Sugar Industry: Decoding the major trend in Sugar Industry & Understanding the Filters to seize the good companies in this cyclical industry.

Retweet for maximum reach to spread knowledge. 🙏🙏

🧵👇

Retweet for maximum reach to spread knowledge. 🙏🙏

🧵👇

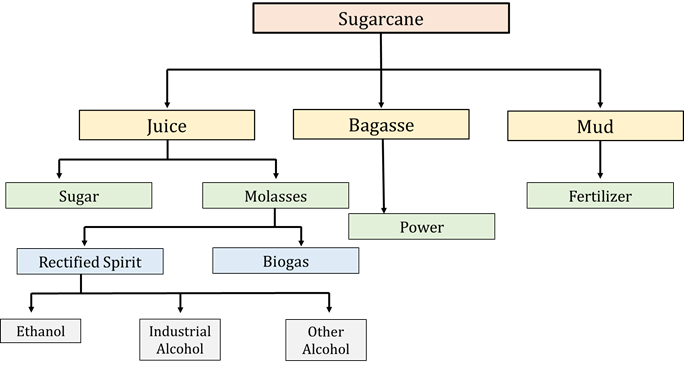

How Sugar is Made?

- Sugar is mainly made from sugarcane, of which 20% is made from Sugar Beans.

- Depending on variety & sowing time, growing cycle of sugarcane is 1-1.5 years. As the cane grows, it is sent to mills for processing.

- Sugar is mainly made from sugarcane, of which 20% is made from Sugar Beans.

- Depending on variety & sowing time, growing cycle of sugarcane is 1-1.5 years. As the cane grows, it is sent to mills for processing.

Sugar in India is sourced from third party. In the mills, sugar is first crushed in "Roller", where Juice, Bagasse & Mud is separated

- From the crushed mixture, Bagasse is separated & burned in boiler which produces energy (internally consumed). Mud is used in biogas fertilizer

- From the crushed mixture, Bagasse is separated & burned in boiler which produces energy (internally consumed). Mud is used in biogas fertilizer

- Juice is then taken for processing & heated to make syrup

- There are different stages of boiling Sugarcane Juice. Post boiling residual is left which is known as Molasses. It is used in distillery, and is further used for Ethanol & Alcohol. Ethanol can also be made from juice

- There are different stages of boiling Sugarcane Juice. Post boiling residual is left which is known as Molasses. It is used in distillery, and is further used for Ethanol & Alcohol. Ethanol can also be made from juice

Sugar comes in 3 forms:

1. Large (L) Crystals

2. Medium (M) Crystal

3. Small (S) Crystal

M & S Crystals forms about 80% of production. The shelf life of sugar is 3 year.

- The process of sugar manufacturing is 300 year old and there has been no innovation in this process.

1. Large (L) Crystals

2. Medium (M) Crystal

3. Small (S) Crystal

M & S Crystals forms about 80% of production. The shelf life of sugar is 3 year.

- The process of sugar manufacturing is 300 year old and there has been no innovation in this process.

Molasses are of different types of boiling.

A. C-Heavy Molasses: 3 Times of Boiling of Sugarcane Juice is C-Heavy Molasses. Content:

1 Ton of Sugar= 9.5-13% Sugar + 4-5% Molasses + 30% Bagasse + Rest Water)

A. C-Heavy Molasses: 3 Times of Boiling of Sugarcane Juice is C-Heavy Molasses. Content:

1 Ton of Sugar= 9.5-13% Sugar + 4-5% Molasses + 30% Bagasse + Rest Water)

B. 2 Times of Boiling of Sugarcane Juice.

(Content- 1 Ton of Sugar= 9.5-13% Sugar + 4-5% Molasses + 30% Bagasse + Rest Water)

(Content- 1 Ton of Sugar= 9.5-13% Sugar + 4-5% Molasses + 30% Bagasse + Rest Water)

About Industry:

- In India there are about 752 Installed sugar factories, with a crushing capacity of 339 Lakh MT.

1. 330 Co-operative units

2. 379 Private Factories

3. 43 Public Factories

- In India there are about 752 Installed sugar factories, with a crushing capacity of 339 Lakh MT.

