Fineotex Chemical Ltd ( My Observation ,no recommendations )

Market Cap 1,232 Cr.

Current Price 111

High / Low 120 / 29.2

Book Value 18.9

Promotors holding-around 65% ( In Last 3 yrs from 72.36 to 64.72 and last few month 64.72 to 64.82)

Market Cap 1,232 Cr.

Current Price 111

High / Low 120 / 29.2

Book Value 18.9

Promotors holding-around 65% ( In Last 3 yrs from 72.36 to 64.72 and last few month 64.72 to 64.82)

-OPM betwee 18-19% ( consolidated )in last 3-4 yrs

standalone between 20-25%

-sales growth last 3 yrs 16% and profit growth 23%

- Almost debt free

- High debtor days

-Good ROCE and ROE

EBITDA Margins - Company is hopeful for maintaining margins of 18-19%

standalone between 20-25%

-sales growth last 3 yrs 16% and profit growth 23%

- Almost debt free

- High debtor days

-Good ROCE and ROE

EBITDA Margins - Company is hopeful for maintaining margins of 18-19%

-Manufacturing ,JV and R&D

1- Navi Mumbai- Capacity 36000 MT

2 Malaysia -6500 MT

3- Upcoming- Ambernath facility - 36000 TPA

1- Navi Mumbai- Capacity 36000 MT

2 Malaysia -6500 MT

3- Upcoming- Ambernath facility - 36000 TPA

4-JV with HealthGuard Australia for durable metal-free sustainable chemistry solutions that are anti-microbial and anti-viral(textile,detergent, leather and allied products)

5-Sasmira-Setting up a state of art Research & Development centre in collaboration with Sasmira Institute, one of India’s premier textile institutes

-Fy 21 R&D expenses 1.85 cr with top line of 219 cr ( I hope after Sasmira Tie up R&D will be much better

-Fy 21 R&D expenses 1.85 cr with top line of 219 cr ( I hope after Sasmira Tie up R&D will be much better

The capacities for the company are fungible across segments and products. This has resulted in better revenue generation on every unit of investment. Additionally, the investment required to put up additional capacities is low for the company and this has supported the strong

RoCE at 21-22% and asset turnover of more than 5 times over the past few years

Business Segment -

- Textile ( Major Revenue)

- Home Care and Hygiene( Recent Entry )

- Drilling ( Recent entry)

-Other Specialities

Business Segment -

- Textile ( Major Revenue)

- Home Care and Hygiene( Recent Entry )

- Drilling ( Recent entry)

-Other Specialities

-Speciality textiles - FCL manufactures chemicals for entire valve chain in textile segment from weaving to finishing.

- Major Customer ( See Below)

- Major Customer ( See Below)

Sales in 60+ countries including Brazil, Bangladesh, Germany, Indonesia, Malaysia, Singapore, Syria, Thailand, USA, Venezuela and Vietnam

-Revenue mix ( FY 21) 57% international 43% india

-Revenue mix ( FY 21) 57% international 43% india

Aquastrike VCF–( Product developed by Malaysian subsidiary ) waiting for WHO Approval since last 3 yrs ( Not sure whether they will get approval or not but its a interesting product )

It is a non toxic, non polluting, Eco-friendly solution, produced

It is a non toxic, non polluting, Eco-friendly solution, produced

• Simply poured on the water surface at a rate of 1ml per square meter, the silicon based

liquid forms a molecule thick film, that doesn't stop water oxygenation (so no effect on fish, worms, snails and vegetals) but alter the water surface tension

liquid forms a molecule thick film, that doesn't stop water oxygenation (so no effect on fish, worms, snails and vegetals) but alter the water surface tension

. As a result, larvae and pupae are unable to attach their breathing syphon and end up drowning.

• The adult mosquitoes while trying to lay eggs on the surface of the water, drown because of the lower surface tension.

• The adult mosquitoes while trying to lay eggs on the surface of the water, drown because of the lower surface tension.

• It doesn't kill the mosquitoes by poisoning. Aquastrike effect is physical not chemical,

which eliminates the risk of mosquito developing immunity to the product as it is the case

with some insecticides or even BTI.

which eliminates the risk of mosquito developing immunity to the product as it is the case

with some insecticides or even BTI.

Risk -

1- Big European competitors

Clariant ( Archroma)

Huntsman

Woodolf

CHT

Woolera

ICI Croda

2-Sebi Fined Promotors for IPO case

3- Many family transections ( Probably to save Tax) Read article by Dr Vijay Malik for Details .

1- Big European competitors

Clariant ( Archroma)

Huntsman

Woodolf

CHT

Woolera

ICI Croda

2-Sebi Fined Promotors for IPO case

3- Many family transections ( Probably to save Tax) Read article by Dr Vijay Malik for Details .

Why I bought shares of FCL

1- New capacity in coming up

2- Tie Up with Health Guard Australia for products

3- Growth in Textile industry

4- Recent entry in Home care and Hygiene Products

5- R&D will be better with SASMIRA tie-up.

1- New capacity in coming up

2- Tie Up with Health Guard Australia for products

3- Growth in Textile industry

4- Recent entry in Home care and Hygiene Products

5- R&D will be better with SASMIRA tie-up.

