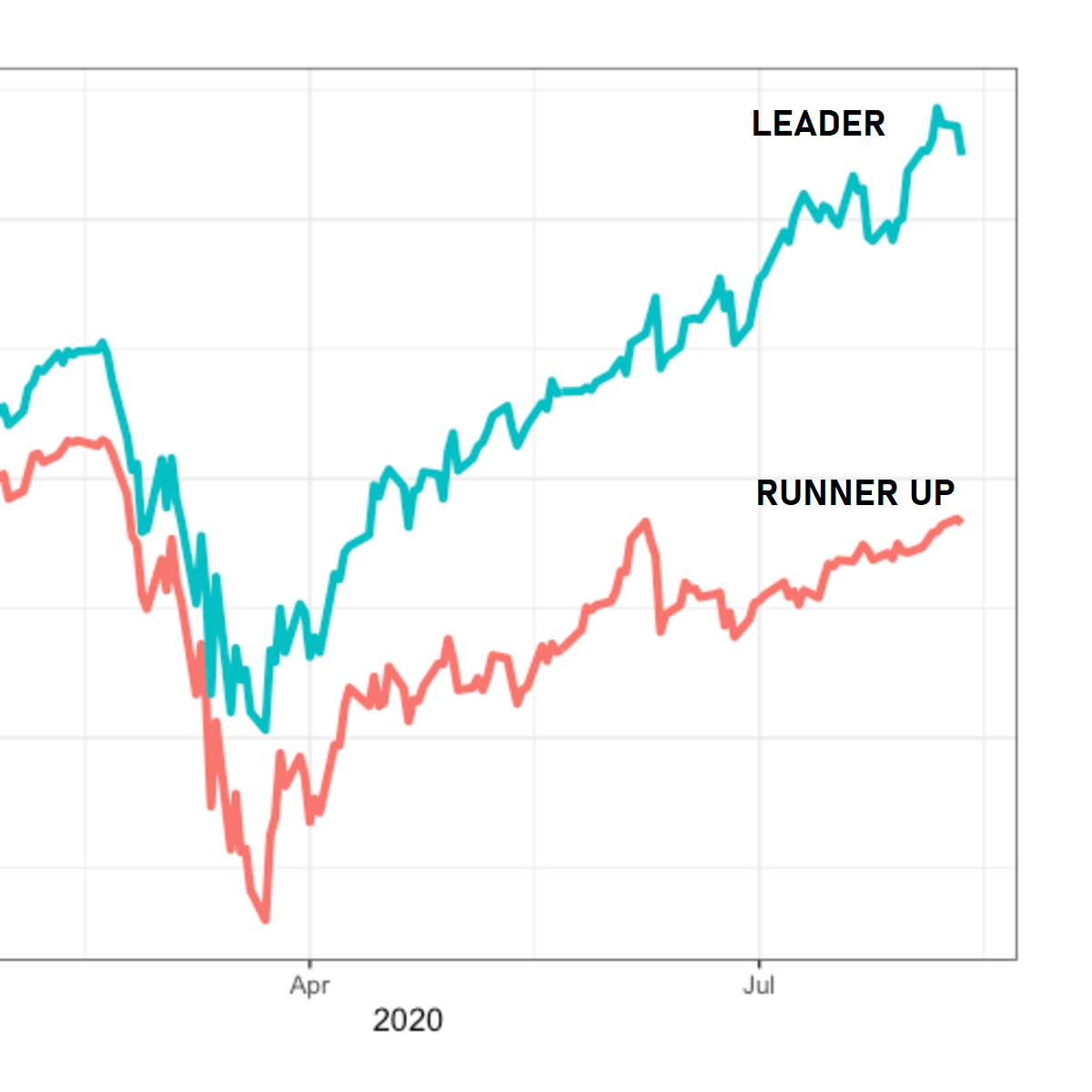

Should we only buy the leaders?

Should we only buy the leaders?  When they plotted out the damage these planes were incurring, it was spread out, but largely concentrated around the tail, body and wings. So the most natural impulse was to armor the parts with the most bullet holes.

When they plotted out the damage these planes were incurring, it was spread out, but largely concentrated around the tail, body and wings. So the most natural impulse was to armor the parts with the most bullet holes.

Earnings yields is mostly stable and smooth curve. It's the stock price that fluctuates due to sentiments, liquidity, news cycle, perception etc.