1. 330 Co-operative units

2. 379 Private Factories

3. 43 Public Factories

- Sugar cycle is roughly of 5 years. 3-4 year of overproduction, followed by a year or two of lower production.

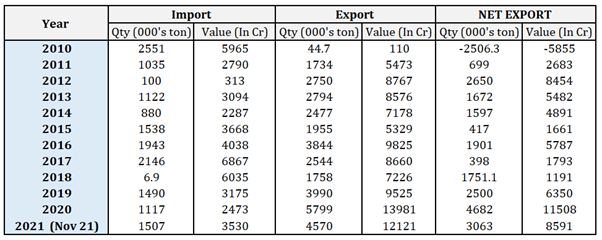

Import Export Data of Sugar of India.

Import Export Data of Sugar of India.

Farmers Favourable Crop:

- Farmers prefer growing sugarcane, because of higher rate of return (60-70%).While the farmers are paid full promised price. There is no middleman in this crop, like that of others, hence the repayment schedule is of shorter tenure as well.

- Farmers prefer growing sugarcane, because of higher rate of return (60-70%).While the farmers are paid full promised price. There is no middleman in this crop, like that of others, hence the repayment schedule is of shorter tenure as well.

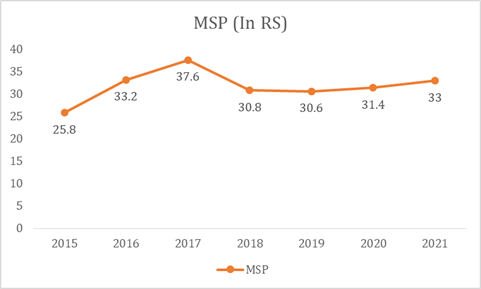

Pricing of Sugarcane: Govt. over year have brought many new reforms

1. Minimum Selling Price (MSP):

Minimum Price which FCI (Food Corporation of India) sets for sugar mills to sell sugarcane (protecting downside risk). This was temporarily brought to stabilize the price of sugar

1. Minimum Selling Price (MSP):

Minimum Price which FCI (Food Corporation of India) sets for sugar mills to sell sugarcane (protecting downside risk). This was temporarily brought to stabilize the price of sugar

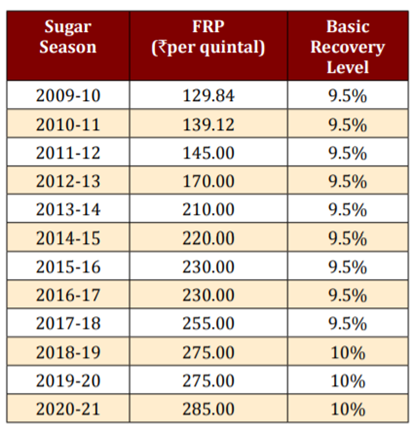

2. Fair Remunerative Price (FRP):

Minimum price to be paid by sugar mills to the farmers. In case, sugar mills having exceptional profit, such profits shall also be shared with the farmers.

Minimum price to be paid by sugar mills to the farmers. In case, sugar mills having exceptional profit, such profits shall also be shared with the farmers.

3. State Advisory Price (SAP): Some states charge additional costs higher than FRP, to their state mills. However in the past few years this has barely changed.

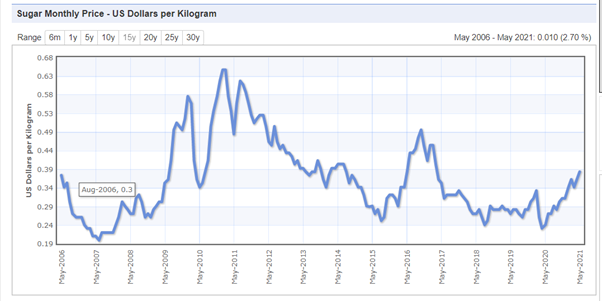

Price Trend of sugar:

- Recently sugar has touched an All Time High price of the last 5 year. In the month of March there had been a decline in the international price of sugar, temporarily but then again went all time high.

- Recently sugar has touched an All Time High price of the last 5 year. In the month of March there had been a decline in the international price of sugar, temporarily but then again went all time high.

