0/ Leading FinTech co's are seeing CAC decrease as they scale.

$SQ finished '20 w/ a CAC <$5 & 36M MAUS (up from 24M in '19) while $HOOD saw CAC hit $15 in 1Q21 down from $20 for '20, $32 in 1Q20 & $53 in '19 w/ 18M accounts in 1Q21 up from 12.5M, 7.2M & 5.1M respectively

$SQ finished '20 w/ a CAC <$5 & 36M MAUS (up from 24M in '19) while $HOOD saw CAC hit $15 in 1Q21 down from $20 for '20, $32 in 1Q20 & $53 in '19 w/ 18M accounts in 1Q21 up from 12.5M, 7.2M & 5.1M respectively

1/ These customer bases are starting to surpass incumbents: E.g., $BAC has 39.3M "digital users" (12.9M Zelle) while $JPM has 63.4M households, 55.3M digital / 40.9M mobile customers

$SCHW has 32M active broker accounts with $7.4T in clients assets & $IBKR at 1.4M /$363B

$SCHW has 32M active broker accounts with $7.4T in clients assets & $IBKR at 1.4M /$363B

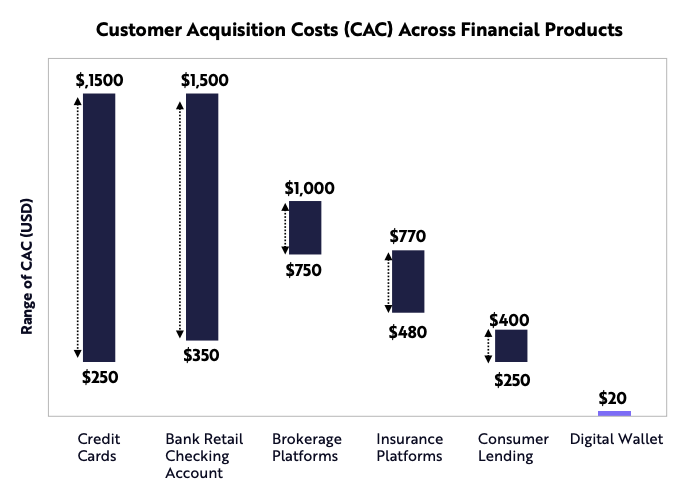

2/ The CAC associated with legacy broker accounts has ranged from ~$750-$1,000 while bank accounts ranged considerably from ~$350-$1,500 per @ARKInvest

3/ While the FinTech firms are still sub-scale relative to incumbents (e.g., $HOOD avg account size is ~$4,500 compared to $IBKR of $260K or $SCHW of $233K both apples to oranges given the prominence of RIA's on the platform) the early cohort / demographic data is promising

4/ Ultimately as more FinTech co's come public we'll need to see valuation metrics converge b/w legacy fin service companies & their more modern peers.

One of the biggest differences thus far is on the cost structure which should remain an advantage lower CAC & lower bloat

One of the biggest differences thus far is on the cost structure which should remain an advantage lower CAC & lower bloat

5/ They'll need to show the ability to continue to grow monetization to start to equate to that of incumbent peers b.c incumbents like $JPM & $GS continue to invest in / acquire FinTech co's as have other smaller players such as $FITB, $PNC, $SIVB, $SIGN, etc...

6/ The digital banks seem to have the toughest comps as they are the furthest behind on monetization given the lack of balance sheet / cost of capital / no formal charters & reliance on Durbin exemption

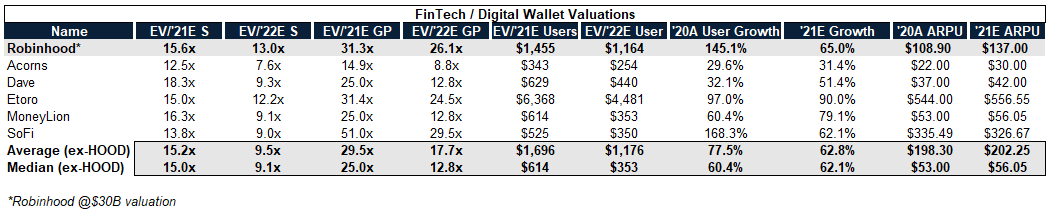

7/ Looking at some of the FinTech co's that have come public via SPAC or IPO they are being valued ~15.0x / 9.5x '21E / '22E EV/S and 29.5x / 17.7x '21E / '22E GP well in excess of incumbents.

• • •

Missing some Tweet in this thread? You can try to

force a refresh