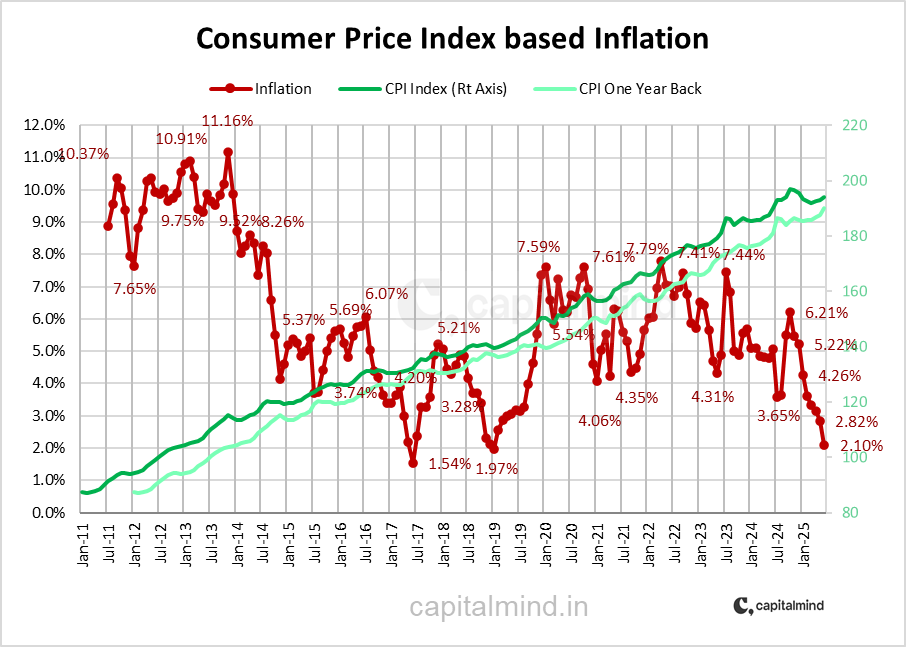

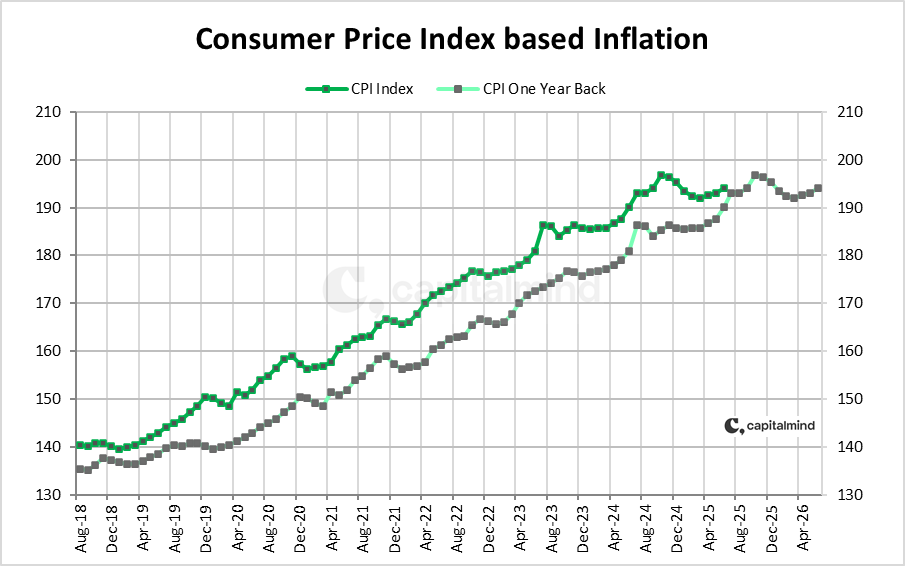

Retail individual investors are the biggest player in our markets. Not FIIs, and not mutual funds. Look at the equity market (non derivative). (Thread)

45% of India's stock market volumes are from retail investors. Up from 33% in 2016.

FIIs went from 23% down to 11%. Domestic institutions at 7%.

And look at the index futures market:

FIIs went from 23% down to 11%. Domestic institutions at 7%.

And look at the index futures market:

Individuals do 39% of index futures. FIIs merely 15%.

Domestic institutions are 1% - Rest is mostly prop books of brokers.

In index options, prop books dominate at 39%, but retail's gone up from 22% to 32%. FIIs only 16%.

Domestic institutions are 1% - Rest is mostly prop books of brokers.

In index options, prop books dominate at 39%, but retail's gone up from 22% to 32%. FIIs only 16%.

Even in Interest Rate futures (!!) retail seems to have suddenly gone to 14% of the market:

In essence, the market is largely traded by retail investors. Domesticmutual funds are a tiny part of the game. But here's a statistic that will shock you further.

Despite now having 45% of the trading volumes of the market, retail stock ownership has been flat the last three years, at only 18% of non-promoter shares ("float")

FIIs own 43%, Domestic MFs own 15%. Insurers and others have actually reduced their ownership as a %.

FIIs own 43%, Domestic MFs own 15%. Insurers and others have actually reduced their ownership as a %.

And then, from 2001, when promoters owned 40% of the market, now they own 50%.

FIIs went from under 10% to 21%.

Retail investors fell from 18% to 9%.

FIIs went from under 10% to 21%.

Retail investors fell from 18% to 9%.

Looks like foreign investors (and domestic mutual funds) don't trade that much but are continuously increasing their marketshare of ownership.

Retail is just the opposite!

Retail is just the opposite!

Source: NSE's awesome market pulse letter at: static.nseindia.com//s3fs-public/i…

For posterity: capitalmind.in/2021/05/omg-th…

• • •

Missing some Tweet in this thread? You can try to

force a refresh