Key Drivers of Industry:

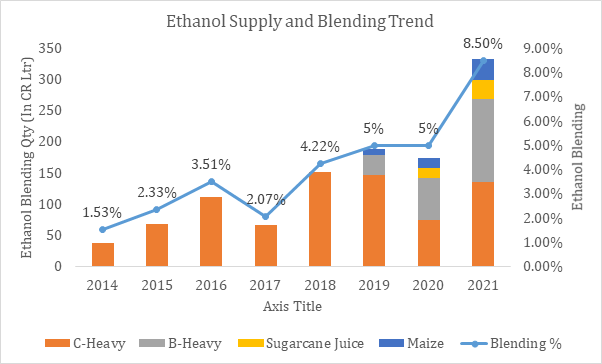

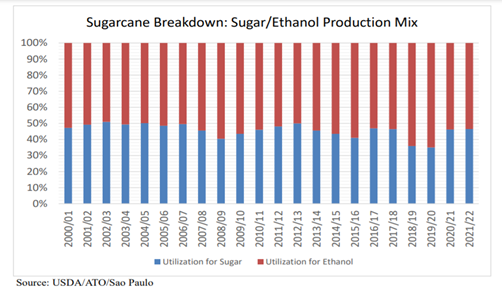

1. Ethanol Blending Policy:

- Over the years the Ethanol Blending trend has been shifting and sugar companies are shifting more towards B-Molasses, instead of C-Heavy Molasses.

(Detail Thread on Ethanol Blending Policy coming tomorrow)

1. Ethanol Blending Policy:

- Over the years the Ethanol Blending trend has been shifting and sugar companies are shifting more towards B-Molasses, instead of C-Heavy Molasses.

(Detail Thread on Ethanol Blending Policy coming tomorrow)

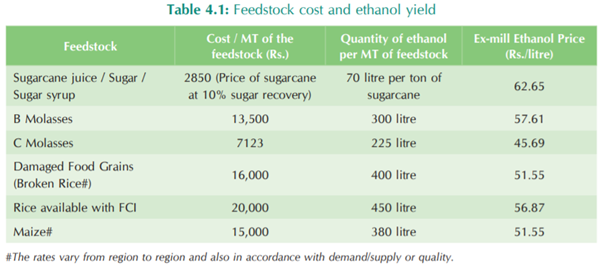

- Ethanol from sugar is much more profitable for the companies. Currently the price of sugar is ~Rs33. Price of B-Molasses is around Rs57.61 and the price of C-Molasses is Rs 45.7. Hence there is additional margin of Rs 24 and Rs 13 in B & C Molasses respectively.

- 1 Tonne of sugarcane produces 11% of sugar (110 Kg). If converted directly into ethanol, 70 Litre (7%) of ethanol is produced. Hence with 1.6 times higher price than sugar will yield more return in Ethanol.

- Producing Ethanol is much more profitable.

- Producing Ethanol is much more profitable.

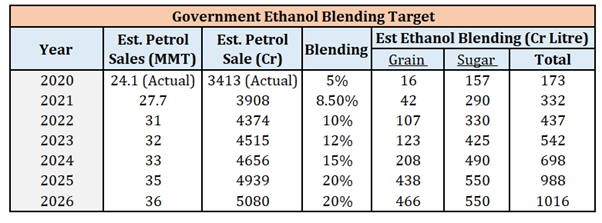

2. Government Push:

Government has recently initiated the National BioFuel Policy, where they are aiming to reduce import on petroleum products. Ethanol blending target increased from 10% to 20%.

Government has recently initiated the National BioFuel Policy, where they are aiming to reduce import on petroleum products. Ethanol blending target increased from 10% to 20%.

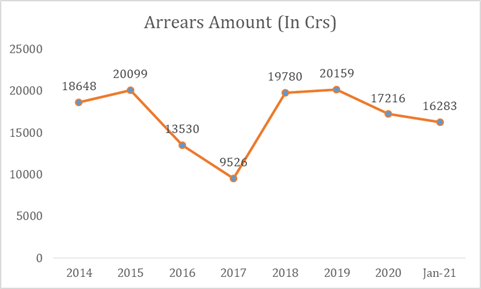

3. Decrease in Arrears:

Sugar mills have to pay to the farmers within 15 days. If there is a delay in payment then they are liable to pay an interest of ~18% per annum.

