DIY investor, lawyer - writing on corporate governance - and reading between the lines.

If state wishes to promote domestic manufacturing, it can put tariff controls like it does for solar modules. If it wishes to promote better quality, it puts standards and BIS enforces them. BIS does not 'promote domestic manufacturing'; its function is quite different.

If state wishes to promote domestic manufacturing, it can put tariff controls like it does for solar modules. If it wishes to promote better quality, it puts standards and BIS enforces them. BIS does not 'promote domestic manufacturing'; its function is quite different.

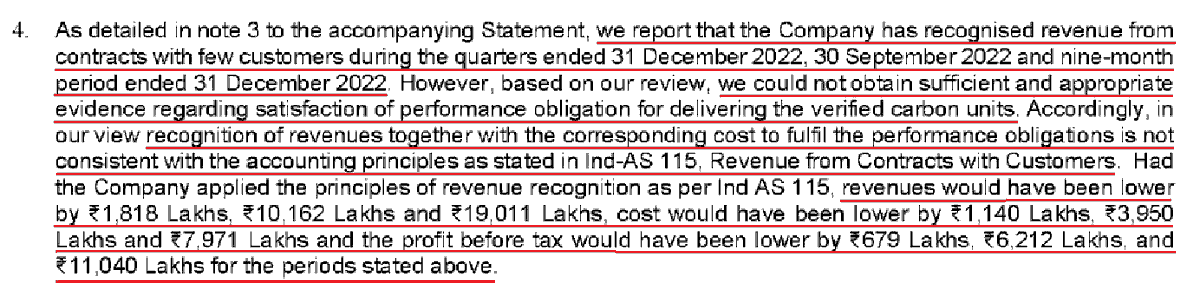

Management has recognised revenue, AGAINST opinion of auditor, in absence of fulfillment of contractual performance obligations!

Management has recognised revenue, AGAINST opinion of auditor, in absence of fulfillment of contractual performance obligations!

Promoters justify 12% stake sale in AGL for investment into a related entity Adicon Ceramica LLP, where they state they have no holding. Weak argument, because business is intertwined and a designated partner of the LLP is a director in all material subsidiaries of AGL. (2/7)

Promoters justify 12% stake sale in AGL for investment into a related entity Adicon Ceramica LLP, where they state they have no holding. Weak argument, because business is intertwined and a designated partner of the LLP is a director in all material subsidiaries of AGL. (2/7)