Earnings yields is mostly stable and smooth curve. It's the stock price that fluctuates due to sentiments, liquidity, news cycle, perception etc.  #SupremeInd management has diligently worked to eliminate their debt from 2008 to being completely debt free now.

#SupremeInd management has diligently worked to eliminate their debt from 2008 to being completely debt free now.

They have 2 major segments, pipes and adhesives. 77% revenue comes from Piping and the rest from Adhesives.

They have 2 major segments, pipes and adhesives. 77% revenue comes from Piping and the rest from Adhesives.

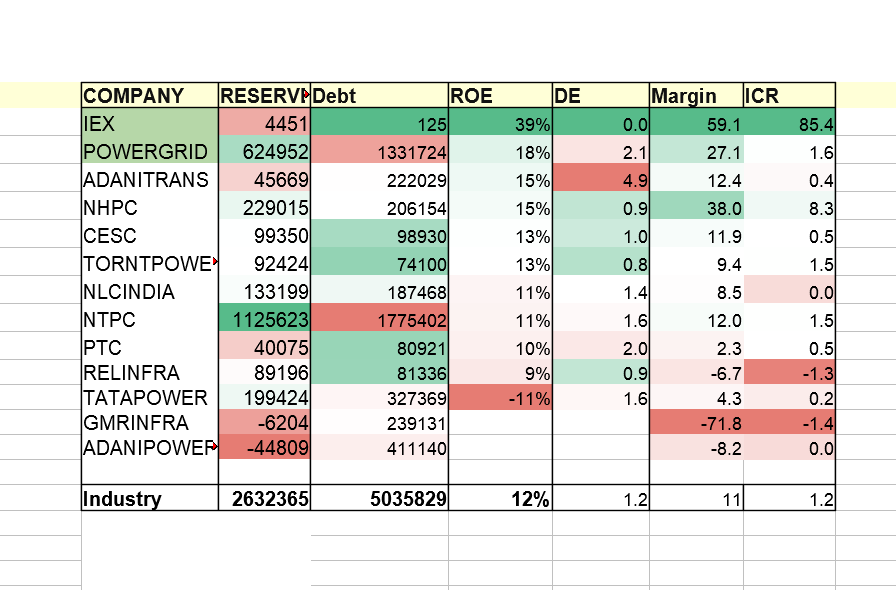

IEX and PowerGrid appear to be slightly better options (अन्धों में काना राजा) in a capital intensive and dud sector.

IEX and PowerGrid appear to be slightly better options (अन्धों में काना राजा) in a capital intensive and dud sector.

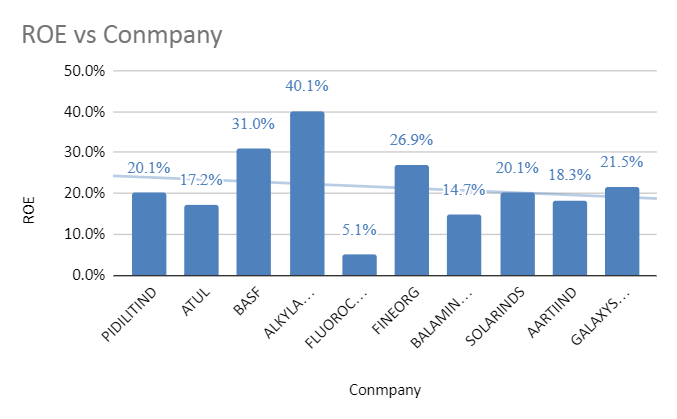

Pidilite, Atul, Alkyl amines, FinOrg have among the best ROE.

Pidilite, Atul, Alkyl amines, FinOrg have among the best ROE.

Presently all Insurance stocks are fully valued (i.e 4% margin priced in but 6% margin not priced in)

Presently all Insurance stocks are fully valued (i.e 4% margin priced in but 6% margin not priced in) Whereas, if the correction is taking its own time & allowing (i.e inviting) people to buy, it is usually a distribution prior to multi-year stagnation

Whereas, if the correction is taking its own time & allowing (i.e inviting) people to buy, it is usually a distribution prior to multi-year stagnation

Tata Elxsi profit trend :

Tata Elxsi profit trend :

Sorted by sales figures, it's clear that the market is rewarding TataElxsi with some premium marketcap, because there are companies which make similar sales but don't enjoy the same valuation (and with good reason) :

Sorted by sales figures, it's clear that the market is rewarding TataElxsi with some premium marketcap, because there are companies which make similar sales but don't enjoy the same valuation (and with good reason) :

Relaxo sales history :

Relaxo sales history :