With upturn in cycle, arrears (liability of sugar mills) are constantly declining.

Sugar mills have to pay to the farmers within 15 days. If there is a delay in payment then they are liable to pay an interest of ~18% per annum.

With upturn in cycle, arrears (liability of sugar mills) are constantly declining.

- The Receivable cycle in ethanol is much lower than that of sugar. Hence it results in decrease of Working Capital.

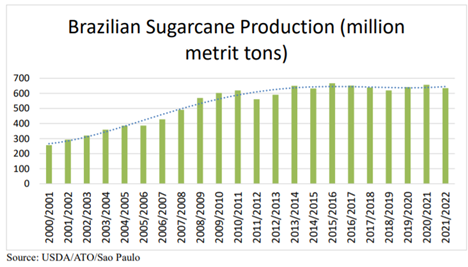

4. Drought in Brazil & Thailand

- Brazil is the largest sugar exporter. Brazil revenue from production of sugar & ethanol is 50:50.

- Recently, Brazil has been facing a severe Drought than that of the past year. It has reduced the total production of sugar.

- Brazil is the largest sugar exporter. Brazil revenue from production of sugar & ethanol is 50:50.

- Recently, Brazil has been facing a severe Drought than that of the past year. It has reduced the total production of sugar.

- Advantage in producing Ethanol in India has led to shift in production from sugar to ethanol in India. This may exceed the demand of sugar than the supply in the market. Hence there is also the probability of increase in sugar price.

Thailand:

- Thailand is the 2nd largest exporter. Monsoon this year in Thailand has remain bad. Expectation of production fall would be around 7-8MT

- Usually, a significant impact on production happens in the 2nd year of drought. Hence this may turn good for Indian sugar mills.

- Thailand is the 2nd largest exporter. Monsoon this year in Thailand has remain bad. Expectation of production fall would be around 7-8MT

- Usually, a significant impact on production happens in the 2nd year of drought. Hence this may turn good for Indian sugar mills.

5. Adoption of Innovative Seed

Previously seeds in UP were of low quality leading to lower production than other regions. However adoption of CO-0238 seed (since 2016) has improved the production, leading to 40% increase in production.

Previously seeds in UP were of low quality leading to lower production than other regions. However adoption of CO-0238 seed (since 2016) has improved the production, leading to 40% increase in production.

6. Government measure on increase in the rate of Ethanol price, has led to Structurize the demand – supply gap in India. However, currently, there is a subsidy on the production of petrol from ethanol, as the price of petrol from ethanol turned out to be ~Rs75.

- Over the years, there has been a steady increase in demand supply gap of sugar, leading to unsustainability of margin. While Working Capital remains the major issue (Payment to farmers in 15 days and receivable of sugar take a year). Ethanol facility will remove this problem.

Will the Sugar industry shift to structural from cyclical?

1. Brazil has ~50% Ethanol blending. But over the past, they couldn’t able to Structurize the industry.

2. Production problems in Brazil will remain a short term event, post which, the price of sugar can again fluctuate

1. Brazil has ~50% Ethanol blending. But over the past, they couldn’t able to Structurize the industry.

2. Production problems in Brazil will remain a short term event, post which, the price of sugar can again fluctuate

3. Price sustainability of Ethanol remains a question as govt. has to bear its revenue from petrol when produced from Ethanol due to subsidies involved.

4. Every Co. in India is increasing their capacity of sugar production. Due to this Supply can exceed resulting in cyclicality

4. Every Co. in India is increasing their capacity of sugar production. Due to this Supply can exceed resulting in cyclicality

Hence shift of industry to structural theme seems difficult. However with the recent demand, this time cycle can be a bit bigger cycle for Indian sugar players.

However with the current trend, atleast the industry seems to be safe for the coming few periods. But as a significant part of this cycle is already done, one has to cautiously enter this industry. Here are key parameters to look at in this industry.

