Tom Russo's thesis on $BABA

"Alibaba’s management team enjoys the “capacity to suffer”

as the result of protection from Wall Street’s disruptive censures as a result of protection provided them by Alibaba’s founding shareholder, Jack Ma."

"Alibaba’s management team enjoys the “capacity to suffer”

as the result of protection from Wall Street’s disruptive censures as a result of protection provided them by Alibaba’s founding shareholder, Jack Ma."

Alibaba network is deeply ingrained with commerce.

"With roughly one billion Chinese average annual consumers and roughly 260 million additional consumers outside of China, it is hard to imagine shopping in China without involvement in one manner or another with Alibaba."

"With roughly one billion Chinese average annual consumers and roughly 260 million additional consumers outside of China, it is hard to imagine shopping in China without involvement in one manner or another with Alibaba."

Alibaba is well capitalized with rock-solid balance sheet.

$71 billion in cash & equivalent.

Investments in over 100 disruptive start-ups.

Over 30% interest in Ant Financial.

$71 billion in cash & equivalent.

Investments in over 100 disruptive start-ups.

Over 30% interest in Ant Financial.

Valuation is modest, at a multiple of EV/EBITA of 10x.

Position sized to 2.5% to 3% due to regulatory risks that may cripple Alibaba's competitive moats.

Position sized to 2.5% to 3% due to regulatory risks that may cripple Alibaba's competitive moats.

Russo seeks to invest in companies with multiple business gems.

Particularly if the company's services are the only way that consumers can obtain such goods or services.

$BABA businesses provide brands & products that consumers can't do without and could only obtain via $BABA

Particularly if the company's services are the only way that consumers can obtain such goods or services.

$BABA businesses provide brands & products that consumers can't do without and could only obtain via $BABA

Russo deems that it is more probable that China would recognize that they needed the Western-style, modern retail, and a robust innovation pipeline.

He did not anticipate the pace and appetite of regulatory declarations and investigations since his initial position in 2020.

He did not anticipate the pace and appetite of regulatory declarations and investigations since his initial position in 2020.

Russo referred to China's recent move as "disinfectants" to combat risks that have arisen over decades of business misconduct.

How the disinfectant may lead to healthier business practices:

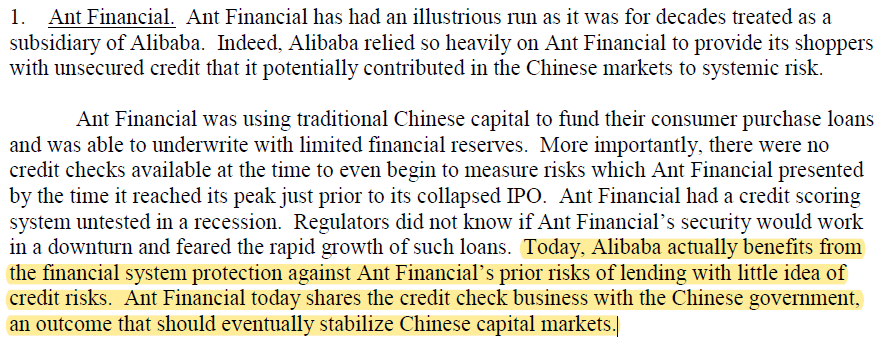

1. Ant Financial 🐜

How the disinfectant may lead to healthier business practices:

1. Ant Financial 🐜

2. Data Security 💻

3. Below Cost Pricing 🛒

4. Future Technology 🤖

5. No More "Choose One from Two" 🏪

6. Increase War on Counterfeit

7. Academic Expectations

All-in-all, Russo believes these "disinfectants" will strengthen $BABA position over time.

Despite what the headlines and share price may imply.

Despite what the headlines and share price may imply.

Summary of Russo's bull thesis 🐂

Alibaba has been buying back shares at an attractive valuation.

Expecting strong growth from cloud and core commerce business.

• • •

Missing some Tweet in this thread? You can try to

force a refresh