While this soundbite sounds good, it's not accurate. Using standard measures of market concentration, you can EASILY see that off-exchange trading is highly concentrated, and for large retail brokers it fits the DOJ definition for anti-trust enforcement.

https://twitter.com/Dougielarge/status/1438847925145194496

The Herfindahl Index (HHI) is a standard measure of corporate concentration. Total OTC trading in July 2021 showed an index of nearly 2,000, but that doesn't tell the real story. Looking just at HOOD's 606, their HHI ranges from 2,500 (S&P 500) to over 3,000 for options.

This is the literal definition of corporate concentration, and it results in worse outcomes for everyone involved (except for the wholesalers and HOOD executives).

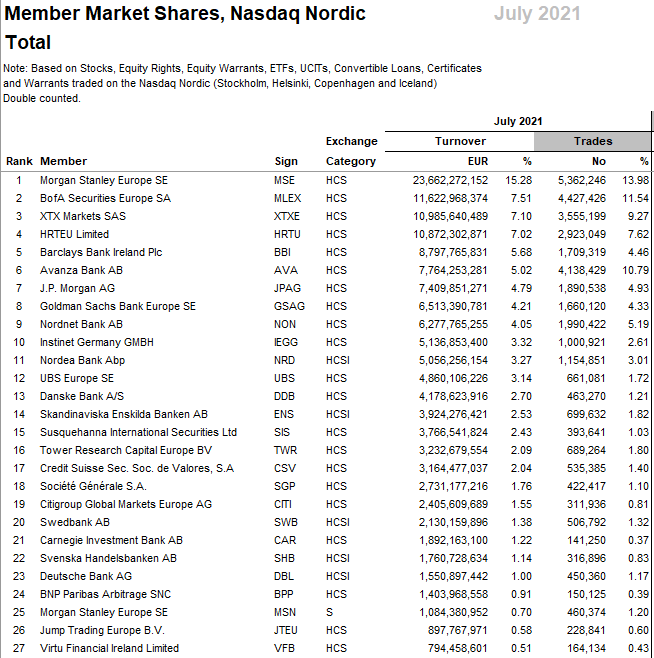

Data on lit exchanges is hard to find, but Nasdaq OMX publishes market share information on trading market share. The HHI on Nasdaq Nordiq? 578 - that means the market is extremely competitive.

It's simple - lit markets are competitive, off-exchange oligopolies are not.

It's simple - lit markets are competitive, off-exchange oligopolies are not.

Once again, this shouldn't surprise anyone. As Ken Griffin explains at minute 13, "In the high-frequency space in US equities, there are really only 2 firms that make any money of note"

It's no surprise that he wants to maintain this duopoly.

It's no surprise that he wants to maintain this duopoly.

• • •

Missing some Tweet in this thread? You can try to

force a refresh