Filters:

1. Average Capacity Utilization of Company

2. Yield per Tonne. Higher the yield will have higher margin

3. Ethanol facility per tonne of cane crush.

4. D/E of the company. (Higher D/E will have priority of debt repayment first. Hence there is no scope for dividend)

1. Average Capacity Utilization of Company

2. Yield per Tonne. Higher the yield will have higher margin

3. Ethanol facility per tonne of cane crush.

4. D/E of the company. (Higher D/E will have priority of debt repayment first. Hence there is no scope for dividend)

5. Higher Production facility with optimum utilization. (Game is more towards increasing margin with little increase in sales). Hence higher utilization will churn profits early.

6. Uttar Pradesh is rich with river water, while production over past years has increased a lot in UP province. In the worst case lower rain water availability would be managed in UP, leading to sugarcane consistent supply.

Sources:

Special Thanks to Anil Goel sir, @varindarbansal sir for arranging a detail video from the experts.

Data from Niti Aayog, Indian Sugar Association, Value Pickr, FAO & World Sugar Market, KPMG, Crops Production Report.

Special Thanks to Anil Goel sir, @varindarbansal sir for arranging a detail video from the experts.

Data from Niti Aayog, Indian Sugar Association, Value Pickr, FAO & World Sugar Market, KPMG, Crops Production Report.

These companies are already in our radar.

Disclosure: We are already invested in Dwarikesh Sugar and Magadh Sugar. Please do your own analysis before investing in the stock. 😀

Disclosure: We are already invested in Dwarikesh Sugar and Magadh Sugar. Please do your own analysis before investing in the stock. 😀

https://twitter.com/tycoonmindset05/status/1404220958693490696?s=19

Adding Few viable sources to track updates on Sugar Industry:

- ISMA- Indian Sugar Mills Association: (indiansugar.com)

- DFPD- Dept. of Food and Public Distriibution

(dfpd.gov.in/sugar_C.htm)

- ISMA- Indian Sugar Mills Association: (indiansugar.com)

- DFPD- Dept. of Food and Public Distriibution

(dfpd.gov.in/sugar_C.htm)

Recent Press Release by ISMA- indiansugar.com/EventDetails.a…

Notable Points:

1 Cane Area Increment

- UP expected to have same of last year

- Maharashtra higher by 11%

- Karnataka higher by 4%

2 Rain is good. Estimated sugar production is ~121.3 LacTons (without diversion of ethanol)

Notable Points:

1 Cane Area Increment

- UP expected to have same of last year

- Maharashtra higher by 11%

- Karnataka higher by 4%

2 Rain is good. Estimated sugar production is ~121.3 LacTons (without diversion of ethanol)

3. Contraction quantity of Ethanol as on 5th July: 333cr Litre.

- B-Heavy expected to be 230cr Litre (Diversion of around 21 lakh tonnes of sugar into ethanol)

- 34 Lakh tonne to be diverted in next year for 10% ethanol blending target.

- B-Heavy expected to be 230cr Litre (Diversion of around 21 lakh tonnes of sugar into ethanol)

- 34 Lakh tonne to be diverted in next year for 10% ethanol blending target.

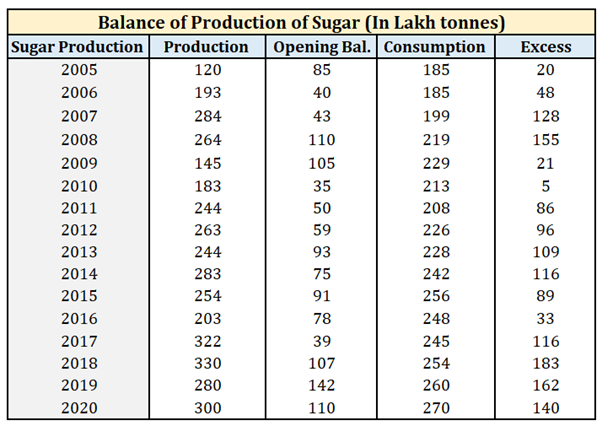

4. Production data (In Lakh Tons)

- Opening Balance (Oct 2020): 107

- Production (2020-21): 309

- Domestic / Export: 260 : 70

- Est. Opening Stock Oct (2021): 87

- Opening Balance (Oct 2020): 107

- Production (2020-21): 309

- Domestic / Export: 260 : 70

- Est. Opening Stock Oct (2021): 87

• • •

Missing some Tweet in this thread? You can try to

force a refresh