Power sector, a bird's eye view thread : 🧵

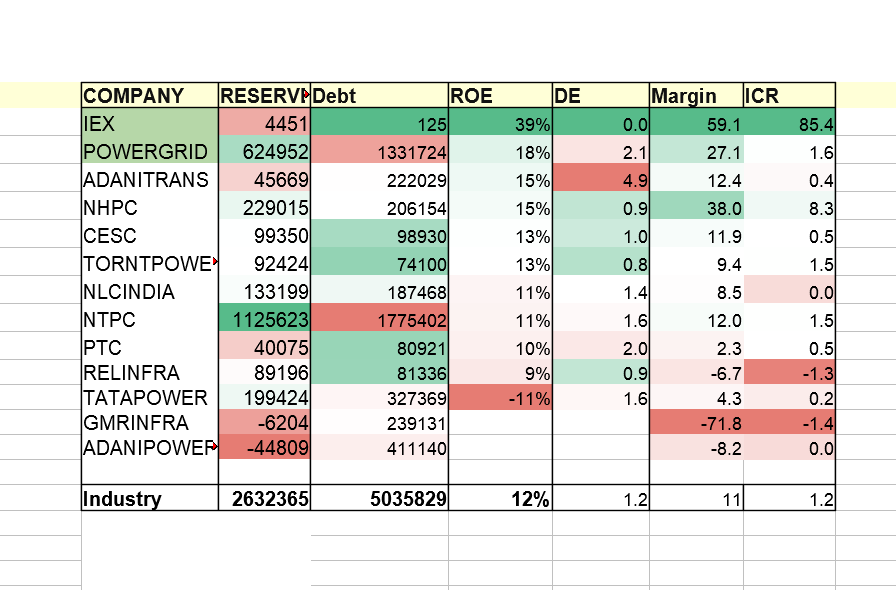

IEX and PowerGrid appear to be slightly better options (अन्धों में काना राजा) in a capital intensive and dud sector.

IEX and PowerGrid have made decent revenues and profits consistently for a decade.

Most companies in this sector are debt laden, with the exception of IEX, due to the unique nature of its business model.

IEX, again, puts up a better show in the margins department.

• • •

Missing some Tweet in this thread? You can try to

force a refresh