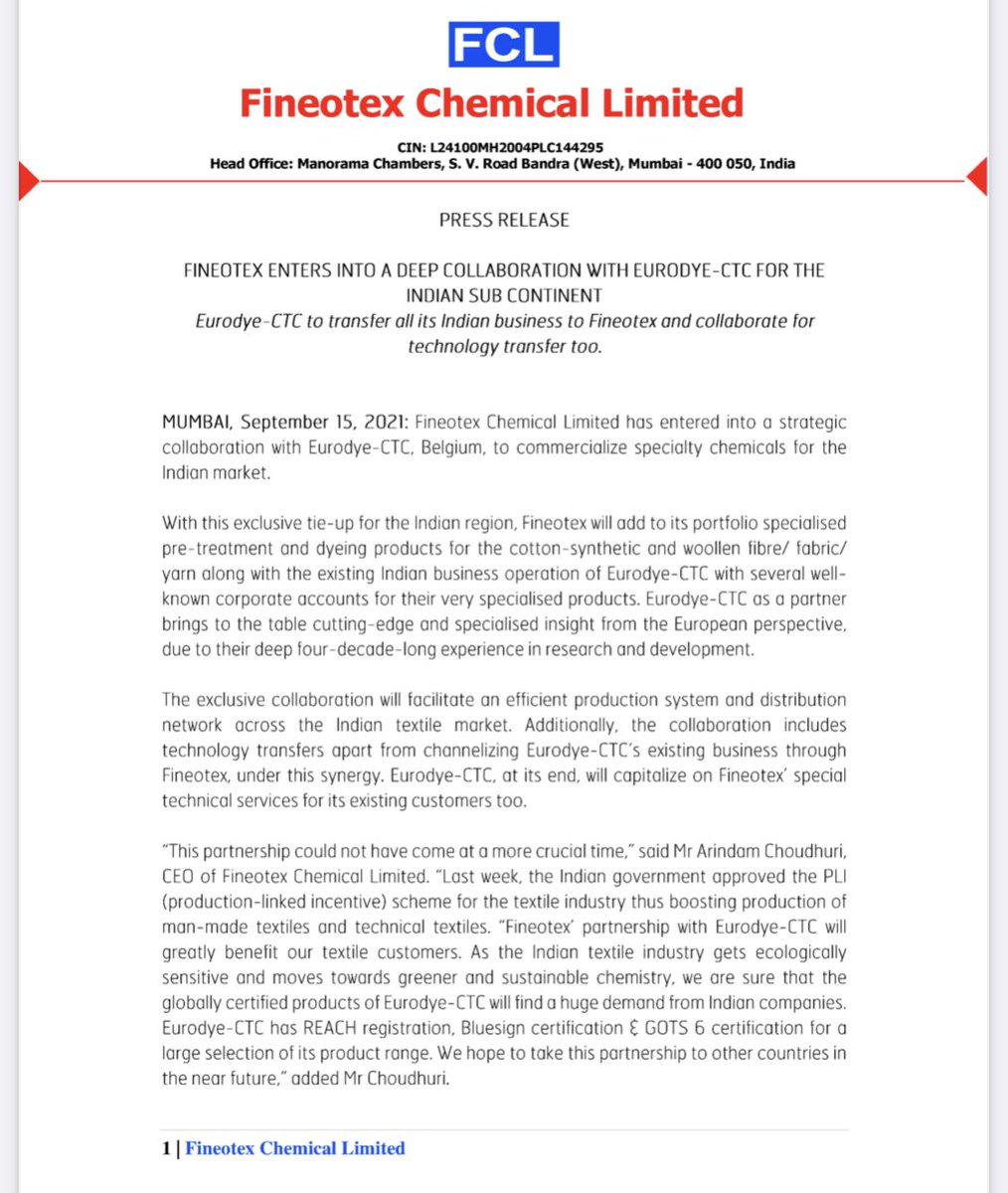

Furodye-CIC to transfer all its Indian business to Fineotex and collaborate for technology transfer too.

Fineotex chemicals-Good growth in top line , growth in bottom line also but RM price impacted growth of bottom line , but still good as compare to other companies in sector, cfo deteriorated.

Fineotex concall

- new expanded capacity will start on 9th nov .

- new expanded capacity will start on 9th nov .

EURODYE CTC - very high margin business and this will enhance EBDITA margins of company,

-Top ten customers contribute to 30% business so no concentration risk

-massive demand so we may go ahead with another capex

-Top ten customers contribute to 30% business so no concentration risk

-massive demand so we may go ahead with another capex

- demand is very high and looking at container problems we strategically kept inventory levels very high and keeping higher RM stock

- Demand is so high that we need to work even on Dipawali days also .

- Demand is so high that we need to work even on Dipawali days also .

-Hygiene business is growing very well and added some customers like Leela hotels , good margin business.

-H2 will be much much better then H1

- Ambarnath capex - 150 Cr Turnover is possible.

-H2 will be much much better then H1

- Ambarnath capex - 150 Cr Turnover is possible.

- RM easily available both domestically and internationally, no dependence on any particular supplier

Fineotex chemicals

Navi Mumbai- Capacity 36000 MT

Malaysia -6500 MT

Upcoming- Ambernath facility - 36000 TPA which will start on 9 th nov ( declared in Concall)

Q2 profit 11 Cr , mcap around 1400 Cr

Almost Debt free

EURODYE CTC - collaboration will add in margins

Navi Mumbai- Capacity 36000 MT

Malaysia -6500 MT

Upcoming- Ambernath facility - 36000 TPA which will start on 9 th nov ( declared in Concall)

Q2 profit 11 Cr , mcap around 1400 Cr

Almost Debt free

EURODYE CTC - collaboration will add in margins

Fineotex chemicals- started production in Ambernath ( 36000MT)

Fineotex chemicals - outstanding performance, congratulations to hard working promoter @sanjayfineotex

• • •

Missing some Tweet in this thread? You can try to

force a refresh