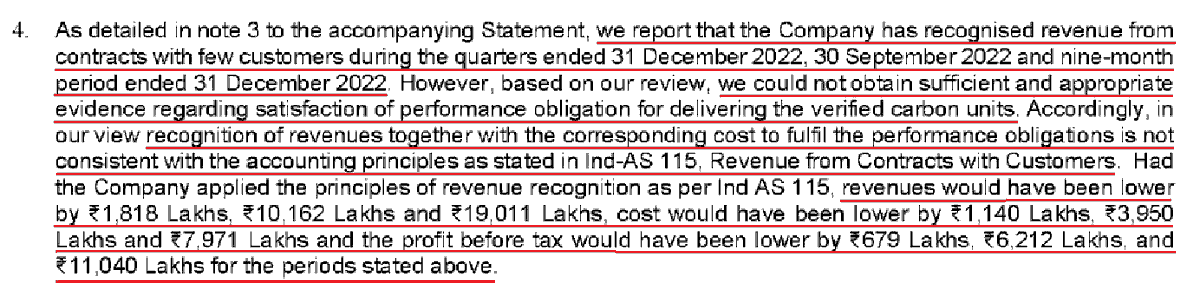

Generally don't write about IPOs, but reading a new Red Herring Prospectus is habit. India Pesticides is an agro-chemical company with seemingly mouth-watering financial ratios. But corporate governance markers suggest extreme caution. (1/n)

What set off this inquiry was a disclosure in the RHP, indicating that the Company issued shares at Rs 33.70 to two individuals in February 2021 (4 months ago), who are related to a director. The IPO has recently closed with 23x subscription at Rs 295 per share. (2/n)

These two individuals were collectively alloted 371,380 shares for a consideration of approx Rs 1.25 crore, which would be worth close to Rs 11 crore after the IPO. That's a 775% increase in 4 months or 40,152% ROI annualized, assuming listing date as 05 July. (3/n)

The allottees are owners of a firm that is 'advisor to the offer' in the draft RHP but the reference is omitted in the final RHP. However, they were issued shares at 87% discount 4 months ago, which seems to indicate lack of transparency on the quid pro quo at play here. (4/n)

It is necessary to ask what role did the 'advisor' play in determining the IPO price? Why did the company allot shares at just 3x price-to-earnings barely months before the IPO? Is there a valuation report for the placement? What kind of valuation methodology was adopted? (5/n)

Section 62(1)(c) of the Companies Act and the rules thereunder require preferential issue to third parties to be accompanied by a valuation report from a registered valuer under the Act. This report would have determined the fair value of the shares to be at *least* Rs 33. (6/n)

It seems odd that the registered valuer justified Rs 33 price in February 2021 as fair value when barely 4 months later the Company is justifying its 25x price-to-earnings in comparison with its listed peers. The listed peers existed 4 months ago too. (7/n)

Either the fair value of Rs 33.70 in February 2021 was understated or the IPO price of Rs 275 in June 2021 is inflated. This is a good example why SEBI should mandate disclosure of valuation reports for all preferential allotments in the 12 months leading to the IPO. (8/n)

Questions naturally arise on other details in the RHP. Between Oct 2020 and Feb 2021, the Company saw complete overhaul of the Board. 2 directors joined the board in Dec 2020 and resigned in Feb 2021. One of them is a noted securities lawyer. Why this musical chairs? (9/n)

CEO and CFO are paid peanuts even after having been employees for decades. A 3000 crore market cap company with Rs 700 crore sales upon listing, and the CEO/CFO are cumulatively paid Rs 22 lakh a year. They also have no equity stake in the company. (10/n)

Further, the 800 crore IPO is primarily an offer for sale (700 crore) by the promoters and 80 crore fresh issue of shares (20 crore is likely for 'general corporate purposes'. What does the company get? Working capital. The Company will NOT use the capital for growth.(11/n)

The reason why is apparent from the fact that the Company has already expanded the capacity of high-mergin technical APIs from 10,000 MT in 2019 to 19,500 MT in 2021. While capacity utilization is down from 80% to 75%, EBIDTA margins are up from 21% to 29%. (12/n)

While decreased utilization after expansion is not abnormal, the receivables and inventory have also been increasing, putting pressure on cash flows. Less than 50% of PBT was converted into cash from operations in 2021. Further, lot of receivables are > 90 days old. (13/n)

Other red flags in the RHP - the Company hasn't specified exact address of their plants/factories, only a general locality given. At the same time, company has transactions with promoter entities in related businesses, who are located in the same locality. (14/n)

Company has many litigations for allegedly misbranding its products, and also for environmental issues. The Company's logo is not trademarked and under dispute. Also, 2 family members were paid Rs 1.2 crore in 'professional fees' in 2021, but CEO/CFO paid only Rs 22 lakh. (15/n)

The Company claims to be an R&D driven organization, but its R&D expenditure can only be summarized as a rounding error. Also, the R&D facility is leased from a promoter entity. (16/n)

Overall, India Pesticides has some major issues. Strange allotments to outsiders gifting 775% gains in 4 months. All KMPs and directors installed in last 9 months. CEO/CFO paid peanuts. Negligible R&D spend. Massive capex. Increasing receivables. Declining cash flows. (17/n)

Personally, I find more red flags here than the annual meeting of the Chinese CPC. As always, this is an educational exercise and not a basis for investment or trading decision. (18/n)

2 3

2 3

Hat tip to @GhanishtNagpal for helping immensely with merchant banking norms on preparation of these documents..

• • •

Missing some Tweet in this thread? You can try to

force a refresh