THE SCOTUS OPINION CALLS THE NWS "PATH OF REHABILITATION"

It bought @TheJusticeDept's argument contending that the NWS was necessary to preserve the UST funding commitment,as the 10% div made(losses)FnF request draws from UST to pay it,depleting the funding commitment.#Fanniegate

It bought @TheJusticeDept's argument contending that the NWS was necessary to preserve the UST funding commitment,as the 10% div made(losses)FnF request draws from UST to pay it,depleting the funding commitment.#Fanniegate

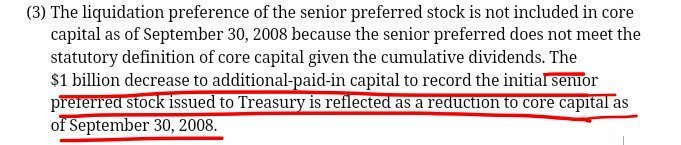

The Justice mixed up the Authority of UST to Purchase Obligations (SPS) that HERA required the emergency determination(ii)to prevent disruptions in the availability of mortgage finance, with the rehabilitation of FnF, which is exclusively the FHFA-C's power: "Put FnF in a sound

and solvent condition".I.e.,Recap and reduce the SPS,resp,what the Restriction on Capital Distributions and exception B,are about.

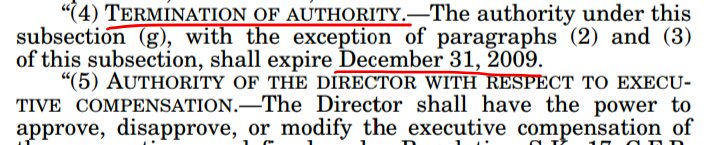

He mentioned the deadline to purchase obligations under this provision(g):Dec 2009,related to the purchase,not future purchase w/ funding commitment.

He mentioned the deadline to purchase obligations under this provision(g):Dec 2009,related to the purchase,not future purchase w/ funding commitment.

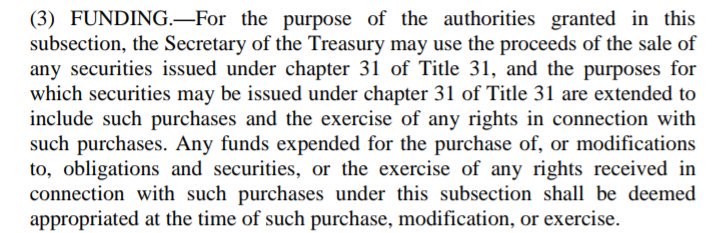

The current UST funding commtmt is illegal,as the authorization to purchase high yield obligations under this provision(g)expired in Dec 2009.The exception(3)FUNDING,is related to how the UST funds the draws of FnF,i.e.,the issuance of Public Debt.Unrelated to the funding commtmt

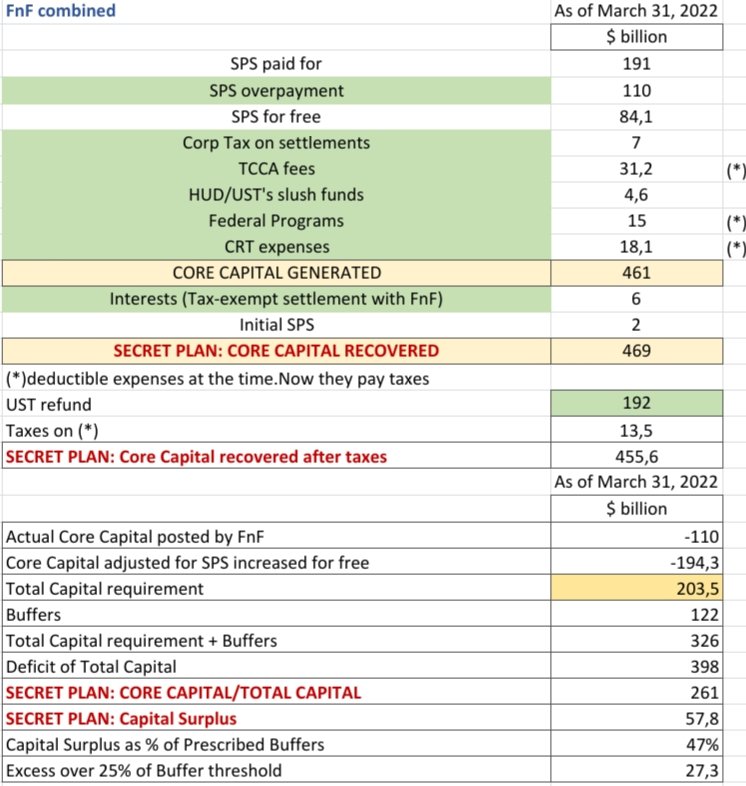

This is why the UST is doing the trick of not purchasing even one security,as either it gets SPS for free(also the Warrant), the SPS LP increases for free or the LP increases after a draw.

Instead,there's an original(prior HERA)low cost UST funding commitment mentioned by the

Instead,there's an original(prior HERA)low cost UST funding commitment mentioned by the

Scotus-amicus, Prof.Nielson,that the court disregarded, despite that this provision(c), has the same name as the one the Justice talks about(g)with high-yield obligations.

This original UST backstop(c) is the only exception to the Charter's Fee Limitation, that bars the UST from

This original UST backstop(c) is the only exception to the Charter's Fee Limitation, that bars the UST from

making profits using the securities or assets of FnF.

Obsolete backstop limited to $2.25b,irrelevant. Congress should've updated it. Anyway,the PA is deemed to have tacitly updated it.

The Charter's purpose is to make FnF get cheap funds on the mkt.A high yield backstop is crazy.

Obsolete backstop limited to $2.25b,irrelevant. Congress should've updated it. Anyway,the PA is deemed to have tacitly updated it.

The Charter's purpose is to make FnF get cheap funds on the mkt.A high yield backstop is crazy.

@threadreaderapp unroll

(*)The screenshot posted says that the provision with high yield obligations is (l), not (g), because it's the Charter of the other GSE.

• • •

Missing some Tweet in this thread? You can try to

force a refresh