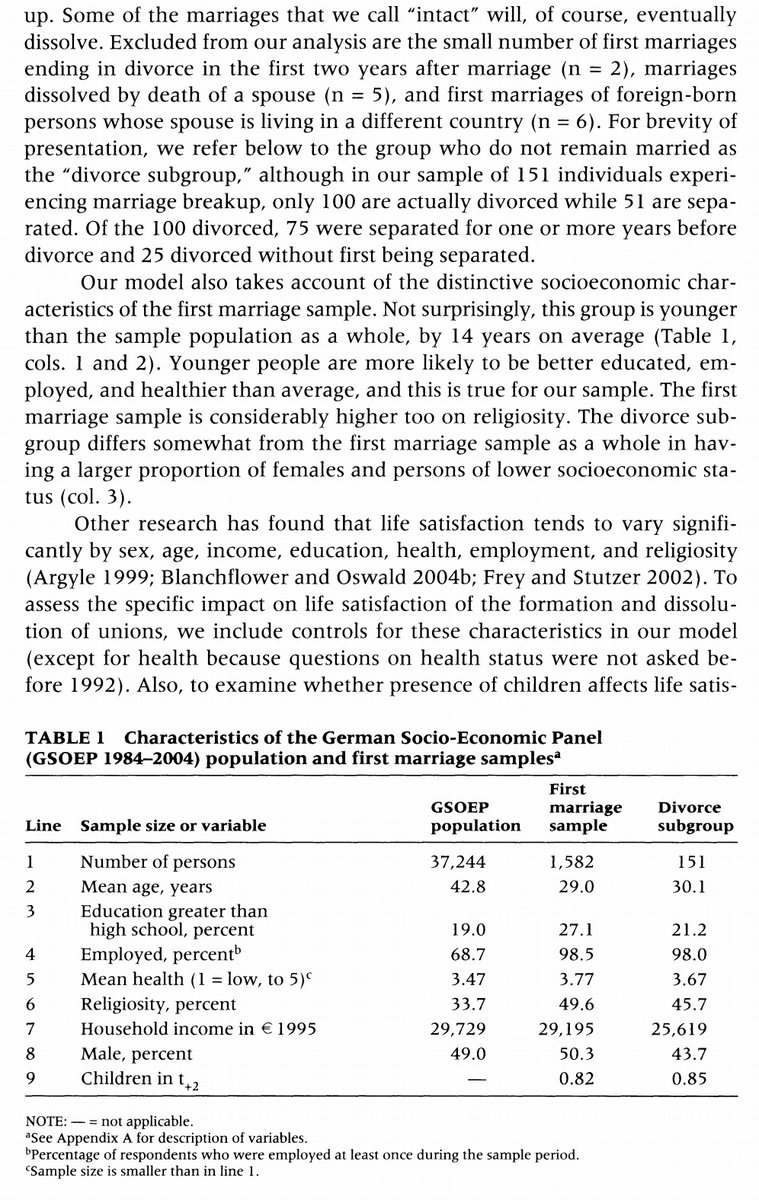

1/ Mapping Investable Return Sources to Macro Environments (AQR)

"Style premia have less macro exposure than do asset classes. Additionally, a diversified portfolio (for asset classes and style premia) may rely less on a specific macroeconomic outcome."

aqr.com/Insights/Resea…

"Style premia have less macro exposure than do asset classes. Additionally, a diversified portfolio (for asset classes and style premia) may rely less on a specific macroeconomic outcome."

aqr.com/Insights/Resea…

2/ "We must stress the limitations of this type of analysis. Any empirical result is specific to the sample period (here 1972-2013) and dependent on design choices.

"Long/short returns are scaled to target 10% annual volatility. We subtract no trading costs or fees."

"Long/short returns are scaled to target 10% annual volatility. We subtract no trading costs or fees."

3/ "The weak relation between equities & growth reflects the forward-looking nature of equity returns. The correlation between annual equity returns & our contemporaneous (*next* year's) growth indicator is 0.24 (0.50).

"Styles were positive in both up and down

environments."

"Styles were positive in both up and down

environments."

4/ "The distinction between simple & partial correlations is the same as that between slope coefficients in simple & multiple regressions.

"It is difficult to find an asset class or even a style that performs well in a stagflationary (growth-down, inflation-up) environment."

"It is difficult to find an asset class or even a style that performs well in a stagflationary (growth-down, inflation-up) environment."

5/ "Again, results might be specific to this sample or our specifications of style premia and macro environments.

"Even L/S styles can be more market-directional in certain asset classes (e.g. currency carry) than in the broadly diversified style composites we analyze here."

"Even L/S styles can be more market-directional in certain asset classes (e.g. currency carry) than in the broadly diversified style composites we analyze here."

6/ "It is difficult to populate the upper-left quadrant on the risk graphs, with rising real yields, inflation, volatility and illiquidity all posing a challenging environment – all compounded by negative growth.

"Style premia tend to be closer to the origin in all four graphs."

"Style premia tend to be closer to the origin in all four graphs."

7/ "The relationships we document are not predictive and thus less useful for tactical decisions than strategic ones.

"As post-WWII history is characterized by broadly benign growth and inflation, investors may have grown to consider equity-friendly conditions too complacently."

"As post-WWII history is characterized by broadly benign growth and inflation, investors may have grown to consider equity-friendly conditions too complacently."

8/ Related reading:

Rate of Return on Everything

Strategic Allocation to Commodity Factor Premiums

Best Strategies for Inflationary Times

Can Risk Parity Outperform If Yields Rise?

Rate of Return on Everything

https://twitter.com/ReformedTrader/status/1259274241515483136

Strategic Allocation to Commodity Factor Premiums

https://twitter.com/ReformedTrader/status/1204964215120809985

Best Strategies for Inflationary Times

https://twitter.com/ReformedTrader/status/1379188472750071809

Can Risk Parity Outperform If Yields Rise?

https://twitter.com/ReformedTrader/status/1337205904932945921

• • •

Missing some Tweet in this thread? You can try to

force a refresh